• What is the sampling distribution of sample means is, and how can we we estimate a population mean

using the sampling distribution in section 5.1?

• What a testing hypothesis is and the testing hypothesis for a single population mean in section 5.2.

• Testing hypothesis for comparing two population means in section 5.3.

• Testing hypothesis for comparing several populations means using analysis of variance in section 5.4.

• Correlation and regression analysis to analyze the relation between several continuous variables in section 5.5.

5.1 Sampling distribution and estimation

A population is usually very massive, and it is difficult and costly to investigate the entire population.

Therefore, characteristic values of the population, such as a population mean

and variance called population parameters, are usually estimated using a set of samples.

Characteristic values of samples, such as a sample mean and sample variance called sample statistic.

The distribution of all possible values of the sample statistic is called a sampling distribution.

The sampling distribution identifies a relationship between the sample statistic and population parameter,

making it possible to estimate and to test a population parameter. Section 5.1.1 discusses the sampling distribution

of all possible sample means, and section 5.1.2 discusses how to estimate the population mean using

the sampling distribution.

5.1.1 Sampling distribution of sample means

A population mean μ is called a parameter of a population, one of the characteristic values of the population.

We collect samples of size n and calculate a sample mean to estimate the population mean.

We hope this sample mean can estimate the population mean correctly, but there are many ways to collect

samples of size n, and therefore, so many possible sample means. We hope this sample mean can estimate

the population mean correctly, but there are many ways to collect samples of size n, and therefore,

so many possible sample means. The distribution of all possible sample means is

called a sampling distribution of all possible sample means.

Since the sample mean is a random variable that can have many different values, it is usually denoted

with a capital letter such as \(\small \overline X \) and called an estimator of the population parameter μ.

An observed sample mean, marked \(\small \overline x \) with a lowercase letter, is called an estimate of μ.

If a population is a normal distribution \( N(μ, σ^2 ) \),

the distribution of all possible sample means is exactly a normal distribution \( N(μ, \frac {σ^2 }{n} ) \).

If a population is not a normal distribution but the sample size is large enough,

the distribution of all possible sample means is approximately a normal distribution such as \( N(μ, \frac {σ^2 }{n} ) \).

We call this the central limit theorem, which is a key theory underlying modern statistics.

Theoretical proof of this theorem is beyond the scope of this book; please refer to any book on mathematical statistics.

Central limit theorem

If a population has an infinite elements with a mean μ and variance \( σ^2 \),

then, if the sample size is large enough, the distribution of all possible sample means is

an approximately normal distribution \( N(μ, \frac {σ^2 }{n} ) \).

We can summarize specifically the central limit theorem as follows.

1) The average of all possible sample means, \(\small μ_{\overline X} \), is equal to the population mean μ. (i.e., \(\small μ_{\overline X} = μ \) )

2) The variance of all possible sample means, \(\small σ_{\overline X}^2 \), is the population variance divided by \(n\). (i.e., \(\small σ_{\overline X}^2 = \frac {σ^2}{n} \) )

3) The distribution of all possible sample means is approximately a normal distribution.

The above facts can be briefly written as \(\small \overline {X} \sim N(μ, \frac {σ^2}{n} ) \).

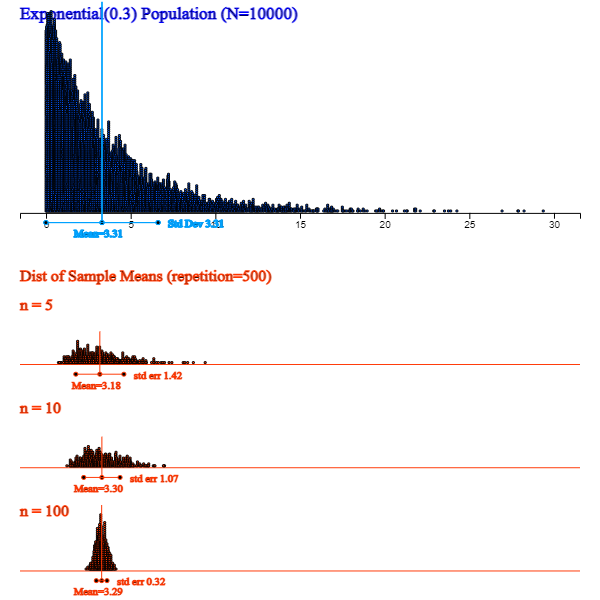

The following simulation using 『eStatU』 shows that when a population is a normal distribution,

the distribution of all possible sample means is approximately normal, but variances become smaller as the sample size increases.

[Central Limit Theorem]

<Figure 5.1.1> shows a simulation using 『eStatU』 in case a population is skewed

from its mean. The distribution of all possible sample means is closer to normal as the sample size increases.

<Figure 5.1.1> 『eStatU』 Simulation of the central limit theorem

5.1.2 Estimation of a population mean

When a sample survey is conducted, only one set of samples, usually smaller than the population size,

is selected from a population to estimate a characteristic value of the population, such as the population mean.

We typically consider the sample mean of the selected samples to estimate the population mean.

Can this sample mean can estimate the population mean well, even if the sample mean is only calculated

from one set of small samples? This question is fundamental in estimating the population parameter

that everyone can think about at least once. The sampling distribution of all possible sample means

answers this question. Whatever the population distribution is, if the sample size

is large enough, all possible sample means are distributed around the population mean in the form

of a normal distribution by the central limit theorem. Therefore, the sample mean obtained from one set of samples is usually

close to the population mean. Even in the worst case, the difference between the population mean

and sample mean, known as an error, is not so significant, and it is possible to estimate the

population mean using the sample mean. The larger the sample size, the more sample means are

concentrated around the population mean based on the central limit theorem and hence,

we can reduce the error of the estimation.

The value of an observed sample mean is called a point estimate of the population mean.

In general, the sample statistic used to estimate a population parameter must have good characteristics

to be accurate. The sample mean has all the good characteristics to estimate the population mean,

and the sample variance also has all the good characteristics to estimate the population variance.

In contrast to the point estimate for a population mean, estimating the population mean using an interval

is called an interval estimation.

If a population follows a normal distribution with the mean μ and variance \(σ^2 \),

the distribution of all possible sample means follows a normal distribution with the mean μ and variance \(\frac {σ^2}{n} \),

so the probability that one sample mean will be included in the interval

\( [\, μ - z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} ,\; μ + z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} \,]\)

is \(\small 1 -\alpha \) as follows.

$$\small

P(\mu - z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} < \overline X < \mu + z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} ) = 1 - \alpha

$$

We can rewrite this formula as follows.

$$\small

P(\overline X - z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} < \mu < \overline X + z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} ) = 1 - \alpha

$$

Assuming σ is known, the meaning of the above formula is that 95% of intervals obtained by applying the formula

\(\small [ \overline {X} - z_{\alpha / 2} \times \frac {σ}{\sqrt{n}}, \overline {X} + z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} ] \)

for all possible sample means include the population mean. The formula of this interval is referred to as

the 100(1- \(\alpha \))% confidence interval of the population mean.

$$\small

\left[ \overline {X} - z_{\alpha / 2} \times \frac {σ}{\sqrt{n}}, \overline {X} + z_{\alpha / 2} \times \frac {σ}{\sqrt{n}} \right]

$$

100(1-α)% here is called a confidence level, which refers to the probability of intervals that will include

the population mean among all possible intervals calculated by the confidence interval formula. Usually, we use 0.01 or 0.05 for α.

\( z_{α} \) is the upper α percentile of the standard normal distribution.

In other words, if \(Z\) is the random variable that follows the standard normal distribution,

the probability that \(Z\) is greater than \( z_{α} \) is α, i.e.,

$$

P(Z > z_{α} ) = α

$$

For example, \( z_{0.025;} \) = 1.96, \( z_{0.05} \) = 1.645, \( z_{0.01} \) = 2.326, and \( z_{0.005} \) = 2.575.

The following simulation shows the 95% confidence intervals for the population mean by extracting

100 sets of samples with the sample size \(n\) = 20

from a population of 10,000 numbers which follow the standard normal distribution N(0,1).

In this case, 96 of the 100 confidence intervals contain the population mean 0.

This result might be different on your computer because the program uses a random number generator,

which depends on the computer. Whenever we repeat these experiments, the result may also vary slightly.

[Confidence Interval Experiment]

Example 5.1.1

The average monthly starting salary of college graduates was 275 (unit: 10,000 KRW) after a simple random sampling

of 100 this year. Assume that the starting salary for all college graduates follows a normal distribution

with a standard deviation of 5.

1) What is the point estimate of the average monthly starting salary of all college graduates?

2) Estimate a 95% confidence interval of the average monthly starting salary of college graduates.

3) Estimate a 99% confidence interval of the average monthly starting salary of college graduates. Compare the width of this interval to the 95% confidence interval.

4) If the sample size is increased to 400 and its average is the same, estimate a 95% confidence interval of the average monthly starting salary for all college graduates. Compare the width of the interval to question 2).

Answer

1) Point estimation of the average monthly starting salary is the sample mean which is 275 (unit: 10,000 KRW).

2) Since the 95% confidence interval implies α = 0.05, z value is as follows.

\( \qquad \small z_{α/2} = z_{0.05/2} = 1.96 \)

Therefore, the 95% confidence interval is as follows.

Therefore, as the sample size increases, the width of the confidence interval becomes narrower, which is more accurate.

Practice 5.1.1

A large manufacturer's quality manager wants to know raw materials' average weight. Twenty-five samples

were collected by simple random sampling, and their sample mean was 60 kg. Assume the population

standard deviation is 5 kg. Use 『eStatU』 to answer the following.

1) What is a point estimation of the population mean weight of raw materials?

2) Estimate a 95% confidence interval of the population mean weight of raw materials.

3) Estimate a 99% confidence interval of the population mean weight of raw materials. Compare the width of this interval to the 95% confidence interval.

4) If the sample size is increased to 100 and its average is the same, estimate a 95% confidence interval of the population mean weight of raw materials. Compare the width of the interval to question 2).

Interval estimation of a population mean – Unknown population variance

One problem in estimating the unknown population mean using the confidence interval formula

in the previous section is that the population variance may be unknown.

If the sample size is large enough, a confidence interval of

the population mean can be obtained approximately using the sample variance instead of the population variance

in the confidence interval formula. However, if the sample size is small and the sample variance is used,

we should use a confidence interval based on the \(t\) distribution.

The \(t\) distribution was studied by a statistician W. S. Gosset, who worked for a brewer in Ireland

and published his study result in 1907 under the alias Student.

So \(t\) distribution is often referred to as Student's \(t\) distribution. The \(t\) distribution

is not just a single distribution, but it is a family of distributions with a parameter called

a degree of freedom, 1,2, ... , 30, ... and denoted as \(t_1 ,t_2 , ... , t_{30} , ... \)

The shape of the \(t\) distribution is symmetrical about zero (y axis), similar to the standard normal

distribution, but it has a tail that is flat and longer than the standard normal distribution.

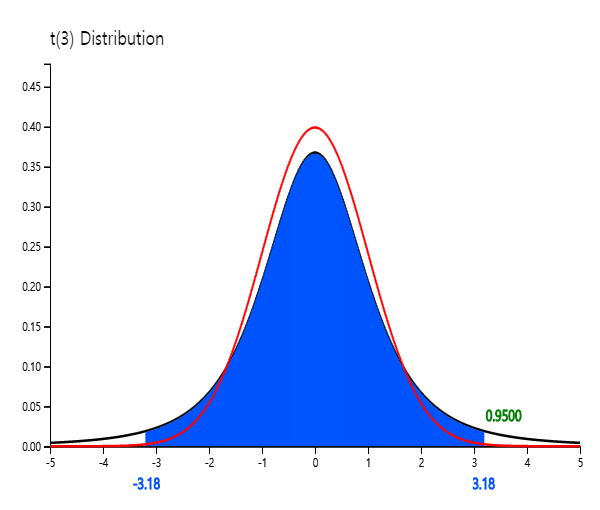

<Figure 5.1.2> shows the standard normal distribution N(0,1), and \(t\) distribution

with 3 degrees of freedom simultaneously using the \(t\) distribution module of 『eStatU』.

<Figure 5.1.2> Comparison of \(t_3\) and N(0,1)

The \(t\) distribution is closer to the standard normal distribution as degrees of freedom increase above 100,

which is why a confidence interval can be obtained approximately using the standard normal distribution

if the sample size is greater than 100.

Denote \(t_{n:\,α}\) as the 100\(\times\)α% percentile from the right tail

of the \(t\) distribution with \(n\) degrees of freedom.

For example, \(t_{7:\,0.05}\) is the 5% percentile of the \(t\) distribution from the right tail and its value is 1.895

as <Figure 5.1.3>. In the standard normal distribution, this value was 1.645. Since

the \(t\) distribution is symmetrical, \(t_{n:\,1-α} = - t_{n:\,α}\).

To find a percentile value from the right tail of the \(t_{7}\) distribution using 『eStatU』,

click on '\(t\) distribution' in the main menu of 『eStatU』 and then set the degree of freedom (df) to 7,

and set the probability value in the sixth option below the \(t\) distribution graph to 0.05,

then \(t_{7:\,0.05}\) = 1.895 will appear.

[t Distribution]

<Figure 5.1.3> The 5% percentile of the \(t\) distribution from the right tail

Assume that a population follows a normal distribution, and consider an interval estimation of

the population mean in case of the unknown population variance.

If \( X_1 , X_2 , ... , X_n \) is a random sample of size \(n\) from the population,

then it can be shown that the distribution of \( \frac {\overline X -\mu}{S/\sqrt{n}} \), where σ is replaced with S,

is the \(t\) distribution with \( n-1 \) degrees of freedom.

$$\small

\frac {\overline X -\mu}{\frac{S}{\sqrt{n}}} \sim t_{n-1}

$$

Hence, the probability of the following interval is (1 - α).

$$\small

P \left( -t_{n-1;\;\alpha/2} < \frac {\overline{X} - \mu } {\frac{S}{\sqrt{n}}} < t_{n-1:\;\alpha/2} \right) = 1 - \alpha

$$

The above formula can be summarized as the confidence interval for the population mean when the population variance is unknown.

$$\small

\left[\; \overline X - t_{n-1:\;\alpha/2} \frac {S} {\sqrt{n}} ,\; \overline X + t_{n-1:\;\alpha/2} \frac {S} {\sqrt{n}} \; \right]

$$

where \(n\) is the sample size and \(\small S\) is the sample standard deviation.

Example 5.1.2

Suppose we do not know the population variance in Example 4.4.2. If the sample size is 25 and the sample standard deviation is 5 (unit: 10,000 KRW), estimate the mean of the starting salary of college graduates at the 95% confidence level.

Answer

Since we do not know the population variance, we should use the \(t\) distribution for interval estimation of the population mean.

Since \( t_{n-1:\;\alpha/2} = t_{25-1:\;0.05/2} = t_{25-1:\;0.025} = 2.0639 \), the 95% confidence interval of the population mean is as follows.

$$ \small

\begin{multline}

\shoveleft \left[ \overline X - t_{n-1:\;\alpha/2} \frac {S} {\sqrt{n}} , \overline X + t_{n-1:\;\alpha/2} \frac {S} {\sqrt{n}} \right] \\

\shoveleft ⇔ [ 275 - 2.0639(5/5) , 275 + 2.0639(5/5) ] \\

\shoveleft ⇔ [ 272.9361, 277.0639 ]

\end{multline}

$$

Note that the smaller the sample size, the wider the interval width.

Example 5.1.3

The following data shows a simple random sampling of 10 new male students' heights in a college this year.

Use 『eStatU』 to make a 95% confidence interval of the height of the first-year college students.

171 172 185 169 175 177 174 179 168 173

Answer

Click [Estimation : μ Confidence Interval] on the menu of 『eStatU』 and enter data at the [Sample Data] box.

Then the confidence intervals [170.68, 177.92] are calculated using the \(t_9\) distribution.

In this 『eStatU』 module, confidence intervals can also be obtained by entering the sample sizes,

sample mean, and sample variance without entering data.

[ ]

In this module of 『eStatU』, a simulation experiment to investigate the size of the confidence interval

can be done by changing the sample size \(n\) and the confidence level 1 - α.

If you increase \(n\), the interval size becomes narrower. If you increase 1 - α,

the interval size becomes wider.

Practice 5.1.2

In [Practice 5.1.1], suppose you do not know the population standard deviation,

and the sample standard deviation is 5 kg. Answer the same questions in [Practice 5.1.1] using 『eStatU』.

5.2 Testing hypothesis for a population mean

Examples of testing hypotheses for a population mean are as follows.

- The weight of a cookie bag is indicated as 200g. Would there be enough cookies to meet the indicated weight?

- At a light bulb factory, a newly developed light bulb advertises a longer bulb life than the past one. Is this propaganda reliable?

- Immediately after completing this year's academic test, students said there would be a 5-point increase

in the average English score, which is higher than last year. How can you investigate if this is true?

The testing hypothesis is an answer to the above questions (hypothesis). The testing hypothesis is

a statistical decision-making method using samples, which is used to compare two hypotheses about the population

parameter. This section discusses the test of the population mean, which is frequently used in applications.

The following example explains the theory of the testing hypothesis about a single population mean.

Example 5.2.1

At a light bulb factory, the average life expectancy of a light bulb made by a conventional production method is known

to be 1500 hours, and the standard deviation is 200 hours. Recently, the company has been trying to introduce a new production method,

with an average life expectancy of 1600 hours for light bulbs. Thirty samples were taken by simple random sampling from

the new type of light bulbs to confirm this argument, and the sample mean was \(\small \overline x \) = 1555 hours.

Can you tell me that the new light bulb has an average life of 1600 hours?

Answer

A statistical approach to the question of this issue is first to make two assumptions about the different arguments

for the population mean μ . Namely,

$$ \small

\begin{multline}

\shoveleft H_0 : μ = 1500 \\

\shoveleft H_1 : μ = 1600

\end{multline}

$$

\(\small H_0\) is called a null hypothesis and \(\small H_1\) is an alternative hypothesis.

In most cases, the null hypothesis is defined as an ‘existing known fact’ and the alternative hypothesis is defined as

‘new facts or changes in current beliefs’. So when choosing between two hypotheses, the basic idea of testing a hypothesis

is 'unless there is a significant reason, we accept the null hypothesis (current fact) without choosing the alternative

hypothesis (the fact of the matter). This idea of testing a hypothesis is referred to as ‘conservative decision making’.

A common sense for choosing between two hypotheses is 'which population mean of two hypotheses is

closer in the distance to the sample mean'. Based on this common sense, which uses the concept of distance,

the sample mean of 1555 is closer to \(\small H_1 : μ = 1600\), so we choose the alternative hypothesis.

However, a statistical testing hypothesis makes a decision using the sampling distribution of \(\small \overline X\)

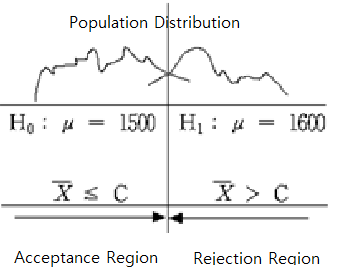

to select a critical value \(C\) and to make a decision rule as follows.

\( \small

\qquad \text { ‘If \(\overline X\) is smaller than C, then the null hypothesis \(H_0\) will be chosen, else reject \(H_0\)’}

\)

The area of {\(\small \overline X ≤ C\)} is called an acceptance region of \(\small H_0\) and

the area {\(\small \overline X > C\)} is called

a rejection region of \(\small H_0\) (<Figure 5.2.1>).

<Figure 5.2.1> Acceptance and rejection region of \(H_{0}\)

If this decision rule chooses a hypothesis, there are always two possible errors.

One is a Type 1 Error which accepts \(\small H_1\) when \(\small H_0\) is true,

the other is a Type 2 Error which accept \(\small H_0\) when \(\small H_1\) is true.

We can summarize these errors as in Table 5.2.1.

Table 5.2.1 Two types of errors in testing hypothesis

Actual \(\small H_0\) is true

Actual \(\small H_1\) is true

Decision : \(\small H_0\) is true

Correct

Type 2 Error

Decision : \(\small H_1\) is true

Type 1 Error

Correct

If you try to reduce one type of error when the sample size is fixed, the other type of error will increase.

That is why we came up with a conservative decision-making method that defines the null hypothesis \(\small H_0\)

as 'past or present facts' and 'accept the null hypothesis unless there is significant evidence for the

alternative hypothesis.' In this conservative way, we try to reduce the type 1 error as much as possible that selects

\(\small H_1\) when \(\small H_0\) is true, which would be more risky than the type 2 error. The testing hypothesis

determines the tolerance for the probability of the type 1 error, usually 5% or 1% for rigorous tests,

and uses the selection criteria that satisfy this limitation. The tolerance for the probability that this

type 1 error will occur is called the significance level and denoted as α.

The probability of the type 2 error is denoted as β.

If the significance level is established, the decision rule for the two hypotheses can be tested using the

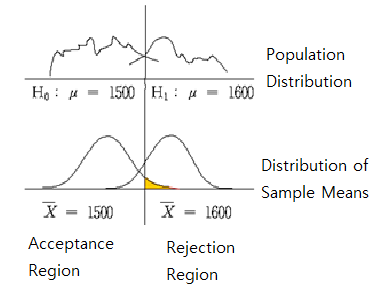

sampling distribution of all possible sample means. <Figure 5.2.2> shows two population distributions

of two hypotheses and their sampling distributions of all possible sample means in each hypothesis.

<Figure 5.2.2> Testing Hypothesis

The sampling distribution of all possible sample means, which corresponds to the population

of the null hypothesis \(\small H_0\) : μ = 1500, is approximately normal

\(\small N(1500,200^2 )\) by the central limit theorem.

The sampling distribution of all possible sample means, which corresponds to the population

of the alternative hypothesis \(\small H_1\) : μ = 1600, is approximately normal

\(\small N(1600,200^2 )\). The population standard deviation for each population is

assumed to be 200 from historical data. Then, the decision rule becomes as follows.

\( \small

\qquad \text {‘If \(\overline X ≤ C\), then accept \(H_{0}\), else accept \(H_{1}\) (i.e. reject \(H_{0}\) )’}

\)

In Figure 5.2.2, the shaded area represents the probability of the type 1 error. If we set the significance level,

which is the tolerance level of the type 1 error, is 5%, i.e., \(\small P(\overline X ≤ C) = 0.95\), \(C\)

can be calculated by finding the percentile of the normal distribution \(\small N(1500,\frac{200^2}{30})\) as follows.

In this problem, the observed sample mean of the random variable \(\small \overline X\) is

\(\small \overline x\)= 1555 and \(\small H_0 \) is accepted. In other words, the hypothesis of

\(\small H_0 \) : μ = 1500 is judged to be correct, which contradicts the result of

common sense criteria that \(\small \overline x\) = 1555 is closer to \(\small H_1 \) : μ = 1600

than \(\small H_0 \) : μ = 1500. We can interpret that the sample mean

of 1555 is insufficient evidence to reject the null hypothesis using a conservative decision-making method.

The above decision rule is often written as follows, emphasizing that it results from a conservative

decision-making method.

\( \small

\qquad \text {‘If \(\overline X\) ≤ 1560.06, then do not reject \(H_0\), else reject \(H_0 \).’}

\)

In addition, this decision rule can be written for calculation purposes as follows.

\( \small

\qquad \text {‘If \(\frac{\overline X - 1500}{\frac {200}{\sqrt{30}}}\) ≤ 1.645, then accept \(H_0\) , else reject \(H_0\).’}

\)

In this case, since \(\small\overline x\) = 1555, \(\frac{1555 - 1500}{\frac {200}{\sqrt{30}}}\) = 1.506,

and it is less than 1.645. Therefore, we accept \(\small H_0\).

Since the testing hypothesis by the conservative decision-making is only based on the probability of

the type 1 error as seen in [Example 5.2.1], even if the alternative hypotheses is \(H_1 : μ > 1500\),

we will have the same decision rule.

Generally, there are three types of alternative hypotheses in the testing hypothesis for the population mean as follows.

1) \(\quad H_1 : \mu \gt \mu_0\)

2) \(\quad H_1 : \mu \lt \mu_0\)

3) \(\quad H_1 : \mu \ne \mu_0\)

Since 1) has the rejection region on the right side of the sampling distribution of all possible sample means

under the null hypothesis, it is called a right-sided test. Since 2) has the rejection region on the left side

of the sampling distribution, it is called a left-sided test. Since 3) has rejection regions on both sides

of the sampling distribution, it is called a two-sided test.

In [Example 5.2.1], if the sample mean is either 1555 or 1540, we cannot reject the null hypothesis,

but the degrees of evidence that the null hypothesis is not rejected are different.

The degree of evidence that the null hypothesis is not rejected is measured by calculating the probability of the type 1 error

when the observed sample mean value is considered as the critical value for decision, which is called the \(p\)-value.

That is, the \(p\)-value indicates where the observed sample mean is located among all possible sample means by

considering the location of the alternative hypothesis. In [Example 5.2.1], the \(p\)-value for \(\small\overline X\) = 1540

is the probability of sample means which is greater than \(\small\overline X\) = 1540 using \(N(1500, \frac{200^2}{30} )\) as follows.

$$ \small

p\text{-value} = P( \overline X > 1540) = P(\frac{\overline X - 1500}{\frac{200}{\sqrt{30}}} ) = 0.0660

$$

The higher the \(p\)-value, the stronger the reason for not being rejected. If \(H_0\) is rejected, the smaller

the \(p\)-value, the stronger the grounds for rejection. Therefore, if the \(p\)-value is less than the significance level

the analyst decided, then \(H_0\) is rejected because it means that the sample mean is in the rejection region.

Statistical packages provide this \(p\)-value. The decision rule using \(p\)-value is as follows.

'If \(p\)-value < α, then \(H_0\) is rejected, else \(H_0\) is accepted.'

If the population standard deviation, σ, is unknown and the population follows a normal distribution,

the test statistic

$$\small

\frac {\overline X - \mu_0}{ \frac {S}{\sqrt{n}} }

$$

is a \(t\) distribution with \((n-1)\) degrees of freedom. If the population standard deviation is unknown,

the decision rule for each type of three alternative hypothesis are summarized in Table 5.2.2 where α

is the significance level.

Table 5.2.2 Testing hypothesis for a population mean - unknown σ case

If \(\small \left | \frac {\overline X - \mu_0}{ \frac {S}{\sqrt{n}} } \right | > t_{n-1; \; α/2} \), then reject \( H_0 \)

Note: Assume that the population is a normal distribution.

The \(\small H_0\) of 1) can be written as \(\small H_0 : \mu \le \mu_0 \) , 2) as \(\small H_0 : \mu \ge \mu_0 \)

Example 5.2.2

The weight of a bag of cookies is supposed to be 250 grams. Suppose the weight of all bags of cookies follows

a normal distribution. In the survey of 16 random samples of bags, the sample mean

was 253 grams, and the sample standard deviation was 10 grams.

Test the hypothesis whether the weight of the bag of cookies is 250g or larger using α = 1% and find the \(p\)-value.

Use 『eStatU』 to test the hypothesis above.

Answer

Since the population standard deviation is unknown and the sample size is small, the decision rule is as follows.

$$ \small

\begin{multline}

\shoveleft \text{'If } \frac {\overline X - \mu_0} {\frac {S}{\sqrt{n}} } > t_{n-1: \; α} , \text{ then reject } H_0 \text{ else accept } H_0 ’ \\

\shoveleft \text{'If } \frac {253 - 250}{ \frac {10}{\sqrt{16}} } > t_{16:\; 0.01} , \text{ then reject } H_0 \text{ else accept } H_0 ’ \\

\end{multline}

$$

Since the value of test statistic is \( \frac {253 - 250}{ \frac {10}{\sqrt{16}} } = 1.2 \),

and \(t_{15: \; 0.01} = 2.602\) , we accept \(\small H_0\). Note that the decision rule can be written as follows.

In 『eStatU』 menu, select [Testing Hypothesis μ], enter 250 at the box on [Hypothesis] and

select the alternative hypotheses as the right test. Check [Test Type] as t test and enter &alpha = 0.01.

At the [Sample Statistics], enter sample size 16, sample mean 253, and sample variance \(10^2 = 100\).

If you click the [Execute] button, the confidence Interval for μ is calculated, and

the testing result will appear as in <Figure 5.2.3>.

<Figure 5.2.3> Testing hypothesis for μ with \(t\) distribution using 『eStatU』

Since the \(p\)-value is the probability that \(t_{15}\) is greater than the test statistics 1.200,

the \(p\)-value is 0.124 using the module of \(t\) distribution in 『eStatU』.

[Testing Hypothesis : Population Mean μ ]

Practice 5.2.1

The following data are weights of the 7 employees randomly selected who are working in the shipping department of a wholesale food company.

154, 186, 159, 174, 183, 163, 181 (unit pound)

Ex ⇨ DataScience ⇨ Weight.csv.

Based on this data, is the average weight of employees working in the shipping department 160 or greater than 160? Use the significance level of 5%.

5.3 Testing hypothesis for two populations means

When samples are selected independently from two populations,

an estimator for the difference of two population means, \(\mu_1 - \mu_2\), is the difference

of two sample means, \(\small {\overline x}_1 - {\overline x}_2\). The sampling distribution of

all possible sample means differences is approximately a normal distribution with the mean

\(\mu_1 - \mu_2\) and variance \(\frac{\sigma^2_1}{n_1} + \frac{\sigma^2_2}{n_2}\)

if both sample sizes are large enough.

Since the population variances \( \sigma^2_1 \) and \( \sigma^2_2 \) are usually unknown,

sample variances, \(\small S^2_1 \) and \(\small S^2_2 \), are used.

If the two populations follow normal distributions and their variances can be assumed to be the same,

we can show that the following sample statistic for the sample means difference follows

\(t\)-distribution with \(n_1 + n_2 -2\) degrees of freedom.

$$ \small

\frac { ({\overline X}_1 - {\overline X}_2 ) }{\sqrt{\frac{S^2_p}{n_1} +\frac{S^2_p}{n_2} } }

\qquad \text{where } S^2_p = \frac{(n_1 -1 )S^2_1 + (n_2 -1)S^2_2}{n_1 + n_2 -2}

$$

\(s^2_p\) is an estimator of the population variance called as a pooled variance

which is an weighted average of two sample variances \( s^2_1 \) and \( s^2_2 \) using

the sample sizes as weights when population variances are assumed to be the same.

Assume that two populations follow normal distributions as \(\small N(\mu_1 , \sigma_1^2 )\), and

\(\small N(\mu_1 , \sigma_1^2 )\). Consider the interval estimation of the population mean difference

when you do not know the population variances, but they can be assumed to be the same.

Using the sampling distribution of the sample mean differences described above,

the 100(1 - α)% confidence interval for the population mean difference when the population variances are unknown

can be shown as follows.

$$\small

\left[\; (\overline X_1 - \overline X_2 ) - t_{n_1 + n_2 - 2: \;\alpha/2} \sqrt { \frac{S^2_p}{n_1} + \frac{S^2_p}{n_2} },\; (\overline X_1 - \overline X_2 ) + t_{n_1 + n_2 -2:\;\alpha/2} \sqrt { \frac{S^2_p}{n_1} + \frac{S^2_p}{n_2} } \;\right]

$$

where \(n_1\) and \(n_2\) are the sample size, \(\small {\overline X}_1 \) and \(\small {\overline X}_2 \)

are sample means of each population.

\(s^2_p\) is an estimator of the population variance, called the pooled variance.

A comparison of two populations means, \(\small \mu_1\) and \(\small \mu_2\). is possible by testing the hypothesis

that the difference in the population means is equal to zero or not.

There are many examples comparing the means of two populations as follows.

- Is there a difference between the starting salary of male and female graduates in this year’s college graduates?

- Is there a difference in the weight of the products produced in the two production lines?

Generally, testing hypothesis for two populations means can be divided into three types,

depending on the type of alternative hypothesis.

$$ \small

\begin{multline}

\shoveleft 1)\quad H_0 : \mu_1 - \mu_2 = D_0 \qquad H_1 : \mu_1 - \mu_2 \gt D_0 \\

\shoveleft 2)\quad H_0 : \mu_1 - \mu_2 = D_0 \qquad H_1 : \mu_1 - \mu_2 \lt D_0 \\

\shoveleft 3)\quad H_0 : \mu_1 - \mu_2 = D_0 \qquad H_1 : \mu_1 - \mu_2 \ne D_0 \\

\end{multline}

$$

Here \(\small D_0\) is the value for the difference in population means to be tested.

When samples are selected independently from two populations,

the estimator of the difference of two population means, \(\small \mu_1 - \mu_2\), is the difference

of sample means, \(\small {\overline x}_1 - {\overline x}_2\).

If two populations follow normal distributions and their variances can be assumed to be the same,

the testing hypothesis for the difference between the two populations means uses the following statistic.

$$ \small

\frac { ({\overline x}_1 - {\overline x}_2 ) - D_0 }{\sqrt{\frac{s^2_p}{n_1} +\frac{s^2_p}{n_2} } }

\qquad \text{where } s^2_p = \frac{(n_1 -1 )s^2_1 + (n_2 -1)s^2_2}{n_1 + n_2 -2}

$$

The test statistic follows a \(t\)-distribution with \(n_1 + n_2 -2\) degrees of freedom.

The decision rule for testing the difference between the two populations' means is as follows.

Table 5.3.1 Testing hypothesis of two populations means

Note: Assume independent samples, normal populations, population variances are equal.

If sample sizes are large enough (\(\small n_1 > 30, n_2 >30 \)), \(t\)-distribution is

approximately close to the standard normal distribution and the decision rule may use the standard

normal distribution.

Example 5.3.1

Two machines produce cookies at a factory, and a cookie bag's average weight should be 270g. We sampled cookie bags

from each of the two machines to examine the weight of the cookie bags. The average weight of 15 cookie bags extracted

from machine 1 was 275g, and their standard deviation was 12g. The average weight of 14 cookie bags extracted

from machine 2 was 269g, and the standard deviation was 10g.

1) Find a 99% confidence interval for the difference between two population means.

2) Test whether the two machines' cookie bag weights are different. Use α = 0.01.

3) Check the test result using 『eStatU』.

Answer

1) We can summarize the sample information in this example as follows.

$$ \small

\begin{multline}

\shoveleft n_1 = 15,\quad \overline x_1 = 275,\quad s_1 = 12 \\

\shoveleft n_2 = 14,\quad \overline x_2 = 269,\quad s_2 = 10 \\

\end{multline}

$$

Therefore, the pooled variance of two samples is as follows.

$$ \small

\begin{multline}

\shoveleft s^2_p = \frac{(n_1 -1 )s^2_1 + (n_2 -1)s^2_2}{n_1 + n_2 -2}

= \frac{(15 - 1 ) 12^2 + (14 - 1) 10^2}{15 + 14 -2} = 122.815 \\

\end{multline}

$$

Since the t-value for 99% confidence interval is \(\small t_{15 + 14 -2;\; 0.01/2} = t_{27:\; 0.005} = 2.7707\),

the 99% confidence interval is as follows.

$$ \small

\begin{multline}

\left[\; (\overline X_1 - \overline X_2 ) - t_{n_1 + n_2 - 2: \;\alpha/2} \sqrt { \frac{S^2_p}{n_1} + \frac{S^2_p}{n_2} },\; (\overline X_1 - \overline X_2 ) + t_{n_1 + n_2 -2:\;\alpha/2} \sqrt { \frac{S^2_p}{n_1} + \frac{S^2_p}{n_2} } \;\right]

\end{multline}

$$

$$\small

\begin{multline}

\left[\; (275 - 269) - 2.7707 \sqrt { \frac{122.815}{15} + \frac{122.815}{14} },\; (275 - 269) + 2.7707 \sqrt { \frac{122.815}{15} + \frac{122.815}{14} } \;\right] \\

\end{multline}

$$

$$\small

\begin{multline}

\left[\; -5.410, \; 17.410 \; \right ]

\end{multline}

$$

2) The hypothesis of this problem is \(\small H_0 : \mu_1 = \mu_2 ,\, H_1 : \mu_1 \ne \mu_2 \). Hence, the decision rule is as follows.

$$ \small

\begin{multline}

\shoveleft '\text{If } \left | \frac { ({\overline x}_1 - {\overline x}_2 ) - D_0 }{\sqrt{\frac{s^2_p}{n_1} +\frac{s^2_p}{n_2} } } \right | > t_{n_1 + n_2 -2;\, α/2} , \text{ then reject } H_0 ’ \\

\end{multline}

$$

\(\small D_0 = 0\) in this exaample. The calculation of the test statistic is as follows.

$$ \small

\begin{multline}

\shoveleft \left | \frac {275 - 269} { \sqrt{\frac{122.815}{15} +\frac{122.815}{14} } } \right | = 1.457 \\

\end{multline}

$$

Since 1.457 < 2.7707, \(\small H_0\) can not be rejected.

3) In 『eStatU』 menu, select [Testing Hypothesis \(\mu_1 , \mu_2\)]. At the window shown in <Figure 5.3.1>,

check the alternative hypotheses of not equal case at [Hypothesis], check the variance assumption of

[Test Type] as the equal case, check the significance level of 1%, check the independent sample,

and enter sample sizes \(n_1 , n_2\), sample means \(\small \overline x_1 , \overline x_2\), and sample variances

as the following window. Click [Execute] button to see the confidence interval and result of the testing hypothesis.

[Testing Hypothesis : two populations Means μ1, μ2]

If variances of two populations are different, the test statistic

$$\small

\frac { ({\overline x}_1 - {\overline x}_2 ) - D_0 }{\sqrt{\frac{s^2_1}{n_1} +\frac{s^2_2}{n_2} } }

$$

does not follow a \(t\)-distribution even if populations are normally distributed. The testing hypothesis

for two populations means when their population variances are different is called a Behrens-Fisher problem,

and several methods to solve this problem have been studied. The Satterthwaite method approximates

the degrees of freedom of the \(t\)-distribution in the decision rule in Table 5.3.1 with \(\phi\) as follows.

$$

\phi = \frac { \left( \frac{s_1^2}{n_1} + \frac{s_2^2}{n_2} \right)^2 }

{ \frac { \left( \frac{s_1^2}{n_1} \right)^2 } {n_1 -1} + \frac { \left( \frac{s_2^2}{n_2} \right)^2 } {n_2 -1} }

$$

Example 5.3.2 (Monthly wages by male and female)

Random samples of 10 male and female college graduates this year showed their monthly

wages as follows. (Unit 10,000 KRW)

1) If population variances are assumed to be the same, test the hypothesis at the 5%

significance level of whether the average monthly wage for males and females is the same.

2) If population variances are assumed to be different, test the hypothesis at the 5%

significance level of whether the average monthly wage for males and females is the same.

Answer

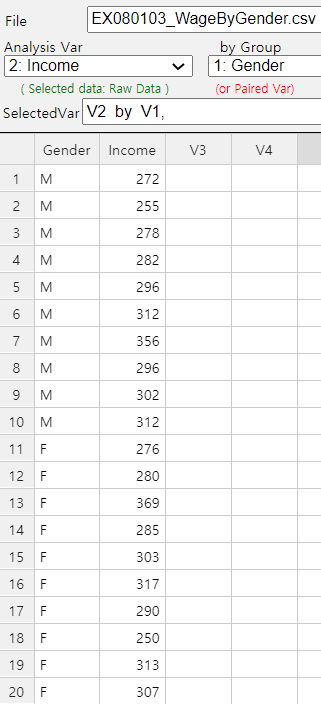

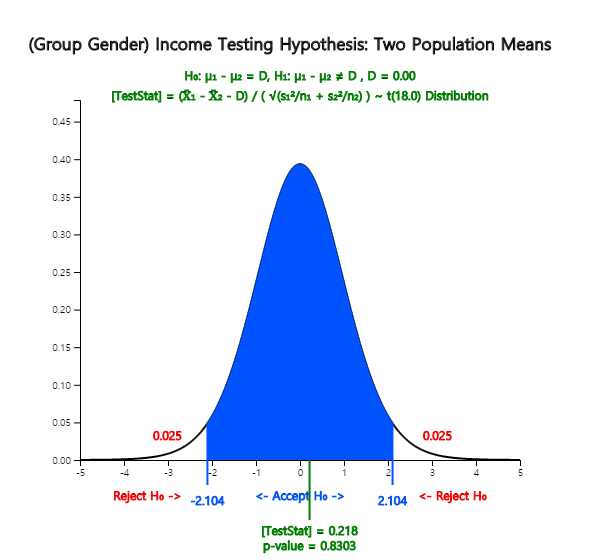

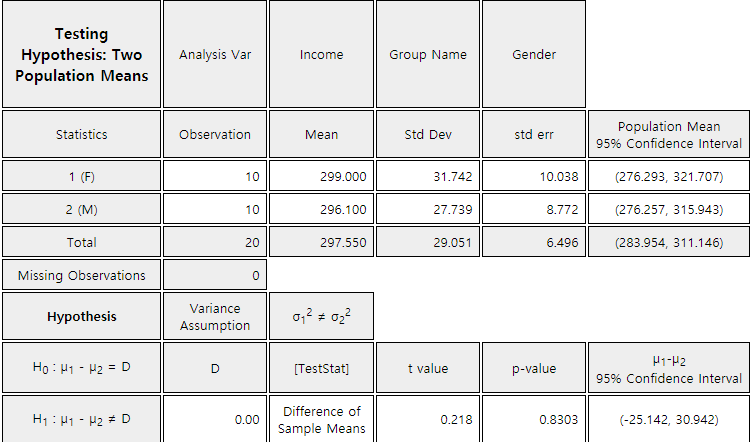

1) In 『eStat』, enter raw data of gender (M or F) and income as shown in <Figure 5.3.1>

on the sheet. This type of data input is similar to all statistical packages.

After entering the data, click the icon for testing two populations' means and select

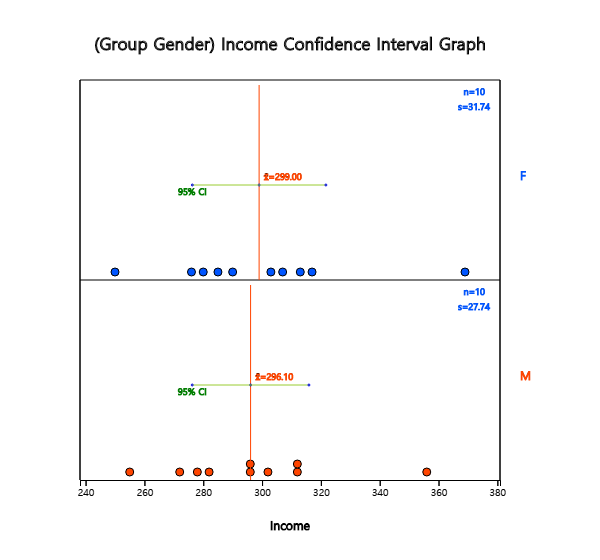

'Analysis Var' as V2 and 'By Group' variable as V1. A 95% confidence interval graph

that compares the sample means of two populations will be displayed as <Figure 5.3.2>.

<Figure 5.3.1> Data input for testing two populations means

<Figure 5.3.2> Dot graph and confidence Intervals by gender for testing two populations means

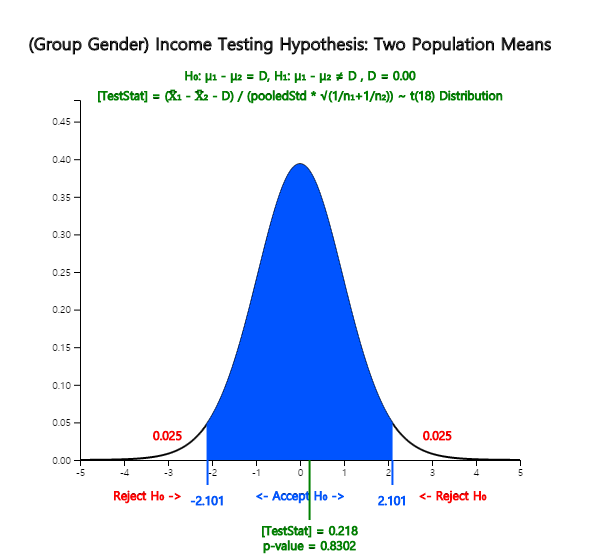

In the options window, as in <Figure 5.3.3> located below the Graph Area,

enter the average difference \(\small D = 0\) for the desired test, select the variance assumption

\(\sigma_1^2 = \sigma_2^2\), the 5% significance level and click the [t-test] button.

Then, the graphical result of the testing hypothesis for two populations' means will be shown

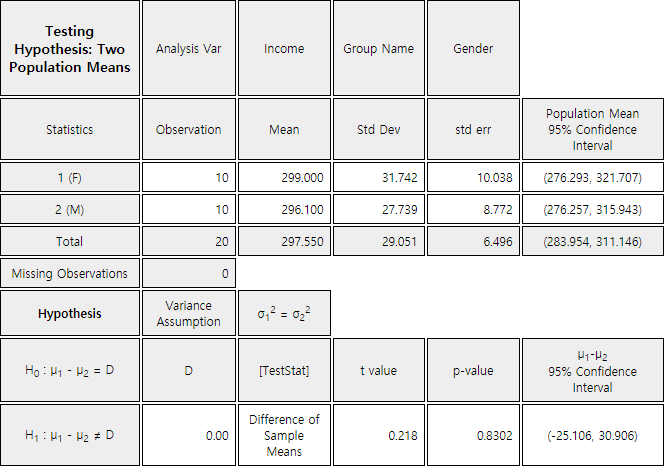

as in <Figure 5.3.4> and the test result as in <Figure 5.3.5>.

<Figure 5.3.3> Options to test for two populations means

<Figure 5.3.4> Testing hypothesis for and – case of the same population variances

<Figure 5.3.5> The result of testing hypothesis for two populations means if population variances are the same

2) Select the variance assumption \(\sigma_1^2 \ne \sigma_2^2\) at the option window and

click [t-test] button under the graph to display the graph of the hypothesis test and

the test result table as in <Figure 5.3.6> and <Figure 5.3.7>.

<Figure 5.3.6> Testing hypothesis for and – case of the different population variances

<Figure 5.3.7> result of testing hypothesis for two populations means if population variances are different

Practice 5.3.1 (Oral Cleanliness by Brushing Methods)

Oral cleanliness scores were examined for eight samples using the basic brushing method (coded 1)

and seven samples using the rotation method (coded 2). The data are saved at the following location of 『eStat』.

Ex ⇨ DataScience ⇨ ToothCleanByBrushMethod.csv

1) If population variances are the same, test the hypothesis at the 5% significance level to determine whether scores for both brushing methods are the same using 『eStat』.

2) If population variances are different, test the hypothesis at the 5% significance level to determine whether scores for both brushing methods are the same using 『eStat』.

5.4 Testing hypothesis for several population means: Analysis of variances

Section 5.3 discussed comparing the means of two populations using the testing hypothesis. This section

discusses comparing the means of several populations. There are many examples of comparing means of several

populations as follows.

- Are average hours of library usage for each grade the same?

- Are yields of three different rice seeds equal?

- In a chemical reaction, are response rates the same at four different temperatures?

- Are the average monthly wages of college graduates the same in three different cities?

The group variable used to distinguish population groups, such as the grade or the rice, is called

a factor.

This section describes the one-way analysis of variance (ANOVA), which compares population means when there is a

single factor. Let us take a look at the following example.

Example 5.4.1

We collected samples randomly from each grade to compare the English proficiency scores of each grade at a university,

and the data are in Table 5.4.1. The last column is the average

\({\overline y}_{1\cdot}\), \({\overline y}_{2\cdot}\), \({\overline y}_{3\cdot}\), \({\overline y}_{4\cdot}\) for each grade.

Table 5.4.1 English Proficiency Score by Grade

Socre

Student 1

Student 2

Student 3

Student 4

Student 5

Student 6

Student Average

Grade 1

81

75

69

90

72

83

\({\overline y}_{1\cdot}\)=78.3

Grade 2

65

80

73

79

81

69

\({\overline y}_{2\cdot}\)=74.5

Grade 3

72

67

62

76

80

\({\overline y}_{3\cdot}\)=71.4

Grade 4

89

94

79

88

\({\overline y}_{4\cdot}\)=87.5

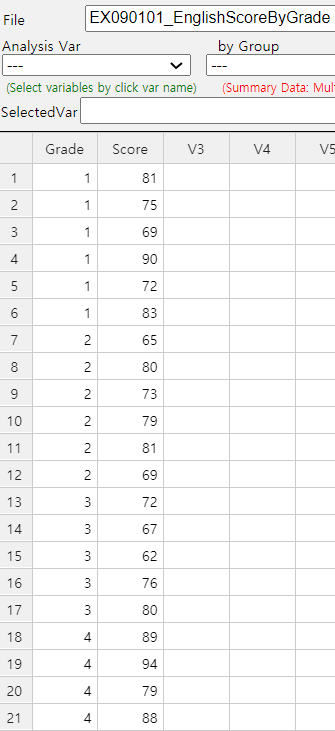

[Ex] ⇨ DataScience ⇨ EnglishScoreByGrade.csv.

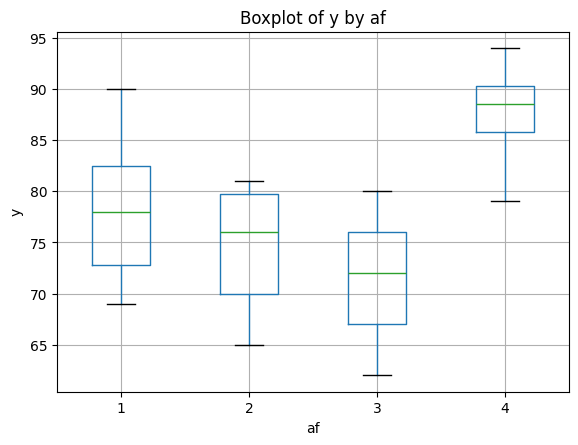

1) Draw a dot graph of test scores for each grade and compare their averages using 『eStat』.

2) Set up a null hypothesis and an alternative hypothesis. Test a hypothesis

whether the average scores of each grade are the same or not.

3) Apply the one-way analysis of variances to test the hypothesis in question 2).

4) Check the result of the ANOVA test using 『eStat』.

Answer

1) Enter data on the sheet to draw a dot graph with data shown in Table 5.4.1 using 『eStat』, and

set variable names to 'Grade' and 'Score' as shown in <Figure 5.4.1>. In the variable selection box

appeared by clicking the ANOVA icon on the main menu of 『eStat』, select 'Analysis Var' as ‘Score’

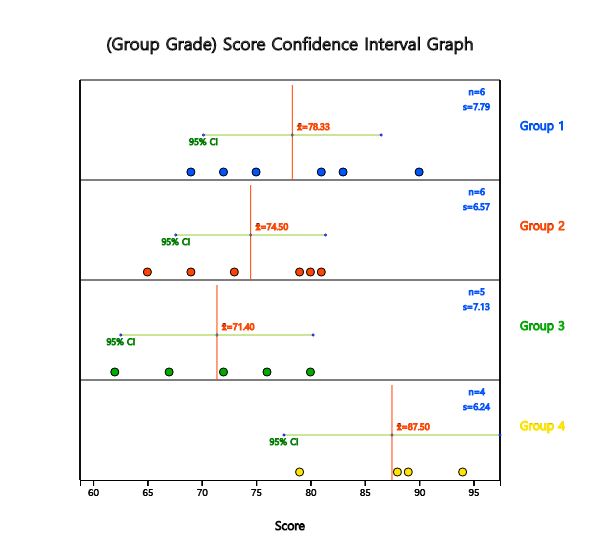

and 'By Group' as ‘Grade’. The dot graph of English scores by each grade and the 95% confidence interval

are displayed in <Figure 5.4.2>.

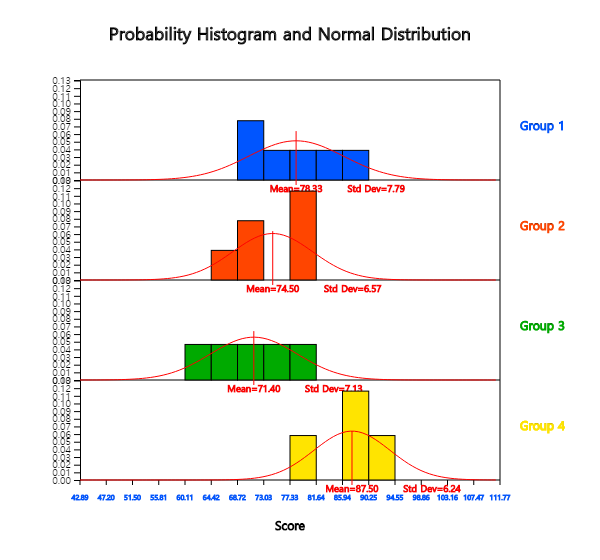

Clicking the 'Confidence Interval Graph' button, we can see a more detailed comparison of the population mean

on each dot graph. <Figure 5.4.2> shows sample means as \({\overline y}_{1\cdot}\)= 78.3,

\({\overline y}_{2\cdot}\) = 74.5, \({\overline y}_{3\cdot}\) = 71.4,

\({\overline y}_{4\cdot}\) = 87.5. The sample mean of the 4th grade is

relatively larger than the other grades and \({\overline y}_{2\cdot}\) and \({\overline y}_{3\cdot}\) are similar.

Therefore, we can expect that the population mean

\(\mu_{2}\) and \(\mu_{3}\) would be the same and \(\mu_{4}\) will differ from three other population means.

However, we need to test whether these differences of sample means are statistically significant.

<Figure 5.4.1> 『eStat』 data input for ANOVA

<Figure 5.4.2> 95% Confidence Interval by grade

Clicking the [Histogram] button under this graph, as in <Figure 5.4.3>, to check the normality of the data will

draw histograms and normal distributions simultaneously, as shown in Figure 5.4.4>

<Figure 5.4.3> Options of ANOVA

<Figure 5.4.4> Histogram of English score by grade

2) In this example, the null hypothesis to test is that the population means of English scores of the four grades

are all the same, and the alternative hypothesis is that the population means of the English scores are not the same.

In other words, if \(\mu_1 , \mu_2 , \mu_3 ,\) and \(\mu_4\) are the population means of English scores

for each grade, the hypothesis to test can be written as follows,

Alternative hypothesis \( \quad \small H_1\): at least one pair of \(\mu_i\) is not the same

3) A measure that can be considered first as a basis for testing differences in multiple sample means would be

the distance from each mean to the overall mean. In other words, if the overall sample mean for all 21 students

is expressed as \(\overline y_{\cdot \cdot}\), the squared distance from each sample mean to the overall mean

is as follows when the number of samples in each grade is weighted. This squared distance is called

the between sum of squares (SSB) or the treatment sum of squares (SSTr).

If the squared distance \(\small SSTr\) is close to zero, all sample means of English scores for four grades are similar.

However, this treatment sum of squares can be larger if the number of populations increases.

Modifications are required to become a test statistic to determine whether several population means are equal.

The squared distance from each observation to its sample mean of the grade is called the within sum of squares (SSW) or

the error sum of squares (SSE) as defined below.

If population distributions of English scores in each grade follow normal distributions and their variances are

the same, the following test statistic has the \(F_{3, 17}\) distribution.

This statistic can be used to test whether or not the population's English scores in four grades are the same.

In the test statistic, the numerator \(\frac{SSTr}{4-1}\) is called the treatment mean square (MSTr),

which implies a variance between

grade means. The denominator \(\frac{SSE}{21-4}\) is called the error mean square (MSE),

which implies a variance within each grade. The MSE is a pooled variance of four sample variances.

Thus, the above test statistics are based on the ratio of two variances, which is why the test of multiple

population means is called an analysis of variance (ANOVA).

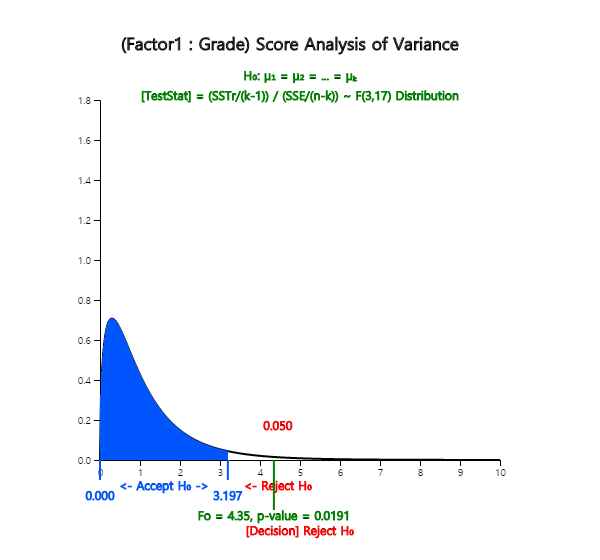

The calculated test statistic, which is the observed \(\small F\) value \(\small F_{0}\), using data of

English scores for each grade is as follows.

Since \(\small F_{3,17;\; 0.05}\) = 3.20, the null hypothesis that population means of English scores

of each grade are the same, \(\small H_0 : \mu_1 = \mu_2 = \mu_3 = \mu_4 \), is rejected at the 5% significance level.

In other words, there is a difference in population means of English scores of each grade.

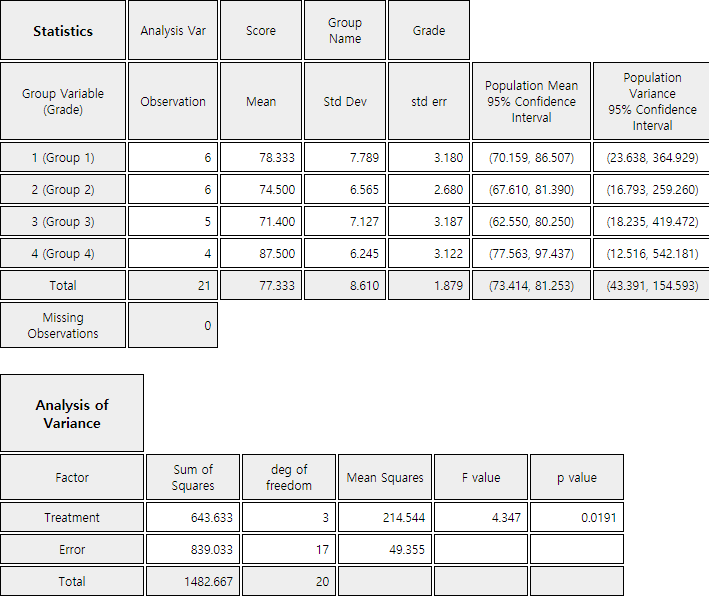

The following ANOVA table provides a single view of the above calculation.

Factor

Sum of Squares

Degree of freedom

Mean Squares

F ratio

Treatment

SSTr = 643.633

4-1

MSTr = \(\frac{643.633}{3}\)

\(F_0 = 4.347\)

Error

SSE = 839.033

21-4

MSE = \(\frac{839.033}{17}\)

Total

SST = 1482.666

20

4) In <Figure 5.4.3>, if you select the significance level of 5%, the confidence level of 95%,

and click [ANOVA F test] button, a graph showing the location of the test statistic in the F distribution

is appeared as shown in <Figure 5.4.5>. Also, in the Log Area, the mean and confidence interval tables

and test results for each grade appear in <Figure 5.4.6>.

<Figure 5.4.5> 『eStat』 ANOVA F test

<Figure 5.4.6> 『eStat』 Basic Statistics and ANOVA table

The analysis of variance is also possible using 『eStatU』 as below. Entering the data as below,

and clicking the [Execute] button will have the same result as in <Figure 5.4.5> and <Figure 5.4.6>.

[Testing Hypothesis : 3+ Population Means (ANOVA)]

The above example refers to two variables: the English score and grade. The variable, such as the English score, is

called an analysis variable or a response variable. The response variable is mostly a continuous variable. The

variable used to distinguish populations, such as the grade, is called a group variable or a factor variable, which

is mostly a categorical variable. Each value of a factor variable is called a level of the factor, and the number

of these levels is the number of populations to be compared. In the above example, the factor has four levels,

1st, 2nd, 3rd and 4th grade. The term 'response' or 'factor' is originated to analyze data

in engineering, agriculture, medicine, and pharmacy experiments.

The analysis of variance method that examines the effect of a single factor on the response variable is called the

one-way ANOVA. Table 5.4.2 shows the typical data structure of the one-way ANOVA when the number of levels of a

factor is \(k\), and the numbers of observations at each level are \(n_1 , n_2 , ... , n_k\).

Table 5.4.2 Notation of the one-way ANOVA

Factor

Observed values of sample

Average

Level 1

\(Y_{11} \; Y_{12}\; \cdots \;Y_{1n_1} \)

\(\overline Y_{1\cdot}\)

Level 2

\(Y_{21} \; Y_{22}\; \cdots \;Y_{2n_2} \)

\(\overline Y_{2\cdot}\)

\(\cdots\)

\(\cdots\)

\(\cdots\)

Level k

\(Y_{k1} \; Y_{k2}\; \cdots \;Y_{kn_k} \)

\(\overline Y_{k\cdot}\)

Total

\( {\overline Y}_{\cdot \cdot} \)

Statistical model for the one-way analysis of variance is given as follows.

$$

\begin{align}

Y_{ij} &= \mu_i + \epsilon_{ij} \\

&= \mu + \alpha_i + \epsilon_{ij}, \;i=1,2,...,k; \;j=1,2,..., n_i \\

&\text{where}\;\; \epsilon_{ij} \backsim N(0, \sigma ^2)

\end{align}

$$

\(Y_{ij}\) represents the \(j^{th}\) observed value of the response variable for the \(i^{th}\) level of factor.

The population mean of the \(i^{th}\) level, \(\mu_{i}\), is represented as \(\mu + \alpha_{i}\) where \(\mu\)

is the mean of entire population and \(\alpha_{i}\) is the effect of \(i^{th}\) level for the response

variable. \(\epsilon_{ij}\) denotes an error term of the \(j^{th}\) observation

for the \(i^{th}\) level, and the all error terms are assumed independent of each other and follow

the same normal distribution with the mean 0 and variance \(\sigma^{2}\).

The error term \(\epsilon_{ij}\) is a random variable in the response variable due to reasons other than levels of the factor.

For example, in the English score example, differences in English performance for each grade can be caused

by other variables besides the variables of grade, such as individual study hours, gender and IQ.

However, by assuming that these variations are relatively small compared to variations due to differences in grade, the

error term can be interpreted as the sum of these various reasons.

The hypothesis to test can be represented using \(\alpha_{i}\) instead of \(\mu_{i}\) as follows.

Alternative hypothesis \( \quad H_1\): at least one \(\alpha_i\) is not equal to 0

The analysis of variance table as Table 5.4.3 is used to test the hypothesis.

Table 5.4.3 Analysis of variance table of the one-way ANOVA

Factor

Sum of Squares

Degree of freedom

Mean Squares

F ratio

Treatment

SSTr

\(k-1\)

MSTr=\(\frac{SSTr}{k-1}\)

\(F_0 = \frac{MSTr}{MSE}\)

Error

SSE

\(n-k\)

MSE=\(\frac{SSE}{n-k}\)

Total

SST

\(n-1\)

where \(\qquad n = \sum_{i=1}^{n} \; n_i\)

The three sum of squares for the analysis of variances can be described as follows.

SST = \(\sum_{i=1}^{k} \sum_{j=1}^{n_i} ( Y_{ij} - {\overline Y}_{\cdot \cdot} )^2 \;\) :

The sum of squared distances between observed values of the response variable and the mean of total observations

is called the total sum of squares (SST).

SSTr = \(\sum_{i=1}^{k} \sum_{j=1}^{n_i} ( {\overline Y}_{i \cdot} - {\overline Y}_{\cdot \cdot} )^2 \;\) :

The sum of squared distances between the mean of each level and the mean of total observations is called the

treatment sum of squares (SSTr). It represents the variation between level means.

SSE = \(\sum_{i=1}^{k} \sum_{j=1}^{n_i} ( {Y}_{ij} - {\overline Y}_{i \cdot} )^2 \;\) :

The sum of squared distances between observations of the \(i^{th}\) level and the mean of the \(i^{th}\) level is referred to as

'within variation', and is called the error sum of squares (SSE).

The following logic determines the degree of freedom of each sum of squares.

The SST consists of \(n\) number of squares, \(( Y_{ij} - {\overline Y}_{\cdot \cdot} )^2\),

but \( {\overline Y}_{\cdot \cdot} \) should be calculated first, before SST is calculated,

and hence the degree of freedom of SST is \(n-1\). The SSE consists of \(n\) number of squares,

\(( {Y}_{ij} - {\overline Y}_{i \cdot} )^2 \), but the number of values,

\({\overline Y}_{1 \cdot}, {\overline Y}_{2 \cdot}, ... , {\overline Y}_{k \cdot}\)

should be calculated first before SSE is calculated, and hence, the degree of freedom of SSE is \(n-k\).

The degree of freedom of SSTr is calculated as the degree of freedom of SST minus the degree of freedom of

SSE, which is \(k-1\). In the one-way analysis of variance, the following partition of the sum of

squares and degree of freedom are always established;

Sum of squares: SST = SSTr + SSE

Degrees of freedom: \((n-1) = (k-1) + (n-k)\)

The sum of squares divided by the corresponding degrees of freedom is referred to as the mean squares, and Table

5.4.3 defines the treatment mean squares (MSTr) and error mean squares (MSE).

The treatment mean square implies the average variation between each level of the factor, and the error

mean square implies the average variation within observations in each level. Therefore, if MSTr is relatively

much larger than MSE, we can conclude that the population means of each level, \(\mu_i\), are not the same. So by what

criteria can you say it is relatively much larger?

The calculated \(F\) value, \(F_0\), in the last column of the ANOVA table represents the relative size of MSTr and MSE. If

the assumptions of \(\epsilon_{ij}\) are satisfied, and if the null hypothesis

\(\small H_0 : \alpha_1 = \alpha_2 = \cdots = \alpha_k \) = 0 is true, then the

test statistic follows a \(F\) distribution with degrees of freedoms \(k-1\) and \(n-k\).

$$

F_{0} = \frac { \frac{SSTr}{(k-1)} } { \frac{SSE}{(n-k)} }

$$

Therefore, when the significance level is \(\alpha\) for a test, if the calculated value \(F_0\) is greater

than the value of \(F_{k-1,n-k; α}\), then the null hypothesis is rejected. That is,

it is determined that the population means of each factor level are different.

(Note: 『eStat』 calculates this test's \(p\)-value. Hence, if the \(p\)-value is smaller than

the significance level \(\alpha\), then reject the null hypothesis.)

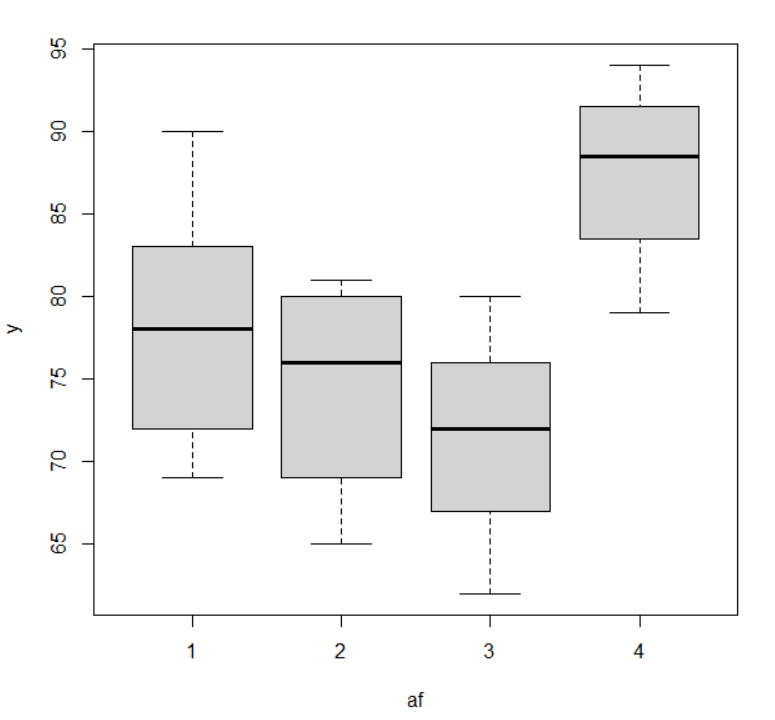

Practice 5.4.1(Plant Growth by Condition)

Results from an experiment to compare yields (as measured by the dried weight of plants) obtained under a control

(leveled ‘ctrl’) and two treatment conditions (leveled ‘trt1’ and ‘trt2’). The weight data with

30 observations on control and two treatments (‘crtl’, ‘trt1’, ‘trt2’), are saved at the following location

of 『eStat』. Answer the following using 『eStat』 ,

[Ex] ⇨ DataScience ⇨ PlantGrowth.csv

1) Draw a dot graph of weights for each control and treatment.

2) Test a hypothesis whether the weights are the same or not. Use the 5% significance level.

5.5 Regression analysis

5.5.1 Correlation analysis

Sample correlation coefficient \(r\) can be used for testing the hypothesis of a population

correlation coefficient \(\rho\). We test usually \(H_0 : \rho = 0\)

which tests the existence of linear correlation. This test can be done using \(t\) distribution

as follows.

Testing a population correlation coefficient

Null hypothesis: \(H_0 : \rho = 0\)

Test statistic: \(\quad t_0 = \sqrt{n-2} \frac{r}{\sqrt{1 - r^2 }}\)

follows \(t\) distribution with \(n-2\) degrees of freedom

We can also test a hypothesis \(H_0 : \rho = \rho_0\) when \(\rho_0 \ne 0\), but please refer other statistics book.

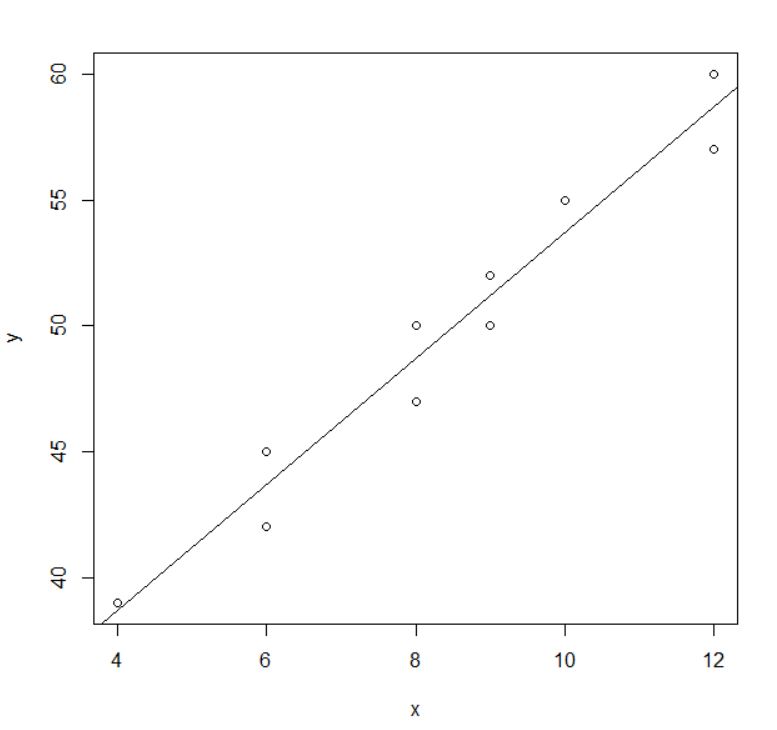

Example 5.5.1

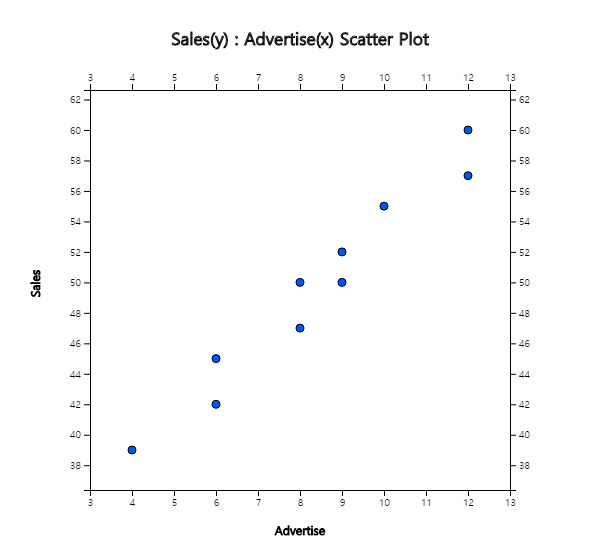

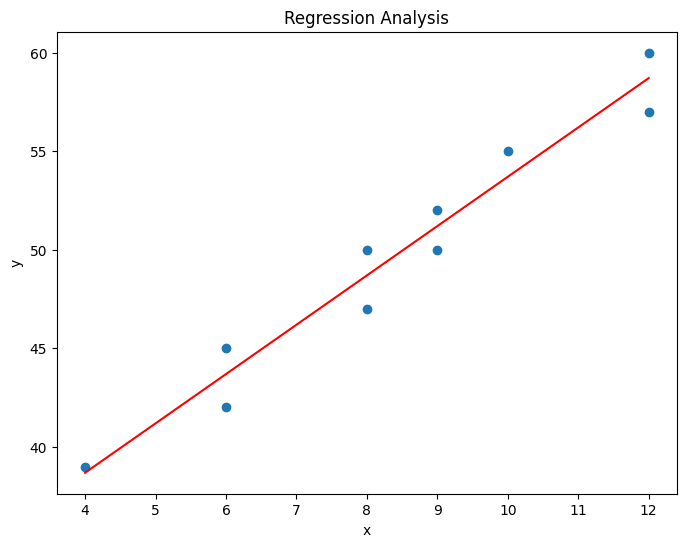

Based on the survey of advertising costs and sales for 10 companies that make the same product,

we obtained the following data as in Table 5.5.1. Draw a scatter plot for this data using 『eStat』,

and find the sample correlation coefficient of the two variables. Test the hypothesis that

the population correlation coefficient is zero with the significance level 0.05.

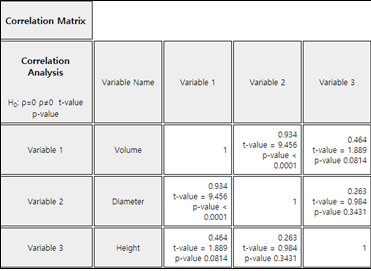

Table 5.5.1 Advertising costs and sales (unit: 1 million USD)

Company

Advertise (X)

Sales (Y)

1

4

39

2

6

42

3

6

45

4

8

47

5

8

50

6

9

50

7

9

52

8

10

55

9

12

57

10

12

60

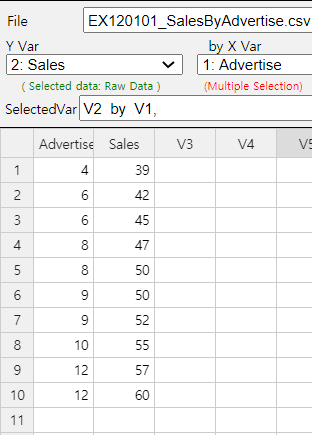

[Ex] ⇨ DataScience ⇨ SalesByAdvertise.csv.

Answer

Using 『eStat』 , enter data as shown in <Figure 5.5.1>. If you select the Sales as 'Y Var' and the

Advertise 'by X Var' in the variable selection box that appears when you click the scatter plot icon on the

main menu, the scatter plot will appear as shown in <Figure 5.5.2>. As we can expect, the scatter

plot show that the more investments in advertising, the more sales increase, and not only that, the form of

increase is linear.

<Figure 5.5.1> Data input in 『eStat』

<Figure 5.5.2> Scatter plot of sales by advertise

To calculate the sample covariance and correlation coefficient, it is convenient to make the following table.

This table can also be used for calculations in regression analysis.

Table 5.5.1 A table for calculating the covariance and correlation coefficient

Number

\(X\)

\(Y\)

\(X^2\)

\(Y^2\)

\(XY\)

1

4

39

16

1521

156

2

6

42

36

1764

252

3

6

45

36

2025

270

4

8

47

64

2209

376

5

8

50

64

2500

400

6

9

50

81

2500

450

7

9

52

81

2704

468

8

10

55

100

3025

550

9

12

57

144

3249

684

10

12

60

144

3600

720

Sum

64

497

766

25097

4326

Mean

8.4

49.7

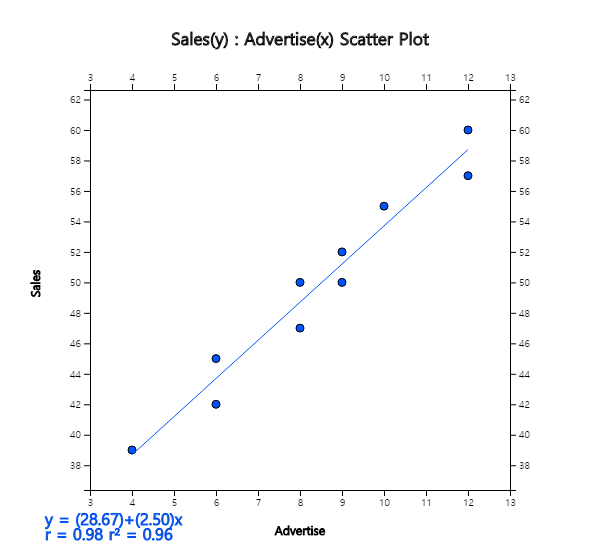

Terms which are necessary to calculate the covariance and correlation coefficient are as follows:

\(\small SXX, SYY, SXY \)represent the sum of squares of \(\small X\), the sum of squares of

\(\small Y\), the sum of squares of \(\small XY\). Hence, the covariance and

correlation coefficient are as follows:

\(\small \quad S_{XY} = \frac{1}{n-1} \sum_{i=1}^{n} (X_i - \overline X )(Y_i - \overline Y ) = \frac{151.2}{10-1} = 16.8 \)

\(\small \quad r = \frac {\sum_{i=1}^{n} (X_i - \overline X )(Y_i - \overline Y )} { \sqrt{\sum_{i=1}^{n} (X_i - \overline X )^{2} \sum_{i=1}^{n} (Y_i - \overline Y )^{2} } } = \frac{151.2} { \sqrt{ 60.4 × 396.1 } } = 0.978 \)

This sample correlation coefficient is consistent with the scatter plot which shows a strong positive

correlation of the two variables.

The value of the test statistic \(t_0\) is as follows.

Since it is greater than \(t_{8;\; 0.025}\) = 2.306, \(\small H_0 : \rho = 0\) should be rejected.

The correlation analysis can be done using 『eStatU』 by following data input and clicking [Execute] button..

[]

Practice 5.5.1

A professor of statistics argues that a student's final test score can be predicted from his midterm score.

Ten students were randomly selected, and their mid-term and final exam scores are as follows.

id

Mid-term X

Final Y

1

92

87

2

65

71

3

75

75

4

83

84

5

95

93

6

87

82

7

96

98

8

53

42

9

77

82

10

68

60

[Ex] ⇨ DataScience ⇨ MidtermFinal.csv.

1) Draw a scatter plot of this data with the X-axis mid-term and Y-axis final scores. What do you think is the relationship between mid-term and final scores?

2) Find the sample correlation coefficient and test the hypothesis that the population correlation

coefficient is zero with a significance level 0.05.

5.5.2 Simple linear regression

Data are concentrated around a straight line when two variables show a strong correlation.

In this case, linear regression analysis is a statistical model to estimate the straight line

which describes the data's relationship suitably. The estimated model can be applied to the forecasting analysis.

For example, a mathematical model of the relationship between

sales (\(\small Y\)) and advertising costs (\(\small X\)) would not only explain the relationship between sales

and advertising costs but would also be able to predict the sales for a given investment for advertisement.

As such, the regression analysis is intended to investigate and predict the degree of relation

between variables and the shape of the relation.

In regression analysis, a mathematical model of

the relation between variables is called a regression equation, and the variable affected

by other related variables is called a dependent variable. The dependent variable is

the variable we would like to describe, which is usually observed in response to other variables,

so it is also called a response variable. In addition, variables that affect the dependent

variable are called independent variables. The independent variable is also referred to

as the explanatory variable because it is used to describe the dependent variable.

In the previous example, if the objective is to analyze the change in sales amounts resulting

from increases and decreases in advertising costs, the sales is a dependent variable, and

the advertising cost is an independent variable.

If the number of independent variables included in the regression equation is one, it is called a

simple linear regression. If the number of independent variables is two or more, it is called a

multiple linear regression, explained in section 5.5.3.

Simple linear regression analysis has only one independent variable, and the regression equation is

as follows.

$$

Y = f(X,\alpha,\beta) = \alpha + \beta X

$$

In other words, the regression equation is represented by a linear equation of the independent variable,

and \(\alpha\) and \(\beta\) are unknown parameters that represent the intercept and slope, respectively.

The \(\alpha\) and \(\beta\) are called the regression coefficients. The above equation represents

an unknown linear relationship between \(Y\) and \(X\) in population and is referred to as

the population regression equation.

To estimate the regression coefficients \(\alpha\) and \(\beta\), observations of the dependent

and independent variables are required, i.e., samples. In general, all of these observations are not

located in a line. It is because, even if the \(Y\) and \(X\) have an exact linear relation,

there may be a measurement error in the observations, or there may not be an exact linear relationship

between \(Y\) and \(X\). Therefore, we can write the regression formula by considering these errors

as follows.

$$

Y_i = \alpha + \beta X_i + \epsilon_{i}, \quad i=1,2,...,n

$$

Where \(i\) is the subscript representing the \(i^{th}\) observation, and \(\epsilon_i\) is the

random variable indicating an error with a mean of zero and a variance \(\sigma^2\) which is

independent of each other. The error \(\epsilon_i\) indicates that the observation \(Y_i\) is

how far away from the population regression equation. The above equation includes unknown population

parameters \(\alpha\), \(\beta\), and \(\sigma^2\) and is referred to as a population

regression model.

If \(a\) and \(b\) are the estimated regression coefficients using samples, the fitted regression equation

can be written as follows. It is referred to as the sample regression equation.

$$

{\hat Y}_i = a + b X_i

$$

In this expression, \({\hat Y}_i\) represents the estimated value of \(Y\) at \(X=X_i\) as predicted

by the appropriate regression equation. These predicted values can not match the actual observed values

of \(Y\), and differences between these values are called residuals and denoted as \(e_i\).

$$

\text{residuals} \qquad e_i = Y_i - {\hat Y}_i , \quad i=1,2,...,n

$$

The regression analysis makes assumptions about the unobservable error \(\epsilon_i\).

Since the residuals \(e_i\) calculated using the sample values have similar characteristics as

\(\epsilon_i\), they are used to investigate the validity of these assumptions.

When sample data, \(\small (X_1 , Y_1 ) , (X_2 , Y_2 ) , ... , (X_n , Y_n ) \), are given, a straight line

representing it can be drawn in many ways. Since one of the main objectives of a regression analysis is

prediction, we would like to use the estimated regression line that would make the residuals smallest

that the error occurs when predicting the value of Y. However, it is impossible to minimize the residuals'

value at all points, and it should be chosen to make the residuals 'totally' smaller.

The most widely used of these methods is a method that minimizes the total sum of squared residuals,

called a method of least squares.

Method of least squares

A method of estimating regression coefficients so that the total sum of the squared errors occurring

in each observation is minimized. i.e.,

To obtain the values of \(\alpha\) and \(\beta\) by the least squares method, the sum of squares

above should be differentiated partially with respect to \(\alpha\) and \(\beta\), and equate them zero

respectively. If the solution of \(\alpha\) and \(\beta\) of these equations is \(a\) and \(b\),

the equations can be written as follows.

$$

\begin{align}

a \cdot n + b \sum_{i=1}^{n} X_i &= \sum_{i=1}^{n} Y_i \\

a \sum_{i=1}^{n} X_i + b \sum_{i=1}^{n} X_i^2 &= \sum_{i=1}^{n} X_i Y_i \\

\end{align}

$$

The above expression is called a normal equation. The solution \(a\) and \(b\) of this normal

equation is called a least squares estimator of \(\alpha\) and \(\beta\), and is given as follows.

$$

\begin{align}

b &= \frac {\sum_{i=1}^{n} (X_i - \overline X ) (Y_i - \overline Y )} { \sum_{i=1}^{n} (X_i - \overline X )^2 } \\

a &= \overline Y - b \overline X

\end{align}

$$

After estimating the regression line, how valid it is should be investigated. Since a regression analysis

aims to describe a dependent variable as a function of an independent variable,

it is necessary to find out how much the explanation is. A residual standard error and a coefficient of

determination are used for such validation studies.

Residual standard error \(s\) measures the extent to which observations are scattered around

the estimated line. First, you can define the sample variance of residuals as follows.

$$

s^2 = \frac{1}{n-2} \sum_{i=1}^{n} ( Y_i - {\hat Y}_i )^2

$$

The residual standard error \(s\) is the square root of \(s^2\). The \(s^2\) is an estimate of

\(\sigma^2\) which is the extent that the observations \(Y\) are spread around the population regression

line. A small value of \(s\) or \(s^2\) indicates that the

observations are close to the estimated regression line, which in turn implies that the regression line represents well the

relationship between the two variables.

However, it is not clear how small the residual standard error \(s\) is, although the smaller the value is,

the better. In addition, the size of the value of \(s\) depends on the unit of \(Y\). A relative measure

called the coefficient of determination is defined to eliminate this shortcoming. The coefficient

of determination is the ratio of the variation described by the regression line over the total

variation of observation \(Y_i\), so that it is a relative measure that can be used regardless of the

type and unit of a variable.

As in the analysis of variance in the previous section, the following partitions of the sum of squares and degrees of

freedom are established in the regression analysis:

$$

\begin{align}

\text{Sum of squares:} \qquad \;\; SST \;=\; SSE \;+\; SSR \\

\text{Degrees of freedom:} \quad (n-1) = (n-2) + 1

\end{align}

$$

Description of the above three sums of squares is as follows.

Total sum of squares : \( \small SST = \sum_{i=1}^{n} ( Y_i - {\overline Y} )^2\)

The total sum of squares indicating the total variation in observed values of \(\small Y\) is called the

total sum of squares (\(\small SST\)). This \(\small SST\) has the degree of freedom, \(n-1\), and if \(\small SST\)

is divided by the degree of freedom, it becomes the sample variance of \(\small Y_i\).

Error sum of squares : \( \small SSE = \sum_{i=1}^{n} ( Y_i - {\hat Y}_i )^2\)

The error sum of squares (\(\small SSE\)) of the residuals represents the unexplained variation of the

total variation of the \(\small Y\). Since the calculation of this sum of squares requires the estimation of

two parameters \(\alpha\) and \(\beta\), \(\small SSE\) has the degree of freedom \(n-2\).

This is the reason why, in the calculation of the sample variance of residuals \(s^2\), it was divided

by \(n-2\).

Regression sum of squares : \( \small SSR = \sum_{i=1}^{n} ( {\hat Y}_i - {\overline Y} )^2 \)

The regression sum of squares (\(\small SSR\)) indicates the variation explained by the regression line

among the total variation of \(\small Y\). This sum of squares has the degree of freedom of 1.

If the estimated regression equation fully explains the variation in all samples (i.e., if all

observations are on the sample regression line), the unexplained variation \(\small SSE\) will be zero. Thus,

if the portion of \(\small SSE\) is small among the total sum of squares \(\small SST\), or if the portion of

\(\small SSR\) is large, the estimated regression model is more suitable. Therefore, the ratio of \(\small SSR\)

to the total variation \(\small SST\), called the coefficient of determination, is defined as a

measure of the suitability of the regression line as follows.

$$ \small

R^2 = \frac{Explained \;\; Variation}{Total \;\; Variation} = \frac{SSR}{SST}

$$

The value of the coefficient of determination is always between 0 and 1, and the closer the value is to 1,

the more concentrated the samples are around the regression line, which means that the estimated

regression line explains the observations well.

If we divide three sums of squares obtained in the above example by their degrees of freedom, each

becomes a variance. For example, if you divide the \(\small SST\) by \(n-1\) degrees of freedom,

then it becomes the sample variance of the observed values \(Y_1 , Y_2 , ... , Y_n\). If you divide

the \(SSE\) by \(n-2\) degrees of freedom, it becomes \(s^2\) which is an estimate of the variance

of error \(\sigma^2\). For this reason, addressing the problems associated with the regression

using the partition of the sum of squares is called the ANOVA of regression. Information required

for ANOVA, such as a calculated sum of squares and degrees of freedom, can be compiled in the ANOVA

table, as shown in Table 5.5.2.

Table 5.5.2 Analysis of variance table for simple linear regression

Source

Sum of squares

Degrees of freedom

Mean Squares

F value

Regression

SSR

1

MSR =\(\frac{SSR}{1}\)

\(F_0 = \frac{MSR}{MSE}\)

Error

SSE

\(n-2\)

MSE = \(\frac{SSE}{n-2}\)

Total

SST

\(n-1\)

The sum of squares divided by its degrees of freedom is referred to as mean squares, and Table 5.5.2

defines the regression mean squares (\(\small MSR\)) and error mean squares (\(\small MSE\)) respectively. As the

expression indicates, \(\small MSE\) is the same statistic as \(s^2\) which is the estimate of \(\sigma^2\).

The \(\small F\) value given in the last column is used for testing the hypothesis

\(\small H_0: \beta = 0 ,\; H_1 : \beta \ne 0 \). If \(\small \beta\) is not 0, the \(\small F\) value

can be expected to be large because the assumed regression line is valid and the variation of

\(\small Y\) is explained

in large part by the regression line. Therefore, we can reversely decide that \(\small \beta\) is not zero

if the calculated \(\small F\) ratio is large enough. If the assumptions about the error terms mentioned

in the population regression model are valid and if the error terms follow a normal distribution,

the distribution of \(\small F\) value, when the null hypothesis is true, follows \(\small F\) distribution

with 1 and \(n-2\) degrees of freedom. Therefore, if \(\small F_0 > F_{1,n-2;\; α}\), then we can reject

\(\small H_0 : \beta = 0\).

(In 『eStat』, the \(p\)-value for this test is calculated, and the decision can be made using this

\(p\)-value. That is, if the \(p\)-value is less than the significance level, the null hypothesis

\(\small H_0\) is rejected.)

One assumption of the error term \(\epsilon\) in the population regression model is that it follows

a normal distribution with a mean of zero and variance of \(\sigma^2\). Under this assumption,

the regression coefficients and other parameters can be estimated and tested. Note that, under the

assumption above, the regression model \(Y = \alpha + \beta X + \epsilon \) follows a normal

distribution with the mean \(\alpha + \beta X \) and variance \(\sigma^2\).

1) Inference on the parameter \(\; \beta\)

The parameter \(\beta\), the slope of the regression line, indicates the existence and extent

of a linear relationship between the dependent and the independent variables. The inference for \(\beta\)

can be summarized as follows. The test for hypotheses \(H_0 : \beta = 0\) is used to determine

the independent variable describes the dependent variable significantly or not. The \(F\) test for the hypothesis

\(H_0 : \beta = 0\) described in the ANOVA of regression is theoretically the same as in the test below.

Point estimate: \(\small \quad b = \frac {\sum_{i=1}^{n} (X_i - \overline X) (Y_i - \overline Y)} { \sum_{i=1}^{n} (X_i - \overline X)^2 } , \quad b \sim N(\beta, \frac{\sigma^2} {\sum_{i=1}^{n} (X_i - \overline X )^2 } ) \)

Standard error of estimate \(b\): \(\small \quad SE(b) = \frac{s}{\sqrt {{\sum_{i=1}^{n} (X_i - \overline X)^2} } }\)

Confidence interval of \(\; \beta\): \(\quad b \pm t_{n-2; α/2} \cdot SE(b)\)

2) Inference on the parameter \(\; \alpha\)

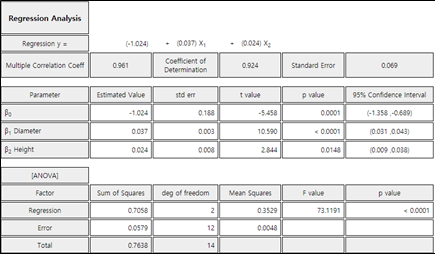

The inference for the parameter \(\alpha\), which is the intercept of the regression line, can be