Chapter 6. Supervised machine learning for categorical data

CHAPTER OBJECTIVES

The classification analysis technique uses data with known group membership

to create a model to determine the data group with unknown group membership. It has been used in traditional Statistics.

Many new models similar to the classification analysis have been developed to train a computer

for artificial intelligence.

All these models for classification are called models for 'supervised machine learning.'

We introduce the following in this chapter.

• Basic concepts of supervised machine learning and introduce classification analysis models in section 6.1.

• Decision tree model for categorical data in section 6.2.

• General Bayes classification model, a basic statistical classification analysis,

and the naive Bayes classification model for categorical data in section 6.2.

• Evaluation of classification model and comparison methods for several classification models.

6.1 Basic concepts of supervised machine learning and classification

Supervised machine learning is a technique that uses data with known group affiliation to create

a model to determine the group of data whose group affiliation is unknown. It is called as

discriminant analysis or

classification analysis in traditional statistics.

In contrast, a technique that determines groups of similar data using data with unknown group affiliation

is called

cluster analysis or

unsupervised machine learning. A supervised machine learning model

is applied in various fields, such as when a doctor examines a patient and classifies the patient's

diagnosis based on the examination record, when spam mail is filtered out using email subject lines,

and when a customer visiting a department store is identified as a customer who will purchase a product.

A standard method to classify data whose group affiliation is unknown into a group would be

to classify it into the group that is the ‘closest’ to that data.

Many methods define 'closeness' as being from one data source to a group.

For example, the Euclid distance from the data

to the mean of each group, the Minkowski distance, or the Mahalanobis distance,

a statistical measure that considers the variance of the data, can be used. If we consider

a probabilistic approach, there may be a method to estimate the distribution function of each group

and classify data whose group affiliation is unknown into the group it is likely to belong to.

There are many classification models based on various reasonable criteria. In this chapter,

we focus on statistical models for discrete data, such as the decision tree model and the naive Bayes classification model.

Chapter 7 discusses other classification models for continuous data,

such as the k-nearest neighbor model, the neural network model, the support vector machine model, and the ensemble model.

Classification analysis procedure

Assume that there are \(K\) number of groups (or classes) and \(n_1 , n_2 , ... , n_K\) data

were observed in each group. Let \(\boldsymbol x = (x_1 , x_2 , ... , x_m )\) be the observed data of

the random variable \(\boldsymbol X = (X_1 , X_2 , ... , X_m )\). <Figure 6.1.1> shows

the general process of the classification analysis.

Data cleaning and division

Collect data from each group, clean and transform it, and divide the data into training and test data.

|

| ↓ ↑ |

Training the model

Establish a classification model \(y = f( \boldsymbol x ) \) using the training data.

|

| ↓ ↑ |

Validation of the model

Validate the classification model using the testing data.

|

| ↓ |

Apply the model

Classify data whose group affiliation is unknown into one group using the classification model.

|

<Figure 6.1.1> General process of classification analysis

First, data is collected, refined, and transformed appropriately for analysis. Then, the observed data

in each group is divided into training data and testing data. Using the training data, establish

a classification model \(y = f( \boldsymbol x ) \) where \(y\) is the target variable to be estimated,

which means the group. The validity of the model is examined using the testing data.

If this model is not satisfactory, another model is established again, and its validity is examined.

After comparing several classification models and selecting the most satisfactory classification model,

this model is applied to data whose group is unknown to determine which group to classify.

If the variable that represents each group is considered as a dependent variable and the variable

used to classify each group is considered as an independent variable, classification analysis is

similar to regression analysis. However, in regression analysis, the dependent variable is

a random variable that follows a normal distribution, and the levels of the independent variables

are assumed to be given constants, but classification analysis does not make this assumption,

so there is a difference in the model.

Preparation of data for classification analysis

Data for classification analysis should be prepared in advance to improve classification accuracy,

efficiency, and scalability.

A. Data cleaning

If there is noise in the data, it is recommended to remove it. If there are missing values,

it is recommended to preprocess using the corresponding variable's average or mode.

B. Relevance analysis

Among the variables in the data, there may be variables that are not related to classification,

or the variables may be duplicated. Relevance analysis can be used to remove irrelevant or

duplicated variables, improving the classification model's efficiency and accuracy.

C. Data transformation

Continuous data may need to be discretized for classification.

The neural network model requires converting the units of variable values,

such as from -1.0 to 1.0 or from 0.0 to 1.0.

6.1.1 Evaluation measures of classification model

Suppose there are two groups \(\small G_1 , G_2\), and there are \(n\) number of data whose group affiliation is known.

If a classification model is used to classify each data,

the actual group of data and the group classified by the model can be compared and summarized in Table 6.1.1.

| Table 6.1.1 Table for the test results of the actual group and the classified group |

|

|

Classified group |

|

|

|

\(\small G_1\) |

\(\small G_2\) |

Total |

| Actual group |

\(\small G_1\) |

\(\small f_{11}\) |

\(\small f_{12}\) |

\(\small f_{11} + f_{12}\) |

| \(\small G_2\) |

\(\small f_{21}\) |

\(\small f_{22}\) |

\(\small f_{21} + f_{22}\) |

|

Total |

|

|

\(n\) |

Here, \(f_{ij}\) means the number of data of the group \(G_i\) classified into the group \(G_j\).

The number of data correctly classified out of the total data is \(f_{11} + f_{22}\), and the number of data

incorrectly classified is \(f_{12} + f_{21}\). The

accuracy of the classification model

is defined as the ratio of the number of correctly classified data out of the total number of data,

and the

error rate is defined as the ratio of the number of incorrectly classified data

out of the total number of data.

$$

\begin{align}

\text{Accuracy} &= \frac{f_{11} + f_{22}}{n} \\

\text{Error rate} &= \frac{f_{12} + f_{21}}{n}

\end{align}

$$

Generally, classification models strive to find an algorithm that maximizes accuracy or

minimizes error rate. Accuracy and error rate are reasonable criteria assuming that each data

belongs to one group. However, there is a possibility that one data belongs to more than one group,

in which case it is reasonable to predict the probability of belonging to the group.

There are various measures other than accuracy and error rate to evaluate a classification model,

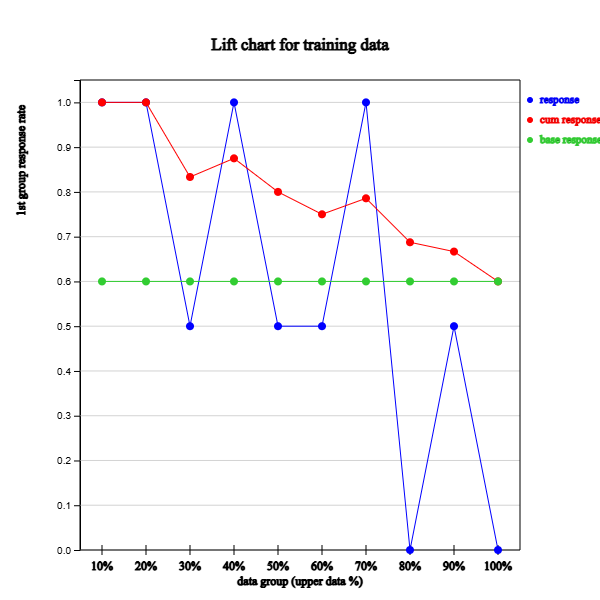

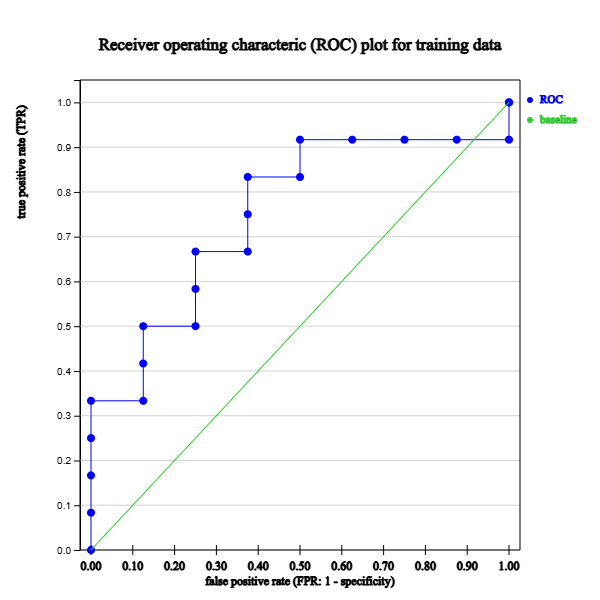

and lift charts, ROC graphs, and statistical analysis methods are used to compare and evaluate various

classification models, which are explained in detail in Section 6.4.

6.1.2 Spliting method for training and testing data

To objectively evaluate a classification model, the entire data set is generally divided

into training data and testing data. The model is established using the training data, and the accuracy

of the model is evaluated using the testing data. If there is sufficient data, validation data is set aside

to improve the performance of the model. This section introduces commonly used methods for dividing

training and testing data.

A. Holdout Method and Random Subsampling

The

holdout method first divides the entire data set into two non-overlapping data sets

and holding out one as training data and the other as testing data. The holdout method is

a widely used method in which a classification model is established using the training data,

and this model is applied to the testing data to measure the accuracy (or error rate).

The ratio at which training and test data are divided depends on the researcher's judgment,

but the most commonly used method is (1/2 training: 1/2 test) or (2/3 training: 1/3 test).

When extracting data at a determined ratio, a simple random sampling method without replacement is used

to reduce bias. The following should be noted when using the reserve method.

1) Since a portion of the entire data for which the group is known is reserved as test data,

there is a risk that the absolute number of training data for establishing the classification model

will be small. In this case, the classification model created with only the training data may not be

as good as the model created using all the data.

2) The classification model may vary depending on how the training and test data are divided.

In general, the smaller the number of training data, the greater the variance in the accuracy of the model.

On the other hand, as the number of training data increases, the reliability of the accuracy estimated

from the test data decreases.

3) Since the training and test data are subsets of the entire data set, they are not independent.

To solve the above problems and to increase the reliability of the accuracy of the classification model,

the preliminary method can be repeatedly performed. Each non-replaced sample is called a subsampling,

and the method of repeatedly extracting them is called the random subsampling method. If the accuracy of

the classification model by the \(i^{th}\) subsampling is \( (Accuracy)_i\), and this experiment is repeated

\(r\) times, the overall accuracy of the classification model is defined as the average of each accuracy

as follows;

$$

\text{Overall accuarcy} = \frac{1}{r} \Sigma_{i=1}^r (Accuracy)_i

$$

Since the random subsampling method does not use the entire data set, just like the holdout method,

it still has problems. However, since the accuracy of the model is repeatedly estimated,

the reliability can be increased.

B. Cross Validation Method

The

cross-validation method is a method that attempts to solve the problems of random subsampling.

Like the holdout method, the entire data set is first divided into training data and testing data.

We create a model using the training data and record the number of data correctly classified by the model

using testing data. Then, the roles of testing data and training data are swapped, and the number of

correctly classified data is added up. It is called the

two-fold cross-validation method, and the accuracy

of the model is calculated as the number of data correctly classified in the entire data. The experiment

is repeated \(r\) times in the same way to obtain the average accuracy. In this method, each data is used once

for training and again for testing, which can somewhat solve the problem of random subsampling.

If the two-fold cross-validation method is extended, the \(k\)-fold cross-validation method can be created.

This method divides the entire data set into \(k\) equal-sized subsets, reserves one of the subsets as

testing data, and uses the remaining data as training data to obtain the classification function.

This method is repeated \(k\) times so that each data subset can be used for testing once.

The accuracy of the classification model is the average of the measured accuracies.

In the cross-validation method, a special case where the total number of data is \(k\), that is,

when there is only one testing data, is called the leave-one-out method. This method has the

advantage of maximizing the training data and testing all data without overlapping the test data.

However, since each testing data contains only one data, there is a disadvantage in that the variance

of the estimated accuracy increases, and since the experiment must be repeated as many times as

the number of data, it takes a lot of time.

C. Bootstrap method

The methods described above extract the training data set from the entire data set without replacement,

so there is no identical data in the training and test data. The bootstrap method extracts

the training data with replacement. The data extracted once is not removed from the entire data set,

and the next data is extracted. When the total number of data is \(N\), and the bootstrap method extracts data,

approximately 63.2% of the entire data is extracted as training data. This is because the probability of

each data being extracted as a bootstrap sample is \(1 - (1 - \frac{1}{N})^N\), and this probability

asymptotically converges to \(1 - \frac{1}{e} \)= 0.632 if \(N\) is sufficiently large. Samples not

extracted by the bootstrap method are used as testing data. A classification model is established

using the data set extracted with replacement as training, and this model is applied to the testing data

to investigate the accuracy. The average of the accuracies measured by repeating similar experiments

is used as the model's overall accuracy.

6.2 Decision tree model

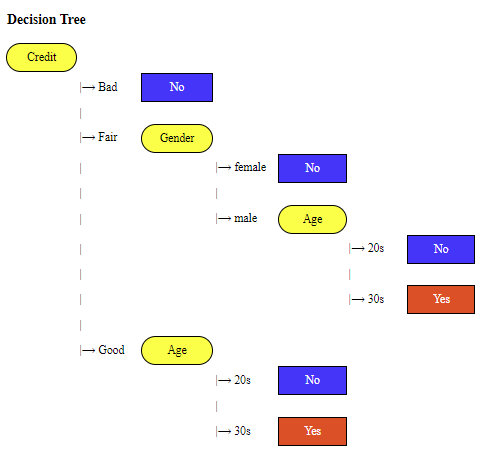

Decision tree is a tree-shaped drawing of a classification function consisting of decision rules,

such as <Figure 6.2.1> which classifies whether a customer visiting a computer store

will purchase a computer. Decision trees are widely used because they are easy to understand

in terms of classification methods and easy to explain results.

<Figure 6.2.1> A decision tree to classify a customer whether he buys or not

In the tree diagram above, the ovals colored yellow represent

nodes that indicate tests for variables, and the top node

is called the

root node. In <Figure 6.2.1>, Credit is the root node, and Gender and Age are nodes

for testing variables. The

branches from the nodes represent the values of the tested variables,

and the

rectangles colored blue or red represent the final classified groups,

which are called

leaves. The root node, Credit, has three branches 'Bad', 'Fair', and 'Good',

and the classified group for 'Bad' credit is indicated by the leaf 'No' which is the Non-purchasing group.

In order to classify the data whose group is unknown, the variable values of the data are examined

along the path from the root node to the leaves. For example, in <Figure 6.2.1>, a person

whose 'Credit' is 'Good' and 'Age' is '30s' is classified as 'Yes', which is a Purchasing group.

When the target variable is a finite number of groups, such as Purchasing group or Non-purchasing group

in the example above, the tree for classification is called a

decision tree. In the case of

a continuous target variable, we can draw a similar decision tree based on a regression model,

which is called a regression tree (Breiman et al.).

The decision tree model was first attempted by Sonquist and Morgan in 1964 and was widely used

by the general public in 1973 because of Morgan and Messenger's algorithm called THAID. In 1980,

Kass introduced an algorithm called CHAID based on the chi-square goodness-of-fit test,

which is still widely used today. In 1982, computer scientist Quinlan introduced a decision tree algorithm

called ID3 and later developed it into an algorithm called C4.5. In 1984, Breiman et al. established

the theory of decision tree growth and pruning through CART. C4.5 and CART are nonparametric classification methods,

but in 1988, Loh and Vanichetaku introduced FACT, a parametric approach.

Recently, rather than classifying data as a single decision tree, an ensemble model that extracts

multiple samples using the bootstrap method and then integrates multiple decision tree classifications

based on these samples is widely used. The ensemble model is studied in Chapter 7.

6.2.1 Decision tree algorithm

The number of cases for making a decision tree is exponentially proportional to the number of variables

and values for each variable, so there are many cases. Some cases may have higher

classification accuracy than others, and some may have higher accuracy but take too much time.

Therefore, many people have studied to find an answer to the question,

‘How can we find an algorithm that is accurate and has reasonable calculation time?’

A rational algorithm partitions a data set by making locally optimal decisions at each node's decision point

when deciding which variable to use. This method is applied sequentially to the partitioned data sets

to complete a decision tree to partition all data sets. In this section, we introduce an algorithm

as an inductive loop.

[

Decision tree algorithm]: Inductive loop

TreeGrowth (\(\small E, F\))

Step 1: \(\;\;\)if stopping_condition(\(\small E, F\)) = true then

Step 2: \(\qquad\)leaf = creatNode().

Step 3: \(\qquad\)leaf.label = Classify(\(\small E\))

Step 4: \(\qquad\)return leaf

Step 5: \(\;\;\)else

Step 6: \(\qquad\)root = creatNode()

Step 7: \(\qquad\)root.test_condition = find_best_split(\(\small E, F\))

Step 8: \(\qquad\)let \(\small V\) = {\(v: v\) is a possible outcome of root.test_condition}

Step 9: \(\qquad\)for each \(\small v \in V\) do

Step 10: \(\qquad \quad\)\(\small E_v =\){ {root.test_condition(\(\small e\)) = } ∩ {\(\small e \in E\)} }

Step 11: \(\qquad \quad\)child = TreeGrowth(\(\small E_v , F\))

Step 12: \(\qquad \quad\)add child as descendent of root and label the edge(root → child) as \(v\)

Step 13: \(\qquad\)end for

Step 14: \(\;\)end if

Step 15: \(\;\)return root

The algorithm's input is training data \(\small E\) and a variable set \(\small F\).

In step 7 of the algorithm, the optimal variable for splitting the data set is selected (find_best_split),

and in steps 11 and 12, the tree is expanded (TreeGrowth). This process is repeated until the stopping

condition of step 1 is satisfied. The entire algorithm process is explained using an example.

6.2.2 Selection of a variable for branching

In classification using decision trees, deciding which variable to select for each node

is crucial for better classification. Various measures have been studied to choose variables

for optimal branching. A common way to select one variable among several variables would be

to choose a variable that makes classification more accurate for each branch when the variable is selected

and branches out. Let's look at the following example.

Example 6.2.1

In a department store, 20 people who visited a particular store were surveyed, and 8 people (40%) were

in the Purchasing group (\(\small G_1\)) and 12 people (60%) were in the Non-purchasing group (\(\small G_2\)).

The Gender and Credit Status of these 20 people were analyzed and a crosstable was created,

as shown in Table 6.2.1 and Table 6.2.2. Let's find out which variable has better branching in a decision tree.

| Table 6.2.1 Crosstable of Gender by Purchase and Non-purchasing group |

| Gender |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

| Male |

4 |

6 |

10 |

| Female |

4 |

6 |

10 |

| Total |

8 |

12 |

20 |

| Table 6.2.2 Crosstable of Credit status by Purchase and Non-purchasing group |

| Credit Status |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

| Good |

7 |

3 |

10 |

| Bad |

1 |

9 |

10 |

| Total |

8 |

12 |

20 |

Answer

In the case of Gender, the ratios of the Purchasing group to the Non-purchasing group for Male and Female are

4 to 6 (40% to 60%), which is the same as the ratio of all 20 people.

In the case of Credit Status, 90% of the customers are in the Non-purchasing group when the Credit Status is Bad,

and 70% are in the Purchasing group when the Credit Status is Good, so there is a significant difference

in the Purchase or Non-purchase ratio between Bad and Good cases. In other words, if the Credit Status

of a customer is Bad, there is a high possibility that he belongs to the Non-purchasing group,

and if it is Good, there is a high possibility that he belongs to the Purchasing group.

So, if the Credit Status is identified, we can distinguish the Purchasing group and the Non-purchasing group can be

somewhat distinguished.

Therefore, if one of the two variables must be selected as a variable for branching

in the decision tree, choosing the Credit Status variable is reasonable for a more accurate classification.

Generally, a variable that has a lot of information for classification is selected.

Many studies have been conducted on how to select a reasonable variable, such as the example above, using

statistical methods. Currently, the most commonly used methods for variable selection in decision trees

include the chi-square independence test, entropy coefficient, Gini coefficient, and classification error rate.

A. Chi-square independence test

The chi-square independence test checks whether the distribution of each group for a variable is independent

or not. In Example 6.2.1, the Gender variable and Purchase status variable can be tested for independence, and

the Credit Status variable and Purchase status variable can be tested for independence.

Suppose there are observed frequencies of a variable \(A\), which are summarized in Table 6.2.3. In that case, the expected frequencies

when the variable \(A\) and the Purchase status variable are independent are calculated in Table 6.2.4.

The expected frequencies are calculated to make the ratios

(\( \frac{O_{\cdot 1}}{O_{\cdot \cdot}} , \frac{O_{\cdot 2}}{O_{\cdot \cdot}}\)) of

the Purchasing group and the Non-purchasing group remain the same in each variable value.

| Table 6.2.3 Observed frequencies of a variable \(A\) by Purchase status group |

Variable \(A\)

value |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

| \(A_1\) |

\(O_{11}\) |

\(O_{12}\) |

\(O_{1 \cdot}\) |

| \(A_1\) |

\(O_{21}\) |

\(O_{22}\) |

\(O_{2 \cdot}\) |

| Total |

\(O_{\cdot 1}\) |

\(O_{\cdot 2}\) |

\(O_{\cdot \cdot}\) |

| Table 6.2.4 Expected frequencies of a variable by Purchase status when they are independent |

Variable \(A\)

value |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

| \(A_1\) |

\(E_{11} = O_{1 \cdot} \times \frac{O_{\cdot 1}}{O_{\cdot \cdot}} \) |

\(E_{12} = O_{1 \cdot} \times \frac{O_{\cdot 2}}{O_{\cdot \cdot}}\) |

\(O_{1 \cdot}\) |

| \(A_1\) |

\(E_{21} = O_{2 \cdot} \times \frac{O_{\cdot 1}}{O_{\cdot \cdot}}\) |

\(E_{22} = O_{2 \cdot} \times \frac{O_{\cdot 2}}{O_{\cdot \cdot}}\) |

\(O_{2 \cdot}\) |

| Total |

\(O_{\cdot 1}\) |

\(O_{\cdot 2}\) |

\(O_{\cdot \cdot}\) |

The chi-square statistic of the observed frequencies in Table 6.2.3 for independence test is the sum of

the squares of the differences between the observed and expected frequencies in each cell divided by

the expected frequency.

$$

\chi^2 = \sum_{i=1}^{2} \sum_{j=1}^{2} \frac{ (O_{ij} - E_{ij})^2}{E_{ij}}

$$

This statistic follows the chi-square distribution with a degree of freedom of 1.

Suppose the distribution

of each group in each variable value is the same as the distribution of the entire group. In that case,

the chi-square statistic becomes 0, concluding that the variables and groups are independent.

Suppose the distribution of each group in each variable value is very different from the distribution of

the entire group. In that case, the chi-square statistic becomes very large, and the null hypothesis that the variables

and groups are independent is rejected. The stronger the degree of rejection, the better the variable is

for branching.

Example 6.2.2

Let's examine which variable is better for branching by using the chi-square independence test

for the Gender and Credit Status variable in Example 6.2.1.

Answer

In the crosstable of the Gender and Purchase status, the distribution of

(purchasing group, non-purchasing group) in the entire data is (40%, 60%). The distributions in each Male

and female are also the same at (40%, 60%), so the expected frequencies of Male and Female are (4, 6)

which are the same as observed frequencies and the chi-square statistic \(\chi_{Gender}^2\)is 0 as follows.

$$ \small

\chi_{Credit}^2 = \frac{ (4 - 4)^2}{4} + \frac{ (6 - 6)^2}{6} +\frac{ (4 - 4)^2}{4} +\frac{ (6 - 6)^2}{6} = 0

$$

Therefore, the Gender variable and Purchase status are independent.

In the crosstable of the Credit and Purchase status, the expected frequencies for each Credit status

is (4, 6), so the chi-square statistic is as follows.

$$ \small

\chi_{Credit}^2 = \frac{ (7 - 4)^2}{4} + \frac{ (3 - 6)^2}{6} +\frac{ (1 - 4)^2}{4} +\frac{ (9 - 6)^2}{6} = 7.5

$$

Therefore, since it is greater than the critical value of \(\small \chi_{1;\; 0.05}^2 \) = 3.841 at the significance level of 5%

in the chi-square distribution with the degree of freedom of 1, the Credit variable and Purchase status

are not independent. In other words, if the Credit status is known, it contains a lot of information

to decide the Purchasing group and the Non-purchasing group. Therefore, the branching is selected

by selecting the Credit variable rather than the Gender variable.

If a variable \(A\) has \(a\) number of values and a group variable has \(k\) number of groups,

the chi-square statistic of the \(a \times k\) crosstable is as follows;

$$

\chi^2 = \sum_{i=1}^{a} \sum_{j=1}^{k} \frac{ (O_{ij} - E_{ij})^2}{E_{ij}} \;\;\text{where}\;\; E_{ij} = O_{i \cdot} \times \frac{O_{\cdot j}}{O_{\cdot \cdot}}

$$

This test statistic follows the chi-square distribution with \((a-1)(k-1)\) degree of freedom.

Since the number of values of each variable can be different, the variable with the smaller \(p\)-value

of the chi-square test is used when selecting a variable to split in a decision tree.

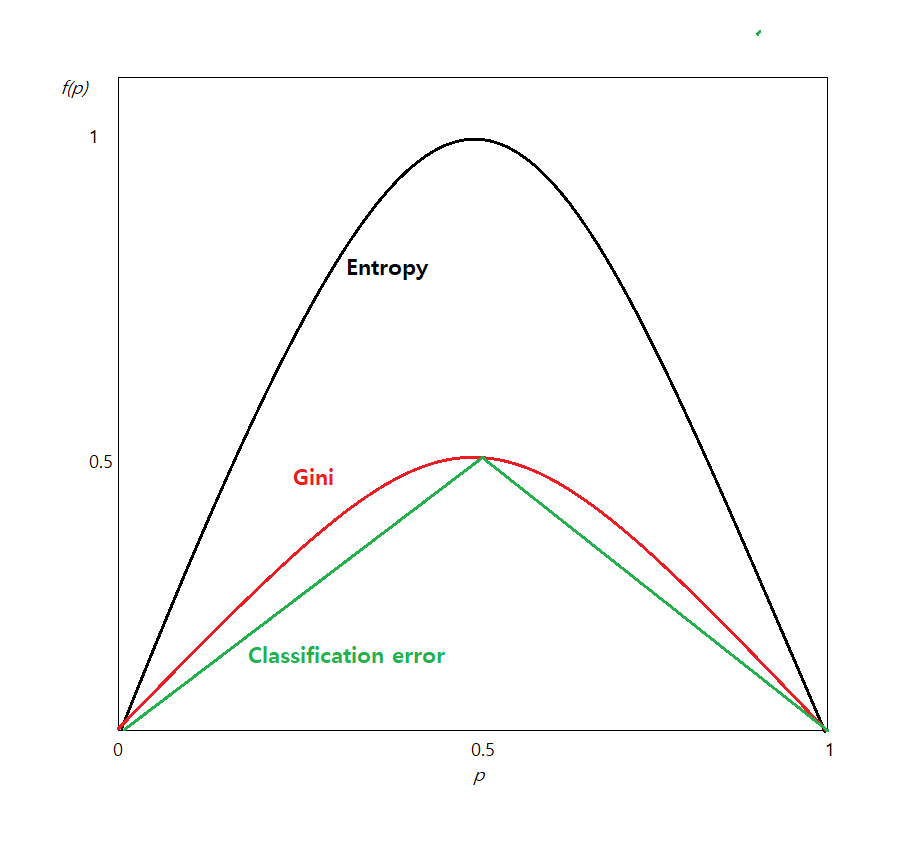

B. Entropy coefficient, Gini coefficient, and classification error rate

The entropy coefficient, Gini coefficient, and classification error rate are similar concepts that measure

the uncertainty or purity of a distribution function. If there are \(k\) number of groups,

\(G_1 , G_2 , ... , G_k\), and \(p_1 , p_2 , ... , p_k\) are the probability distribution that

the data belongs to each group, each measure is defined as follows;

$$

\begin{align}

\text{Entropy coefficient} &= - \sum_{i=1}^{k} p_i \times log_{2} p_i \;\; (\text{define}\;\; 0 \times log_{2} 0 = 0 ) \\

\text{Gini coefficient} &= 1 - \sum_{i=1}^{k} p_{i}^2 \\

\text{Classification error rate} &= 1 - max\{p_1 , p_2 , ..., p_k \}

\end{align}

$$

To understand these three measures, let's look at the case where there are only two groups, that is \(k\) = 2.

If the probability of group 1 is \(p\), then the probability of group 2 is \(1-p\). In this case,

the three measures become as follows;

$$

\begin{align}

\text{Entropy coefficient} &= - p \times log_{2} p - (1-p) \times log_{2} (1-p) \\

\text{Gini coefficient} &= 1 - p^2 - (1-p)^2 \\

\text{Classification error rate} &= 1 - max\{p , 1-p \}

\end{align}

$$

<Figure 6.2.2> shows graphs of three measures according to the value of \(p\).

<Figure 6.2.2> Entropy, Gini coefficient, and classification error when there are two groups

As we can see in the figure, all three measures have a maximum value when \(p\) = 0.5 (in this case,

\(1-p\) = 0.5 also, and it is a uniform distribution) and a minimum value of \(p\) = 0 when or \(p\) = 1.

That is, when the probability of two groups is the same (\(p\) = 0.5), uncertainty has a maximum value

because we do not know which group to classify into.

On the other hand, if the probability of one group is 1, there is no uncertainty, that is, the certainty

of classification is 100%, so each measure has a minimum value of 0. Therefore, branching selects a variable

with less uncertainty.

Example 6.2.3

Find the entropy coefficient, Gini coefficient, and classification error rate for the distribution

of the Purchasing group and the Non-purchasing group (40%, 60%) in the entire data. Also, find the

entropy coefficient, Gini coefficient, and classification error rate for each Gender and Credit Status,

and examine which variable is good for branching.

Answer

The entropy coefficient, Gini coefficient, and classification error rate for the probability distribution

(0.4, 0.6) of the Purchasing group and the Non-purchasing group are as in Table 6.2.5, and the measures

for the Gender are in Table 6.2.6, and the measures for the Credit Status are in Table 6.2.7.

| Table 6.2.5 Uncetainty measures for the distribution of (Purchase, Non-purchase) of entire data |

|

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

Uncetainty measures |

Entire data |

8 |

12 |

20 |

$$ \small

\begin{align}

\text{Entropy coefficient} &= - 0.4 \times log_{2} 0.4 - (1-0.4) \times log_{2} (1-0.4) = 0.9710 \\

\text{Gini coefficient} &= 1 - {0.4}^2 - (1-0.4)^2 = 0.4800\\

\text{Classification error rate} &= 1 - max\{0.4 , 1-0.4 \} = 0.4000

\end{align}

$$

|

| Table 6.2.6 Uncetainty measures for the distribution of (Purchase, Non-purchase) of Gender |

| Gender |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

Uncetainty measures |

Male |

4 |

6 |

10 |

$$ \small

\begin{align}

\text{Entropy coefficient} &= - 0.4 \times log_{2} 0.4 - (1-0.4) \times log_{2} (1-0.4) = 0.9710 \\

\text{Gini coefficient} &= 1 - {0.4}^2 - (1-0.4)^2 = 0.4800\\

\text{Classification error rate} &= 1 - max\{0.4 , 1-0.4 \} = 0.4000

\end{align}

$$

|

Female |

4 |

6 |

10 |

$$ \small

\begin{align}

\text{Entropy coefficient} &= - 0.4 \times log_{2} 0.4 - (1-0.4) \times log_{2} (1-0.4) = 0.9710 \\

\text{Gini coefficient} &= 1 - {0.4}^2 - (1-0.4)^2 = 0.4800\\

\text{Classification error rate} &= 1 - max\{0.4 , 1-0.4 \} = 0.4000

\end{align}

$$

|

| Table 6.2.7 Uncetainty measures for the distribution of (Purchase, Non-purchase) of Credit Status data |

| Credit Status |

Purchasing group

\(G_1\) |

Non-purchasing group

\(G_2\) |

Total |

Uncetainty measures |

Good |

7 |

3 |

10 |

$$

\begin{align}

\text{Entropy coefficient} &= - 0.7 \times log_{2} 0.7 - (1-0.7) \times log_{2} (1-0.7) = 0.8813 \\

\text{Gini coefficient} &= 1 - {0.7}^2 - (1-0.7)^2 = 0.4200\\

\text{Classification error rate} &= 1 - max\{0.7 , 1-0.7 \} = 0.3000

\end{align}

$$

|

Bad |

1 |

9 |

10 |

$$

\begin{align}

\text{Entropy coefficient} &= - 0.1 \times log_{2} 0.1 - (1-0.1) \times log_{2} (1-0.1) = 0.4690 \\

\text{Gini coefficient} &= 1 - {0.1}^2 - (1-0.1)^2 = 0.1800\\

\text{Classification error rate} &= 1 - max\{0.1 , 1-0.1 \} = 0.1000

\end{align}

$$

|

When looking at the uncertainty for the two variables, each attribute of Credit Status is relatively less than

the Gender attribute, so branching using Credit Status is reasonable.

Suppose there are \(k\) groups as \(G_1 , G_2 , ... , G_k \) and there are \(a\) number of attributes in

variable \(A\) as \(A_1 , A_2 , ... , A_a \). Let \(O_{ij}\) be the observed frequency of the

attribute \(A_i \) and the group \(G_j\), \(O_{i \cdot}\) be the sum of the observed frequencies for

the attribute \(A_i\), \(O_{\cdot j}\) be the sum of the observed frequencies for the group \(G_j\),

\(O_{\cdot \cdot}\) be the total number of data, and \(I(A_{i})\) be the uncertainty of the attribute \(A_i\)

as summarized in Table 6.2.8.

| Table 6.2.8 \(a \times k\) frequency table and uncetainty measure of the variable \(A\) |

| Variable \(A\) |

Group \(G_1\) |

Group \(G_2\) |

\(\cdots\) |

Group \(G_k\) |

Total |

Uncetainty |

| \(A_1\) |

\(O_{11}\) |

\(O_{12}\) |

\(\cdots\) |

\(O_{1k}\) |

\(O_{1 \cdot} \) |

\(I(A_1)\) |

| \(A_2\) |

\(O_{21}\) |

\(O_{22}\) |

\(\cdots\) |

\(O_{2k}\) |

\(O_{2 \cdot }\) |

\(I(A_2)\) |

| \(\cdots\) |

\(\cdots\) |

\(\cdots\) |

\(\cdots\) |

\(\cdots\) |

\(\cdots\) |

\(\cdots\) |

| \(A_a\) |

\(O_{a1}\) |

\(O_{a2}\) |

\(\cdots\) |

\(O_{ak}\) |

\(O_{a \cdot} \) |

\(I(A_a)\) |

| Total

| \(O_{\cdot 1}\)

| \(O_{\cdot 2}\)

| \(\cdots\)

| \(O_{\cdot k}\)

| \(O_{\cdot \cdot }\)

| Uncertainty of \(A\)

\(I(A\))

|

The uncertainty of the variable \(A\) is the expected value of each attribute \(A_{i}\) by weighting

the proportion of the observed frequency, \(\frac{O_{i \cdot}}{O_{\cdot \cdot}}\), as follows;

$$

I(A) = \frac{O_{1 \cdot}}{O_{\cdot \cdot}} \times I(A_{1}) + \frac{O_{2 \cdot}}{O_{\cdot \cdot}} \times I(A_{2}) + \cdots + \frac{O_{a \cdot}}{O_{\cdot \cdot}} \times I(A_{a})

$$

If we do not know the information of the variable \(A\), the uncertainty of this node \(T\), \(I(T)\), is

the uncertainty about the distribution of each group proportion. In the case of the entropy coefficient,

it is as follows;

$$

I(T) = - \sum_{j=1}^{k} \left( \frac{O_{\cdot j}}{O_{\cdot \cdot}} \right) \;\; log_{2} \left( \frac{O_{\cdot j}}{O_{\cdot \cdot}} \right)

$$

In the decision tree, a variable for branching is selected if it has a large difference between

the uncertainty of the current node, \(I(T)\), and the expected uncertainty of a variable \(A\), \(I(A)\).

This difference is called an

information gain and is expressed as \(\Delta\). The information gain

at the current node \(T\) by branching into the variable \(A\) is as follows;

$$

\Delta = I(T) - I(A)

$$

The greater information gain of one variable implies that by branching into this variable, more uncertainty

is removed, and, therefore, more accurate classification is expected. The information gain obtained using

the entropy coefficient or Gini coefficient tends to prefer a variable with many variable values.

In order to overcome this problem, the

information gain ratio, which is the information gain

divided by the uncertainty of the current node \(T\) is often used as the basis for branching.

$$

\text{Information gain ratio} = \frac{\Delta}{I(T)}

$$

Example 6.2.4

In Example 6.2.3, find the information gain for each measure of the Gender and Credit Status variables.

Answer

Using the uncertainty values for each measure calculated in Example 6.2.3, the information gain

for each measure of the Gender variable is as follows;

$$ \small

\begin{align}

\text{Information gain by entropy} &= 0.9710 - \left( \frac{10}{20} \times 0.9710 + \frac{10}{20} \times 0.9710 \right) = 0.0000 \\

\text{Information gain by Gini} &= 0.4800 - \left( \frac{10}{20} \times 0.4800 + \frac{10}{20} \times 0.4800 \right) = 0.0000 \\

\text{Information gain by misclassification error} &= 0.4000 - \left( \frac{10}{20} \times 0.4000 + \frac{10}{20} \times 0.4000 \right) = 0.0000 \\

\end{align}

$$

That is, since the Gender variable has the same uncertainty as the current node, there is no information gain

for classification that can be obtained by branching. The information gain for the Credit Status

variable is as follows;

$$ \small

\begin{align}

\text{Information gain by entropy} &= 0.9710 - \left( \frac{10}{20} \times 0.8813 + \frac{10}{20} \times 0.4690 \right) = 0.2958 \\

\text{Information gain by Gini} &= 0.4800 - \left( \frac{10}{20} \times 0.4200 + \frac{10}{20} \times 0.1800 \right) = 0.1800 \\

\text{Information gain by misclassification error} &= 0.4000 - \left( \frac{10}{20} \times 0.3000 + \frac{10}{20} \times 0.1000 \right) = 0.2000 \\

\end{align}

$$

Therefore, regardless of which measure is used, the Credit Status variable has more information gain than Gender,

so it can be said that the Credit Status variable is better for branching at the current node.

There are many comparative studies on the question, ‘Which of the three uncertainty measures is better?’

The conclusion is that since all three measures measure uncertainty similarly, it is not possible to say

‘which measure is better.’

Let's take a closer look at the algorithm for creating a decision tree using the following example.

Example 6.2.5

When we surveyed 20 customers who visited a computer store, 8 customers purchased a computer (Purchasing group, \(\small G_1\)) and

12 customers did not purchase a computer (Non-purchasing group, \(\small G_2 \). The survey included variables such as gender, age,

monthly income, and credit status of these 20 customers as well as Purchase status as shown in Table 6.2.9.

Note that all variables are surveyed as categorical variables such as (Female, Male) for gender, (20s, 30s) for age,

(GE2000, LT2000) for income, (Bad, Fair, Good) for credit status, and (No, Yes) for Purchase status.

1) Find a classification model using the decision tree. Use the entropy coefficient for variable selection, and if the number of data in each leaf is

5 or less, no further branching is performed, and a decision is made by majority vote. If the data in each leaf are classified

into one group, no further branching is performed.

2) Using this decision tree model, classify a customer who is a 33-year-old male with a monthly income of 2,200 (unit 10,000 won)

and good credit status, whether he will purchase a computer or not.

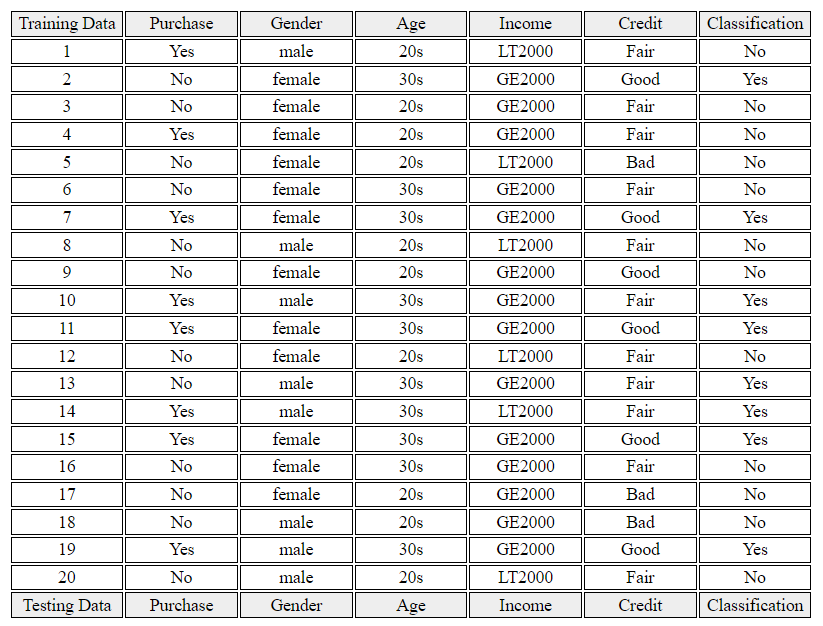

| Table 6.2.9 Survey of customers on gender, age, income, credit status and purchase status |

| Number |

Gender |

Age |

Income

(unit 10,000 won) |

Credit |

Purchase |

| 1 | Male | 20s | LT2000 | Fair | Yes |

| 2 | Female | 30s | GE2000 | Good | No |

| 3 | Female | 20s | GE2000 | Fair | No |

| 4 | Female | 20s | GE2000 | Fair | Yes |

| 5 | Female | 20s | LT2000 | Bad | No |

| 6 | Female | 30s | GE2000 | Fair | No |

| 7 | Female | 30s | GE2000 | Good | Yes |

| 8 | Male | 20s | LT2000 | Fair | No |

| 9 | Female | 20s | GE2000 | Good | No |

| 10 | Male | 30s | GE2000 | Fair | Yes |

| 11 | Female | 30s | GE2000 | Good | Yes |

| 12 | Female | 20s | LT2000 | Fair | No |

| 13 | Male | 30s | GE2000 | Fair | No |

| 14 | Male | 30s | LT2000 | Fair | Yes |

| 15 | Female | 30s | GE2000 | Good | Yes |

| 16 | Female | 30s | GE2000 | Fair | No |

| 17 | Female | 20s | GE2000 | Bad | No |

| 18 | Male | 20s | GE2000 | Bad | No |

| 19 | Male | 30s | GE2000 | Good | Yes |

| 20 | Male | 20s | LT2000 | Fair | No |

Answer

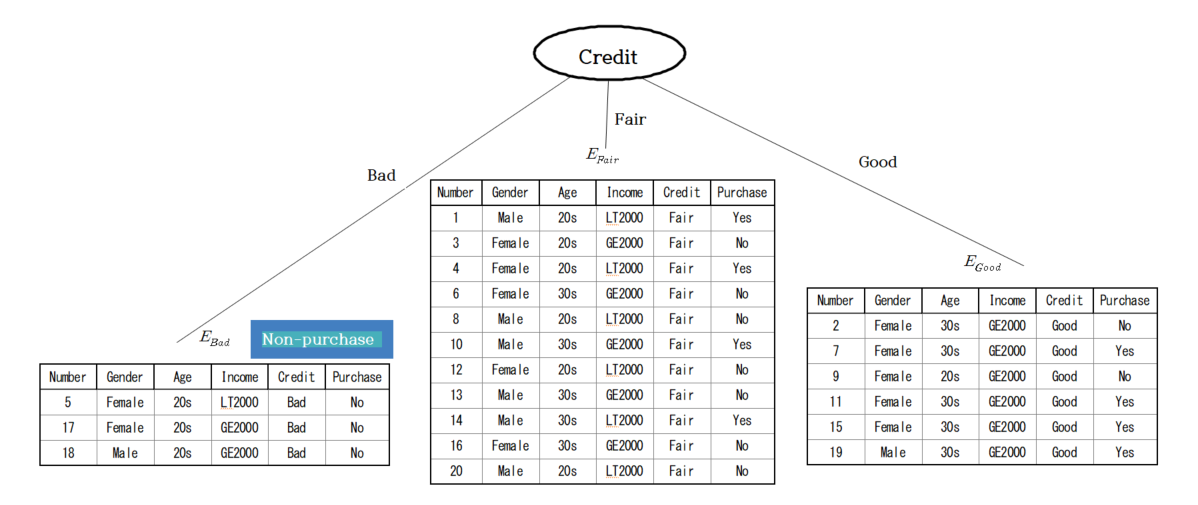

In the decision tree algorithm, the data set \(\small E\) is the data in Table 6.2.9, and the variable set is

\(\small F\) = {Gender, Age, Income, Credit}. The target variable, Purchase, has two groups, {Yes, No}.

The stopping rule of the decision tree is ‘If the number of data in each leaf is 5 or less, do not divide any more’,

and ‘If all are classified into one group, stop with the leaf as the group’.

The number of data in the current data set is 20, so stopping.conditon(\(\small E, F\)) in step 1 is false,

so go to step 6. For the root node \(\small T\)'s creatNode(), the entropy coefficient \(\small I(T) \) for

the distribution of the purchasing group(\(\small G_1\)) and the non-purchasing group (\(\small G_2\)), (8/20, 12/20), is as follows;

$$ \small

I(T) = - 0.4 \times log_{2} 0.4 - 0.6 \times log_{2} 0.6 = 0.9710

$$

In order to find the optimal branch split, find_best_split(), of step 7, a cross-table is obtained for each variable

by group, and the expected information and information gain for the variable are obtained as in Table 6.2.10

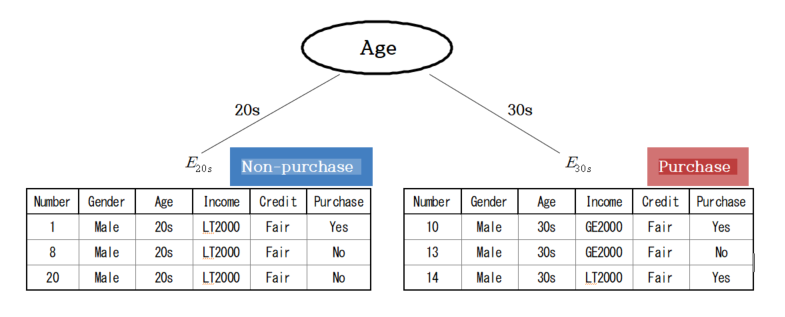

using the entropy coefficient. Since the information gain of the credit status is the largest, the root node

becomes the credit status, and the set of variable values of credit status in step 8 becomes

\(\small V\) = {Bad, Fair, Good}. The \(\small E_{Bad}, E_{Fair}, E_{Good}\) according to the credit status in step 10

are drawn in the form of a decision tree as in <Figure 6.2.3>.

| Table 6.2.10 Expected information and information gain for each variable |

| Variable |

Purchasing group \(G_1\) |

Non-purchasing group \(G_2\) |

Total |

Entropy |

Information gain

\(\Delta\) |

| Gender |

Female |

4 |

8 |

12 |

0.9183 |

| Male |

4 |

4 |

8 |

1.0000 |

| Expected entropy |

0.9510 |

0.0200 |

| Age |

20s |

2 |

8 |

10 |

0.7219 |

| 30s |

6 |

4 |

10 |

0.9710 |

| Expected entropy |

0.8464 |

0.1246 |

| Income |

GE200 |

6 |

8 |

14 |

0.9852 |

| LT200 |

2 |

4 |

6 |

0.9783 |

| Expected entropy |

0.9651 |

0.0059 |

| Credit |

Bad |

0 |

3 |

3 |

0.0000 |

| Fair |

4 |

7 |

11 |

0.9457 |

| Good |

4 |

2 |

6 |

0.9183 |

| Expected entropy |

0.9756 |

0.1754 |

<Figure 6.2.3> Decision tree with branching according to credit status

The TreeGrowth() algorithm is repeatedly applied to each data set until the stopping rule is satisfied (step 11).

Among these, the data sets of 3 people with Bad credit, \(\small E_{Bad} \), are all Non-purchasing groups, satisfying the stopping rule,

so they are not branching any further, and the leaves are marked as the Non-purchasing group.

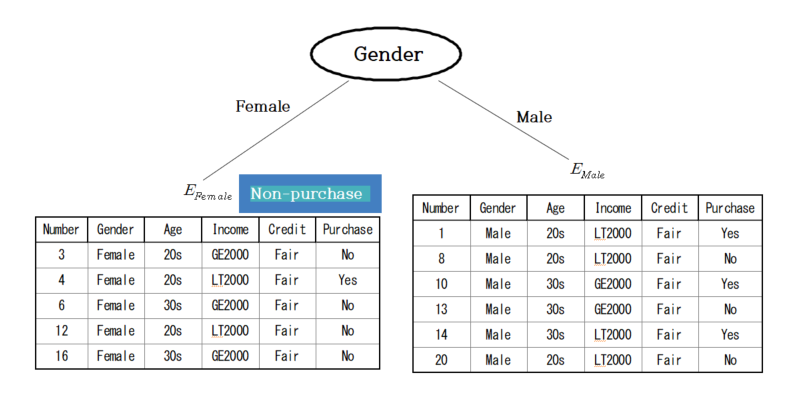

Since the stopping rule is not satisfied for the data set of 11 people with Fair credit, \(\small E_{Fair} \),

this data set needs further split.

The entropy coefficients for the distribution (4/11, 7/11) of the Purchasing group (\(\small G_1 \)) and

the Non-purchasing group (\(\small G_2 \)) are as follows.

$$ \small

I(E_{Fair}) = - \frac{4}{11} \times log_{2} \frac{4}{11} - \frac{7}{11} \times log_{2} \frac{7}{11} = 0.9457

$$

In order to find the optimal split, find_best_split(), for the 11 people, a cross-table for each variable by the group

is obtained, and the expected information and information gain for the variables are obtained using the entropy coefficient,

as shown in Table 6.2.11. In the case of the data set with Fair credit, the information gain for Gender is the largest,

so it becomes a node for branching, and a decision tree such as <Figure 6.2.4> is formed.

| Table 6.2.11 Expected information and information gain for each variable in \(\small E_{Fair} \) |

| Variable |

Purchasing group \(G_1\) |

Non-purchasing group \(G_2\) |

Total |

Entropy |

Information gain

\(\Delta\) |

| Gender |

Female |

1 |

4 |

5 |

0.7219 |

| Male |

3 |

3 |

6 |

1.0000 |

| Expected entropy |

0.8736 |

0.0721 |

| Age |

20s |

2 |

4 |

6 |

0.9183 |

| 30s |

2 |

3 |

5 |

0.9710 |

| Expected entropy |

0.9422 |

0.0034 |

| Income |

GE200 |

2 |

4 |

6 |

0.9183 |

| LT200 |

2 |

3 |

5 |

0.9710 |

| Expected entropy |

0.9422 |

0.0034 |

<Figure 6.2.4> Decision tree with branching according to Gender in \(\small E_{Fair} \)

As shown in the Figure 6.2.4, there are 5 data sets of Female with Fair credit, \(\small E_{Female} \), which satisfies

the stopping rule, so they are not split any further. Since there four people who did not purchase the computer and

only one person purchased, this node are marked as Non-purchasing group by majority vote.

As shown in Figure 6.2.4, there are 6 data sets of Male with Fair credit, \(\small E_{Male} \),

the stopping rule is not satisfied and this data set needs further split.

The entropy coefficients for the distribution (3/6, 3/6) of the Purchasing group (\(\small G_1 \)) and

the Non-purchasing group (\(\small G_2 \)) are as follows.

$$ \small

I(E_{Male}) = - \frac{3}{6} \times log_{2} \frac{3}{6} - \frac{3}{6} \times log_{2} \frac{3}{6} = 1

$$

In order to find the optimal branch split, find_best_split(), for the 6 people, a cross-table by the group for each variable

is obtained, and the expected information and information gain for the variables are obtained using the entropy coefficient,

as shown in Table 6.2.12. In the case of the Male with Fair credit, the information gain for Age is the largest,

so it becomes a node for branching, and a decision tree such as <Figure 6.2.5> is formed.

Here, since there are 3 people in their 20s and 30s, there is no more branching, and the 20s becomes the Non-purchasing group,

and the 30s becomes the Purchasing group by majority vote.

| Table 6.2.12 Expected information and information gain for each variable in \(\small E_{Male} \) |

| Variable |

Purchasing group \(G_1\) |

Non-purchasing group \(G_2\) |

Total |

Entropy |

Information gain

\(\Delta\) |

| Age |

20s |

1 |

2 |

3 |

0.9183 |

| 30s |

2 |

1 |

3 |

0.9183 |

| Expected entropy |

0.9183 |

0.0817 |

| Income |

GE200 |

1 |

1 |

2 |

1.0000 |

| LT200 |

2 |

2 |

4 |

1.0000 |

| Expected entropy |

1.0000 |

0.0000 |

<Figure 6.2.5> Decision tree with branching according to Gender in \(\small E_{Male} \)

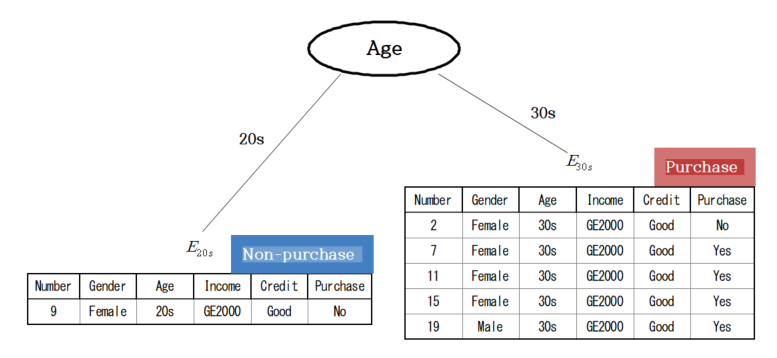

At the root node with Credit, since the stopping rule is not satisfied for the data set of 6 people with Good credit, \(\small E_{Good} \),

the entropy coefficients for the distribution (4/6, 2/6) of the Purchasing group (\(\small G_1 \)) and

the Non-purchasing group (\(\small G_2 \)) are as follows.

$$ \small

I(E_{Good}) = - \frac{4}{6} \times log_{2} \frac{4}{6} - \frac{2}{6} \times log_{2} \frac{2}{6} = 0.9183

$$

In order to find the optimal branch split, find_best_split(), for the 6 people, a cross-table by the group for each variable

is obtained, and the expected information and information gain for the variables are obtained using the entropy coefficient

as shown in Table 6.2.13. Since the information gain of Age is the largest in the data set of Good credit,

it becomes a node for branching and forms a decision tree as in <Figure 6.2.6>. As shown in the figure,

among the people with Good credit, there is only one person in Age 20s who did not purchase a computer,

so it becomes the Non-purchasing group by the stopping rule. There are 5 people in Age 30s, and 4 of them

purchased a computer, so they become the Purchasing group by majority vote.

| Table 6.2.13 Expected information and information gain for each variable in \(\small E_{Good} \) |

| Variable |

Purchasing group \(G_1\) |

Non-purchasing group \(G_2\) |

Total |

Entropy |

Information gain

\(\Delta\) |

| Gender |

Female |

3 |

2 |

5 |

0.9710 |

| Male |

1 |

0 |

1 |

0.0000 |

| Expected entropy |

0.8091 |

0.1092 |

| Age |

20s |

0 |

1 |

1 |

0.0000 |

| 30s |

4 |

1 |

5 |

0.7219 |

| Expected entropy |

0.6016 |

0.3167 |

| Income |

GE200 |

4 |

2 |

6 |

0.9183 |

| LT200 |

0 |

0 |

0 |

0.0000 |

| Expected entropy |

0.9183 |

0.0000 |

<Figure 6.2.6> Decision tree with branching according to Age in \(\small E_{Good} \)

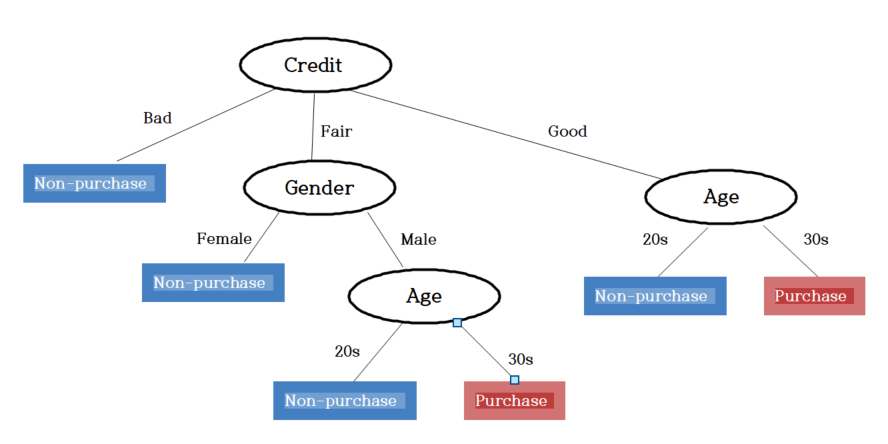

If we combine the above, the decision tree in Figure 6.2.7 is completed. Therefore, the customer

who is a 33-year-old man, has a monthly income of 220, and has a good credit is classified as a Purchasing group.

<Figure 6.2.7> Decision tree to decide a customer will purchase a computer or not

In 『eStatU』 menu, select [Decision Tree] to see the window as follows;

Check the criteria for variable selection which is 'Entropy' in this example, enter the maximum tree depth 5 and

the minimum number of data 5 for a decision. You can divide the original data set into 'Train' and 'Test'

by assigning the percents. Click [Execute] button to see the bar graph matrix and decision tree.

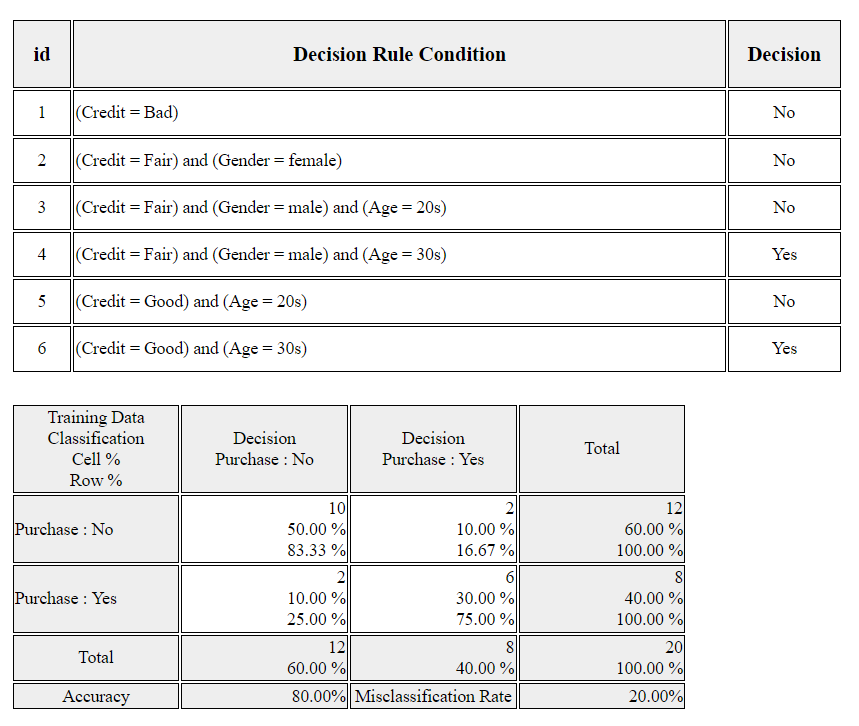

Click [Classification Stat] to see the decision rules of this decision tree and the accuracy/misclassification of

the classification as in <Figure 6.2.8>.

Click [Classification Table] to see the original data and classification result as in <Figure 6.2.9>.

[Decision Tree]

<Figure 6.2.8> Decision rules and classifcation acuracy

<Figure 6.2.9> Original data and classification

6.2.3 Categorization of a continuous variable

We can convert a continuous variable to a categorical variable, and a decision tree model can be applied.

For example, the monthly income variable can be divided into two groups: ‘Greater than or equal 2000’ and

‘Less than 2000’. In this case, the question arises ‘What boundary value should be used to divide

a value of the continuous variable?’ An expert related to this research can decide this boundary value.

However, if the determination of the boundary value is for more accurate classification, then

the uncertainty measures studied in the previous section can be used to determine the boundary value

which increases the accuracy of the classification.

Example 6.2.6

In a store, a survey of 10 customers was conducted on their monthly income (unit 10,000 won) and whether they purchased

a certain product or not, and the results are shown in Table 6.2.14. The incomes are arranged in ascending order

and the purchase status is denoted as 'Y' if a customer purchases, and 'N' if he did not purchase.

In order to apply the decision tree model, we want to divide the monthly income into two categories.

What boundary value of the income is reasonable to divide for classification?

| Table 6.2.14 Survey of customers on income and purchase status |

| Purchase | N | N | N | Y | Y | Y | N | N | N | N |

| Income | 100 | 120 | 160 | 180 | 186 | 190 | 210 | 250 | 270 | 300 |

Answer

It is reasonable to examine all middle values of two adjacent incomes as the boundary value,

and check how their classification result is made. Then select the boundary value with the least ‘uncertainty’ among them.

When a boundary value is examined, if incomes on left side of the boundary value are classified as 'N' group and incomes

on the right-side of the boundary value are classified as 'Y' group, a crosstable for classification is summarized

as in Table 6.2.15. A boundary value which is smaller than the minimum income or larger than the maximum income

is excluded because its division is meaningless. For the first middle value 110 between income 100 and 120 in Table 6.2.11,

we classify data using the rule as follows;

$$ \small

\text{If the income ≤ 110, then classify data as 'N' group, else classify data as 'Y' group}

$$

The data 100 is classified correctly using this rule as 'N' group, and the remaining nine data are classified 'Y' group,

therefore, three (180, 186, 190) out of nine data are classified correctly as 'Y' group, and six (120, 160, 210, 250, 270, 300)

out of nine data are classified incorrectly as 'Y' group as the following crosstable;

Using the Gini coefficient as the uncertainty measure, the expected Gini coefficient when the middle value

is 110 calculated as follows;

$$ \small

\frac{1}{10} \times \left\{ 1 - ( \frac{1}{1} )^2 - ( \frac{0}{1} )^2 \right\} \;+\; \frac{9}{10} \times \left\{ 1 - ( \frac{6}{9} )^2 - ( \frac{3}{9} )^2 \right\} = 0.4000

$$

The expected Gini coefficients for all remaining middle values can be calculated in the same way as Table 6.2.15.

The boundary value with the least uncertainty is 200.

| Table 6.2.15 Expected Gini coefficient using the middle value of two adjacent incomes |

|

|

Actual group |

|

| Middle value = 110 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

1 |

0 |

1 |

| \(Y\) |

6 |

3 |

9 |

|

Total |

|

|

10 |

0.400 |

|

|

Actual group |

|

| Middle value = 135 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

2 |

0 |

2 |

| \(Y\) |

5 |

3 |

8 |

|

Total |

|

|

10 |

0.375 |

|

|

Actual group |

|

| Middle value = 170 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

3 |

0 |

3 |

| \(Y\) |

4 |

3 |

7 |

|

Total |

|

|

10 |

0.343 |

|

|

Actual group |

|

| Middle value = 183 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

3 |

1 |

4 |

| \(Y\) |

4 |

2 |

6 |

|

Total |

|

|

10 |

0.417 |

|

|

Actual group |

|

| Middle value = 188 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

3 |

2 |

5 |

| \(Y\) |

4 |

1 |

5 |

|

Total |

|

|

10 |

0.400 |

|

|

Actual group |

|

| Middle value = 200 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

3 |

3 |

6 |

| \(Y\) |

4 |

0 |

4 |

|

Total |

|

|

10 |

0.300 |

|

|

Actual group |

|

| Middle value = 230 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

4 |

3 |

7 |

| \(Y\) |

3 |

0 |

3 |

|

Total |

|

|

10 |

0.343 |

|

|

Actual group |

|

| Middle value = 260 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

5 |

3 |

8 |

| \(Y\) |

2 |

0 |

2 |

|

Total |

|

|

10 |

0.375 |

|

|

Actual group |

|

| Middle value = 285 |

|

\(N\) |

\(Y\) |

Total |

Expected Gini coefficient |

| Classified group |

\(N\) |

6 |

3 |

9 |

| \(Y\) |

1 |

0 |

1 |

|

Total |

|

|

10 |

0.400 |

The method of setting the boundary value of the continuous variable, as the above example, requires many calculations.

If there are several candidates for the threshold, we can decide which of them is better in a similar way.

Example 6.2.7

In a department store, when 20 customers were surveyed, 7 (35%) made purchases and 13 (65%) did not make purchases.

A cross-tabulation was created to compare the methods of dividing the ages of these 20 people into those

under 25 and over 25, and those under 35 and over 35, as shown in Table 6.2.16. Using the entropy information gain,

decide which interval is better.

| Table 6.2.16 crosstable of two interval divisions by purchase status |

|

Purchase status |

|

| Age interval 1 |

Purchasing group |

Non-purchasing group |

Total |

| < 25 |

1 |

5 |

6 |

| \(\ge\) 25 |

6 |

8 |

14 |

| Total |

7 |

13 |

20 |

| Age interval 2 |

Purchasing group |

Non-purchasing group |

Total |

| < 35 |

3 |

12 |

15 |

| \(\ge\) 35 |

4 |

1 |

5 |

| Total |

7 |

13 |

20 |

Answer

Let us compare the two crosstables to see which interval division is better.

(Age interval 1) has many Non-purchasing groups in both '< 25' and '\(\ge 25\) intervals.

(Age unterval 2) has 12 customers in Non-purchasing group out of 15 customers who are '< 35' which is a high proportion,

and 4 customers in Purchasing group out of 5 customers who are '\(\ge 35\) which is also a high proportion.

Therefore, among the two interval division methods, (Age interval 2) provides more information on purchase.

Let us confirm this using the entropy measure.

The expected entropy for the total distribution (\( \frac{7}{20} , \frac{13}{20}\)) of Purchasing group and

Non-purchasing group is calculated as follows.

$$ \small

- (\frac{7}{20}) \; log_{2} ( \frac{7}{20} ) \; - \;(\frac{13}{20} ) \; log_{2} (\frac{13}{20} ) \;=\; 0.9341

$$

The expected entropy and information gain for the two interval divisions are calculated as in Table 6.2.17.

| Table 6.2.17 Expected entropy and information gain of two interval divisions |

|

Purchase status |

|

| Age interval 1 |

Purchasing group |

Non-purchasing group |

Total |

Entropy |

|

| < 25 |

1 |

5 |

6 |

\(\small - (\frac{1}{6}) log_{2} ( \frac{1}{6} )^2 - (\frac{5}{6} ) log_{2} (\frac{5}{6} ) = 0.6500\) |

| \(\ge\) 25 |

6 |

8 |

14 |

\(\small - (\frac{6}{14}) log_{2} ( \frac{6}{14} )^2 - (\frac{8}{14} ) log_{2} (\frac{8}{14} ) = 0.9852\) |

| Total |

7 |

13 |

20 |

Expected entropy

= \(\small \frac{6}{20} \times 0.6500 + \frac{14}{20} \times 0.9852\)

= 0.8847 |

Information gain

= \(\small 0.9341 - 0.8847\)

= 0.0494 |

| Age interval 2 |

Purchasing group |

Non-purchasing group |

Total |

Entropy |

|

| < 35 |

3 |

12 |

15 |

\(\small - (\frac{3}{15}) log_{2} ( \frac{3}{15} )^2 - (\frac{12}{15} ) log_{2} (\frac{12}{15} ) = 0.7219\) |

| \(\ge\) 35 |

4 |

1 |

5 |

\(\small - (\frac{4}{5}) log_{2} ( \frac{4}{5} )^2 - (\frac{1}{5} ) log_{2} (\frac{1}{5} ) = 0.7219\) |

| Total |

7 |

13 |

20 |

Expected entropy

= \(\small \frac{15}{20} \times 0.7219 + \frac{5}{20} \times 0.7219\)

= 0.7219 |

Information gain

= \(\small 0.9341 - 0.7219\)

= 0.2121 |

(Age interval 2) that divides into '< 35' and '\(\ge\) 35' has a large information gain, so this interval division

is selected.

The above method can also be applied if you want to reduce the number of categories when there are multiple values

for a categorical variable. For example, if there are three categorical variable values, (\(A_{1}, A_{2}, A_{3}\)),

and we want to reduce them to two, we can investigate the information gain for the three possible combinations

(\(A_{1}, A_{2} : A_{3}\)), (\(A_{1}, A_{3} : A_{2}\)), (\(A_{2}, A_{3} : A_{1}\)) and select the combination

that maximizes the information gain.

6.2.4 Overfitting and pruning decision tree

Decision tree models can have an overfitting problem, classifying training data well but not good for testing data.

Pruning is one way to solve the problem of overfitting, and there are pre-pruning and post-pruning. Pre-pruning

is to examine the appropriateness of the division using chi-square tests and information gain to prevent

meaningless divisions from continuing. Regardless of which method is applied, a threshold value must be set,

which must be determined by the researcher. If the threshold value is too high, a simple tree will be formed,

and conversely, if it is too low, a complex tree may be formed.

Post-pruning is a method of removing branches from a completed tree. For example, when pruning subtrees

for each node, the expected error rate is calculated, and if this value is the maximum expected error rate,

the subtrees are maintained. Otherwise, they are pruned. Pre-pruning and post-pruning are sometimes used in combination.

Characteristics of decision tree model

The important characteristics of the decision tree classification model are summarized as follows:

1) The decision tree model is a nonparametric method that does not assume the distribution function of each group.

2) The results of the decision tree model are easy to explain to anyone. The accuracy of the model is not inferior to other classification models.

3) Since the method of creating a decision tree is not computationally complex, it can be created quickly, even for large amounts of data. Once a decision tree is created, the task of classifying data whose group affiliation is unknown into one group is very fast.

4) The decision tree algorithm can classify abnormal noise data without much sensitivity.

5) Even if there are other unnecessary variables that are highly correlated with one variable, the decision tree

is not greatly affected. However, if there are many unnecessary variables, there is a risk that the decision tree

will become too large. It is necessary to remove unnecessary variables before classification to prevent the risk.

6) Since the number of decision trees that can be created from one data is very large, it is not easy to find

the optimal decision tree among them. Most decision tree algorithms use heuristic search to find the optimal tree,

and the Algorithm we discussed also expands the decision tree using a top-down iterative partitioning strategy.

7) Since most decision tree algorithms are top-down iterative partitioning algorithms, they continuously partition

the entire data set into smaller data sets. If this process is repeated, there may be too few data in some leaves

to make a statistically meaningful classification decision. It is necessary to create a stopping rule that

prevents further partitioning when the number of data in a node is less than a certain number.

8) In the entire decision tree, small trees (subtrees) with the same shape can appear in multiple nodes,

which can complicate the decision tree.

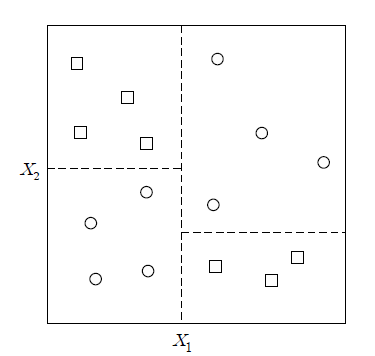

9) A decision tree examines only the conditions for one variable in one node. Therefore, the classification rule

of the decision tree partitions the entire decision space into straight lines parallel to the coordinate axes (variables)

(<Figure 6.2.10>).

<Figure 6.2.10> Split two dimension decision space by a decision tree

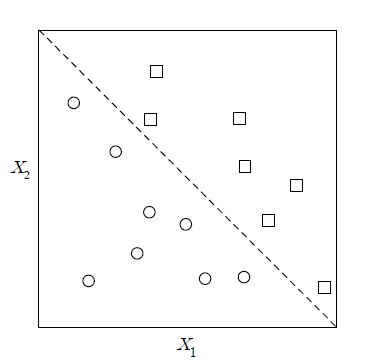

However, the example data in <Figure 6.2.11> is not easy to split by a decision tree.

The test condition at the node can be transformed into one for more than one variable to solve the problem,.

For example, a diagonal shape like <Figure 6.2.11> can be considered as a test condition for two variables.

It would be good to create a test condition for more than two variables, but the calculation is complicated

and another problem of ‘how to create the optimal test condition?’ arises.

<Figure 6.2.11> Example data which is not easy to split by a decision tree

10) The choice of uncertainty measures such as entropy or Gini coefficient does not have a significant effect

on the performance of the decision tree. This is because the measures have similar characteristics.

What affects the performance of the decision tree is the choice of the tree pruning method rather than

the choice of measure.

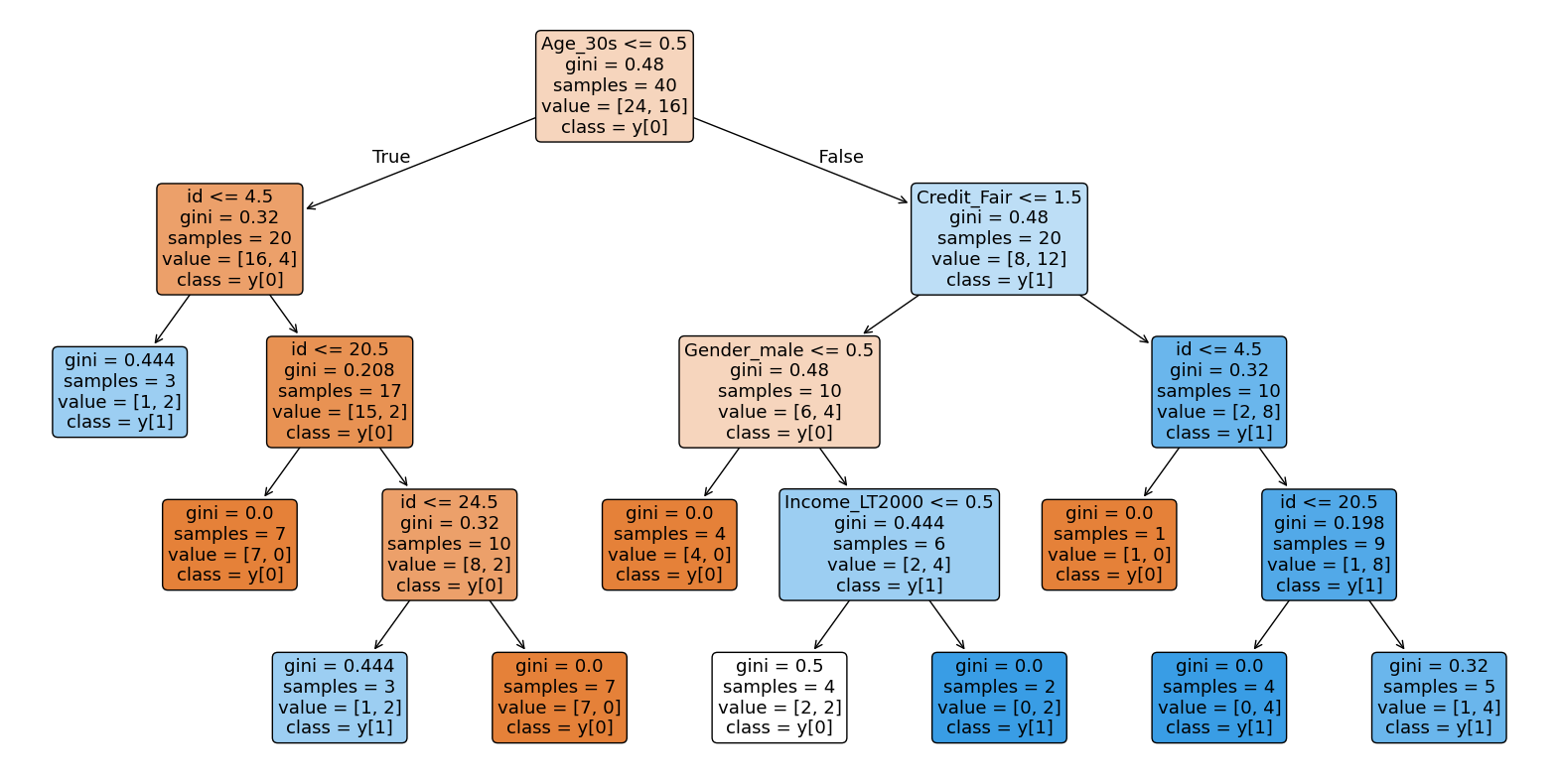

6.2.5 R and Python practice

Let us practice R commands using the data saved at http://estat.me/estat/Example/DataScience/PurchaseByCredit20.csv.

The file format is a comma separated value (csv) type. You can find this file

from 『eStat』 system. Click Ex > DataScience and then click the data 'PurchaseByCredit20.csv'.

After this file is loaded to 『eStat』, save it using 'csv Save' button. It will be

saved at the Download folder on your PC. Copy this file to C:\Rwork\ folder.

In order to practice the decision tree using this data, you need to change first the working directory of R

as follows.

File > Change Directory > C: > Rwork

If you read the data file in R, it looks like as follows.

| # read the data file |

| card <- read.csv("http://estat.me/estat/Example/DataScience/PurchaseByCredit20.csv", header=T, as.is=FALSE) |

card

id Gender Age Income Credit Purchase

1 1 male 20s LT2000 Fair Yes

2 2 female 30s GE2000 Good No

3 3 female 20s GE2000 Fair No

4 4 female 20s GE2000 Fair Yes

5 5 female 20s LT2000 Bad No

6 6 female 30s GE2000 Fair No

7 7 female 30s GE2000 Good Yes

8 8 male 20s LT2000 Fair No

9 9 female 20s GE2000 Good No

10 10 male 30s GE2000 Fair Yes

11 11 female 30s GE2000 Good Yes

12 12 female 20s LT2000 Fair No

13 13 male 30s GE2000 Fair No

14 14 male 30s LT2000 Fair Yes

15 15 female 30s GE2000 Good Yes

16 16 female 30s GE2000 Fair No

17 17 female 20s GE2000 Bad No

18 18 male 20s GE2000 Bad No

19 19 male 30s GE2000 Good Yes

20 20 male 20s LT2000 Fair No

|

| attach(card) |

To analyze decision trees using R, you need to install a package called

rpart. From the main menu of R,

select ‘Package’ => ‘Install package(s)’, and a window called ‘CRAN mirror’ will appear. Here,

select ‘0-Cloud [https]’ and click ‘OK’. Then, when the window called ‘Packages’ appears, select

‘rpart’ and click ‘OK’.

'rpart' is a package for modeling of Recursive Partitioning and Regression Trees and general usage and

key arguments of the function are described in the following table.

Fit a Recursive Partitioning and Regression Trees

|

|

rpart(formula, data, weights, subset, na.action = na.rpart, method, model = FALSE, x = FALSE, y = TRUE, parms, control, cost, ...)

|

| formula |

a formula, with a response but no interaction terms. If this a a data frame, that is taken as the model frame (see model.frame). |

| data |

an optional data frame in which to interpret the variables named in the formula. |

| method |

one of "anova", "poisson", "class" or "exp". If method is missing then the routine tries to make an intelligent guess. If y is a survival object, then method = "exp" is assumed, if y has 2 columns then method = "poisson" is assumed, if y is a factor then method = "class" is assumed, otherwise method = "anova" is assumed. It is wisest to specify the method directly, especially as more criteria may added to the function in future. |

| parms |

optional parameters for the splitting function.

Anova splitting has no parameters.

Poisson splitting has a single parameter, the coefficient of variation of the prior distribution on the rates. The default value is 1.

Exponential splitting has the same parameter as Poisson.

For classification splitting, the list can contain any of: the vector of prior probabilities (component prior), the loss matrix (component loss) or the splitting index (component split). The priors must be positive and sum to 1. The loss matrix must have zeros on the diagonal and positive off-diagonal elements. The splitting index can be gini or information. The default priors are proportional to the data counts, the losses default to 1, and the split defaults to gini.

|

| control |

a list of options that control details of the rpart algorithm. See rpart.control. |

| rpart.control(minsplit = 20, minbucket = round(minsplit/3), cp = 0.01,

maxcompete = 4, maxsurrogate = 5, usesurrogate = 2, xval = 10,

surrogatestyle = 0, maxdepth = 30, ...)

|

| minsplit |

the minimum number of observations that must exist in a node in order for a split to be attempted. |

| minbucket |

the minimum number of observations in any terminal node. If only one of minbucket or minsplit is specified, the code either sets minsplit to minbucket*3 or minbucket to minsplit/3, as appropriate. |

| cp |

complexity parameter. Any split that does not decrease the overall lack of fit by a factor of cp is not attempted. For instance, with anova splitting, this means that the overall R-squared must increase by cp at each step. The main role of this parameter is to save computing time by pruning off splits that are obviously not worthwhile. Essentially,the user informs the program that any split which does not improve the fit by cp will likely be pruned off by cross-validation, and that hence the program need not pursue it. |

| maxdepth |

Set the maximum depth of any node of the final tree, with the root node counted as depth 0. Values greater than 30 rpart will give nonsense results on 32-bit machines.

|

An example of R commands for a decision tree using the dataset card is as follows.

The results of practicing a decision tree in R with purchase as the dependent variable of card data

and other variables as independent variables are as follows. In Example 6.2.5, the information gain

of credit status was the largest, so this variable was the root node. However, since some of the number of data

belonging to credit status variable value was small (‘bad’ = 3, ‘good’ = 6, ), the next largest information gain,

which is age, was selected as the root node in R.

| install.packages('rpart') |

| library(rpart) |

| fit <- rpart(Purchase ~ Gender + Age + Income + Credit, data = card) |

fit

n= 20

node), split, n, loss, yval, (yprob)

* denotes terminal node

1) root 20 8 No (0.6000000 0.4000000)

2) Age=20s 10 2 No (0.8000000 0.2000000) *

3) Age=30s 10 4 Yes (0.4000000 0.6000000)

|

However, the analysis result is simple because the minimum number of pruning data of the rpart function is 20

or more by default. Let's change this default setting and prune it.

The results of practicing decision trees in R with purchase as the dependent variable of card data

and other variables as independent variables are as follows.

| fit2 <- rpart(Purchase ~ Gender + Age + Income + Credit, data = card, control = rpart.control(minsplit = 6)) |

fit2

n= 20

node), split, n, loss, yval, (yprob)

* denotes terminal node

1) root 20 8 No (0.6000000 0.4000000)

2) Age=20s 10 2 No (0.8000000 0.2000000) *

3) Age=30s 10 4 Yes (0.4000000 0.6000000)

6) Credit=Fair 5 2 No (0.6000000 0.4000000) *

7) Credit=Good 5 1 Yes (0.2000000 0.8000000) *

|

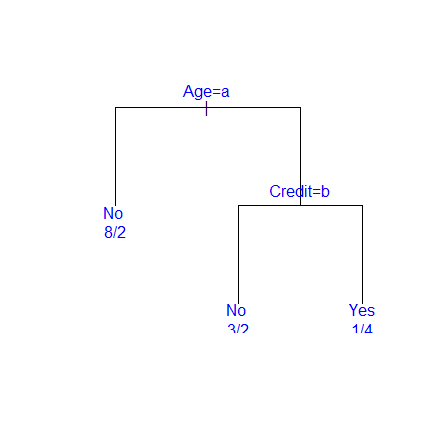

To draw a decision tree as a graph, use the plot and text commands below.

'plot' draws a tree diagram and, if the option 'compress' is T, the vertical width is narrowed,

and if 'uniform' is T, the horizontal width is narrowed. 'margin' sets the margin.

If the margin is 0, the label may be cut off, so set it little by little.

'text' labels the tree, and 'use.n' displays something like 0/4. The decision tree drawn with the above command is as follows.

| plot(fit2,compress=T,uniform=T,margin=0.1) |

text(fit2,use.n=T,col='blue')

<Figure 6.2.12> Decision tree using R

|

In the decision tree diagram above, age=a is the condition of the left branch, and 'a' means the first variable value '20s',

credit=b is also the condition of the left branch, and 'b' means 'fair'

(in this case, it seems to have been merged because 'bad' is missing).

For more information, please refer to the help. In packages such as R, when the number of data corresponding to each variable value

is too small, pruning is determined by merging with adjacent variable values.

Python practice

[Colab]

# Import required libraries

import pandas as pd

import matplotlib.pyplot as plt

# Read the data file

url = 'https://raw.githubusercontent.com/ogut77/DataScience/refs/heads/main/PurchaseByCredit40.csv'

card = pd.read_csv(url)

# Display the data

print(card)

id Gender Age Income Credit Purchase

0 1 male 20s LT2000 Fair Yes

1 2 female 30s GE2000 Good No

2 3 female 20s GE2000 Fair No

3 4 female 20s GE2000 Fair Yes

4 5 female 20s LT2000 Bad No

5 6 female 30s GE2000 Fair No

6 7 female 30s GE2000 Good Yes

7 8 male 20s LT2000 Fair No

8 9 female 20s GE2000 Good No

9 10 male 30s GE2000 Fair Yes

10 11 female 30s GE2000 Good Yes

11 12 female 20s LT2000 Fair No

12 13 male 30s GE2000 Fair No

13 14 male 30s LT2000 Fair Yes

14 15 female 30s GE2000 Good Yes

15 16 female 30s GE2000 Fair No

16 17 female 20s GE2000 Bad No

17 18 male 20s GE2000 Bad No

18 19 male 30s GE2000 Good Yes

19 20 male 20s LT2000 Fair No

20 21 male 20s LT2000 Fair Yes

21 22 female 30s GE2000 Good No

22 23 female 20s GE2000 Fair No

23 24 female 20s GE2000 Fair Yes

24 25 female 20s LT2000 Bad No

25 26 female 30s GE2000 Fair No

26 27 female 30s GE2000 Good Yes

27 28 male 20s LT2000 Fair No

28 29 female 20s GE2000 Good No

29 30 male 30s GE2000 Fair Yes

30 31 female 30s GE2000 Good Yes

31 32 female 20s LT2000 Fair No

32 33 male 30s GE2000 Fair No

33 34 male 30s LT2000 Fair Yes

34 35 female 30s GE2000 Good Yes

35 36 female 30s GE2000 Fair No

36 37 female 20s GE2000 Bad No

37 38 male 20s GE2000 Bad No

38 39 male 30s GE2000 Good Yes

39 40 male 20s LT2000 Fair No

# Prepare the data

y=card['Purchase']

X=card.drop(['Purchase'], axis=1)

# X=pd.get_dummies(X,drop_first=True)

# Prepare the data

for column in X.select_dtypes(include=['object']).columns:

X[column] = label_encoder.fit_transform(X[column])

# Create and train the decision tree model

dt = DecisionTreeClassifier()

fit = dt.fit(X, y)

fit

DecisionTreeClassifier()

In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

dt = DecisionTreeClassifier(min_samples_split=6, random_state=42) #Added random_state for reproducibility

fit2 = dt.fit(X, y) #Fit on the training data

fit2

DecisionTreeClassifier(min_samples_split=6, random_state=42)

In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

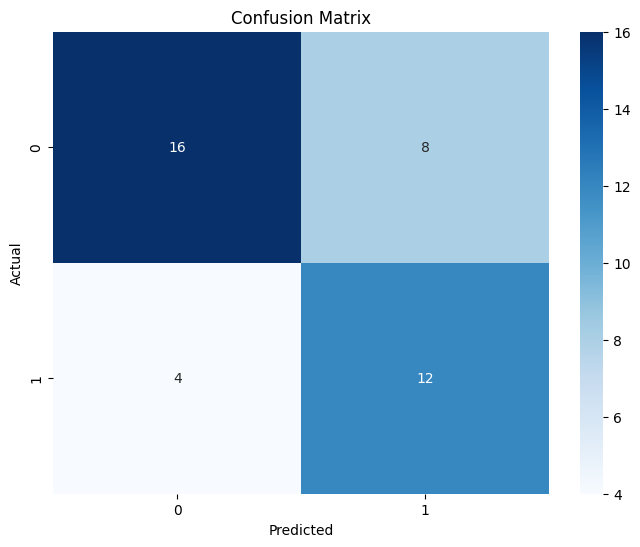

# prompt: plot(fit2,compress=T,uniform=T,margin=0.1)

# text(fit2,use.n=T,col='blue') in python

import matplotlib.pyplot as plt

from sklearn.tree import plot_tree