Chapter 7. Supervised machine learning for continuous data

CHAPTER OBJECTIVES

Classification analysis is a technique that uses data with known group membership to create a model

to determine the group of data with unknown group membership. This chapter

introduces the classification analysis for continuous data as follows.

• Bayes classification model, which is the basis of statistical classification analysis.

• Logistic regression model in case of two groups uses multiple linear regression analysis.

• Nearest neighbor classification model, which utilizes distances between observations.

• Neural network model, which is a nonlinear optimization model.

• Support vector machine model, which is a mathematical classification model.

• Ensemble models that synthesize the results of several classification models.

7.1 Bayes Classification Model - Continuous data

In section 6.3.1, we studied the Bayes classification model, which classifies data into groups

with high probability by calculating the posterior probability using Bayes theorem.

In section 6.3.2, we studied the naive Bayes classification model, which is an application of

Bayes classification to categorical data when variables can be assumed to be independent.

Suppose there are \(m\) random variables \(\small \boldsymbol X = (X_{1}, X_{2}, ... , X_{m}) \).

Let the prior probabilities of \(k\) number of groups,

\(\small G_{1}, G_{2}, ... , G_{k}\), be \(\small P(G_{1}), P(G_{2}), ... , P(G_{k})\), and let the likelihood

probability distribution function for each group be \(\small P(X | G_{1}), P(X | G_{2}), ... , P(X | G_{k})\).

Given the observation data \(\small \boldsymbol x\) for classification, the posterior probability

\(\small P(G_{i} | \boldsymbol x)\) that this data comes from the group \(\small G_{i}\) is as follows.

$$ \small

P( G_{i} | \boldsymbol x ) = \frac {P( G_{i} ) \times P(\boldsymbol x | G_{i})}{P(G_{1}) \times P(\boldsymbol x |G_{1}) + P(G_{2}) \times P(\boldsymbol x | G_{2}) + \cdots + P(G_{k}) \times P(\boldsymbol x | G_{k}) }

$$

The Bayes classification rule, which uses the posterior probability, is as follow.

Bayes Classification - multiple groups

Suppose that prior probabilities of \(k\) number of groups, \(\small G_{1}, G_{2}, ... , G_{k}\), are

\(\small P(G_{1}), P(G_{2}), ... , P(G_{k})\), and likelihood probability distribution functions

for each group are \(\small P(X | G_{1}), P(X | G_{2}), ... , P(X | G_{k})\).

Given the observation data \(\small \boldsymbol x\) for classification, let the posterior probabilities

that \(\small \boldsymbol x\) comes from each group be

\(\small P(G_{1} | \boldsymbol x), P(G_{2} | \boldsymbol x), ... , P(G_{k} | \boldsymbol x)\).

The Bayes classification rule is as follows.

\(\qquad\) 'Classify \(\boldsymbol x\) into a group with the highest posterior probability'

If we denote the likelihood probability functions as

\(\small f_{1}(\boldsymbol x), f_{2}(\boldsymbol x), ... , f_{k}(\boldsymbol x)\),

since the denominators in the calculation of posterior probabilities are the same, the Bayes classification rule

can be written as follows.

\(\qquad\) 'If \(\small P(G_{k}) f_{k}(\boldsymbol x) ≥ P(G_{i}) f_{i}(\boldsymbol x) \) for all \(k\) ≠ \(i\),

classify \(\boldsymbol x\) into group \(\small G_{k}\)'

If there are only two groups \(\small G_{1}\)and \(\small G_{2}\), the Bayesian classification rule is expressed as follows.

\(\qquad\) 'if \( \frac{f_{1}(\boldsymbol x)}{f_{2}(\boldsymbol x)} ≥ \frac{P(G_{2})}{P(G_{1})} \),

classify \(\boldsymbol x\) into group \(\small G_{1}\), else into group \(\small G_{2}\)'

When there are sample data, we can estimate the likelihood probability distribution \(f_{i}(\boldsymbol x)\)

from the sample, the Bayes classification rule can also be estimated using the likelihood distribution.

Therefore, the Bayes classification rule can appear in many variations depending on the estimation method of

the likelihood probability distribution. Estimating the likelihood probability distribution using samples

can be done using either a parametric method, such as maximum likelihood estimation, or a nonparametric method.

In the case of categorical data, a multidimensional distribution estimated from the sample is often used,

and in the case of continuous data, a multivariate normal distribution is often used.

For more information, please refer to the related references.

Example 7.1.1 - Bayes classification with one continuous variable

A survey of customers at a computer store showed the prior probabilities of the purchasing group (\(\small G_{1}\))

and the non-purchasing group (\(\small G_{2}\)) are \(\small P(G_{1})\) = 0.4 and \(\small P(G_{2})\) = 0.6, respectively.

Suppose that the likelihood distribution of the age in the purchasing group is a normal distribution with a mean of 35

and a standard deviation of 2, \(\small N(35, 2^{2})\), and the non-purchasing group is a normal distribution

with a mean of 25 and a standard deviation of 2, \(\small N(25, 2^{2})\).

If a customer who visited this store on a certain day is 30 years old,

classify the customer using the Bayes classification model whether he will purchase the product or not.

Answer

The functional form of the likelihood probability distribution of the purchasing group \(\small G_{1}\)

and the non-purchasing group \(\small G_{2}\) are as follows.

$$ \small

\begin{align}

P(x | G_{1}) = f_1 (x) &= \frac{1}{\sqrt{2 \pi} \; 2} \; exp \{ - \; \frac{(x - 35)^2}{2 \times 2^2} \} \\

P(x | G_{2}) = f_2 (x) &= \frac{1}{\sqrt{2 \pi} \; 2} \; exp \{ - \; \frac{(x - 25)^2}{2 \times 2^2} \}

\end{align}

$$

Therefore, the Bayes classification rule is as follows.

$$ \small

\text{If} \;\; \frac{f_1 (x)}{f_2 (x)} \;=\; exp \{ - \; \frac{(x - 35)^2}{2 \times 2^2} - \; \frac{(x - 25)^2}{2 \times 2^2} \} \; \ge \; \frac{P(G_2)}{P(G_1)} \;=\; \frac{0.6}{0.4}, \; \text{classify} \; x \; \text{into} \; G_{1}, \; \text{else} \; G_{2}.

$$

If we organize the above equation by taking the log, the classification rule is as follows.

$$ \small

\text{If} \;\; x \ge \; 30.16, \; \text{classify} \; x \; \text{into} \; G_{1}, \; \text{else} \; G_{2}.

$$

Therefore, the customer whose age is 30 is classified as a non-purchasing group (\(G_{2}\)).

If there are two groups, \(\small G_{1}\) and \(\small G_{2}\), and the likelihood probability distributions

\(\small f_{1} (\boldsymbol x)\) and \(\small f_{2} (\boldsymbol x)\) for each group follow

the multivariate normal distribution \(\small N(\boldsymbol \mu_{1}, \Sigma_{1})\) and \(\small N(\boldsymbol \mu_{2}, \Sigma_{2})\),

the classification rule is as follows.

$$ \small

\text{If}\;\; d^Q (\boldsymbol x) \;=\; - \frac{1}{2} \; ln \; \frac{|\Sigma_{2}|}{|\Sigma_{1}|} \;-\; \frac{1}{2} (\boldsymbol x - \boldsymbol \mu_{1})' \Sigma_{1}^{-1} (\boldsymbol x - \boldsymbol \mu_{1} ) \;+\; \frac{1}{2} (\boldsymbol x - \boldsymbol \mu_{2})' \Sigma_{2}^{-1} (\boldsymbol x - \boldsymbol \mu_{2} ) \; \ge \; ln \; \frac{P(G_2)}{P(G_1)}, \; \text{classify} \; x \; \text{into} \; G_{1}, \; \text{else} \; G_{2}.

$$

\( d^Q (\boldsymbol x) \) is a quadratic classification function.

If the covariances of groups \(\small G_{1}\) and \(\small G_{2}\) are the same (i.e.,

\(\Sigma_{1} = \Sigma_{2} = \Sigma \)), the classification function \( d^Q (\boldsymbol x) \)

becomes the following linear classification function

\( d^L (\boldsymbol x) \), which is widely used in the classification of continuous data.

$$ \small

\text{If}\;\; d^L (\boldsymbol x) \;=\; (\boldsymbol \mu_1 - \boldsymbol \mu_2)' \; \Sigma^{-1} \; [\; \boldsymbol x \;-\; \frac{1}{2} ( \boldsymbol \mu_{1} + \boldsymbol \mu_{2}) \;] \; \ge \; ln \; \frac{P(G_2)}{P(G_1)}, \; \text{classify} \; x \; \text{into} \; G_{1}, \; \text{else} \; G_{2}.

$$

Since the two means, \(\small \mu_1\) and \(\small \mu_2\), and covariance matrix \(\small \Sigma\) of the two populations

are generally unknown, an estimated classification function is used using the sample means, \(\overline {\boldsymbol x}_1\) and \(\overline {\boldsymbol x}_2\),

and sample covariance matrix \(\small S\) from each population.

$$ \small

\text{If}\;\; d^L (\boldsymbol x) \;=\; (\overline {\boldsymbol x}_1 - \overline {\boldsymbol x}_2)' \; S^{-1} \; [\; \boldsymbol x \;-\; \frac{1}{2} ( \overline {\boldsymbol x}_{1} + \overline {\boldsymbol x}_{2}) \;] \; \ge \; ln \; \frac{P(G_2)}{P(G_1)}, \; \text{classify} \; x \; \text{into} \; G_{1}, \; \text{else} \; G_{2}.

$$

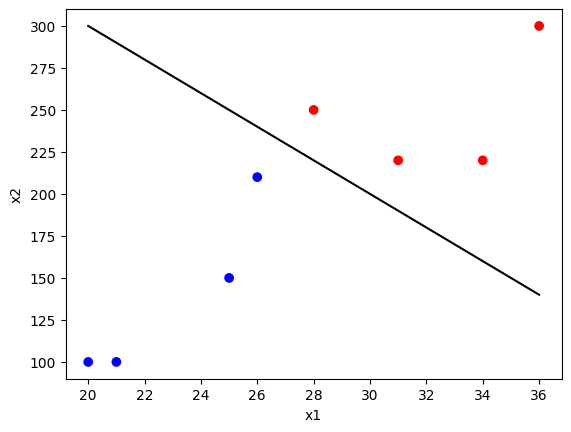

Example 7.1.2

Consider a survey of 20 customers at a computer store on age (\(\small X_{1}\)), monthly income (\(\small X_{2}\)),

and purchasing status, as shown in Table 7.1.1.

Assume that these continuous variables are multivariate normal distributions with the same covariance.

Find a Bayes classification function and classify a customer who is 33 years old and has a monthly income of 200,

whether he will purchase a computer or not.

| Table 7.1.1 Survey of customers on age, income, and purchasing status |

| Number |

Age |

Income

(unit 10,000 won) |

Purchase |

| 1 | 25 | 150 | Yes |

| 2 | 34 | 220 | No |

| 3 | 27 | 210 | No |

| 4 | 28 | 250 | Yes |

| 5 | 21 | 100 | No |

| 6 | 31 | 220 | No |

| 7 | 36 | 300 | Yes |

| 8 | 20 | 100 | No |

| 9 | 29 | 220 | No |

| 10 | 32 | 250 | Yes |

| 11 | 37 | 400 | Yes |

| 12 | 24 | 120 | No |

| 13 | 33 | 350 | No |

| 14 | 30 | 180 | Yes |

| 15 | 38 | 350 | Yes |

| 16 | 32 | 250 | No |

| 17 | 28 | 240 | No |

| 18 | 22 | 220 | No |

| 19 | 39 | 450 | Yes |

| 20 | 26 | 150 | No |

Answer

The sample means of age and income of each group, \( \overline {\boldsymbol x}_1\) and \( \overline {\boldsymbol x}_2\),

and sample covariance matrix \(\small \boldsymbol S\) are calculated as follows.

$$ \small

\qquad \overline {\boldsymbol x}_1 \; = \; \left[ \matrix{27.250 \cr 200.000} \right], \qquad \overline x_2 \; = \; \left[ \matrix{33.125 \cr 291.250} \right], \qquad \boldsymbol S \; = \; \left[ \matrix{31.621 & 470.105 \cr 470.105 & 9129.211} \right]

$$

\(\small \overline {\boldsymbol x}_1 - \overline {\boldsymbol x}_2\), \(\small \boldsymbol S^{-1}\) and \(\small ( \overline {\boldsymbol x}_1 - \overline {\boldsymbol x}_2 )' \boldsymbol S^{-1}\) is as follows.

$$ \small

\qquad \overline {\boldsymbol x}_1 - \overline {\boldsymbol x}_2 \; = \; \left[ \matrix{-5.875 \cr -91.25} \right], \qquad \boldsymbol S^{-1} = \left[ \matrix{0.134895 & -0.006946 \cr -0.006946 & 0.000467} \right], \qquad ( \overline {\boldsymbol x}_1 - \overline {\boldsymbol x}_2 )' \boldsymbol S^{-1} = \left [ \matrix{ -0.15865 \cr -0.00182} \right ]

$$

Assume that the prior probability of non-purchasing group is \(\small P(G_{1})\) = 0.6, and the prior probability of

purchasing group \(\small P(G_{2})\) = 0.4, the sample linear classification function is as follows.

$$ \small

\text{If}\;\; (-0.15865) \times x_{1} + (-0.00182) \times x_{2} + 5.64297 \; \ge \; 0, \; \text{classify} \; \boldsymbol x = (x_{1}, x_{2}) \; \text{into} \; G_{1}, \; \text{or} \; G_{2}.

$$

If the visiting customer's age is 33 and income is 200, the classification function becomes as follows.

$$ \small

(-0.15865)*(33) + (0.00182) * (200) + (5.64297) = 0.04251

$$

Therefore, the customer is classified into the non-purchasing group \(\small G_{1}\).

[]

If we can estimate the likelihood probability distribution, Bayes classification can be applied even

when the variables are continuous or discrete. If continuous and discrete variables are mixed,

the naive Bayes classification can be applied by discretizing the continuous variables.

Variable selection

When there are many variables, selecting only the variables that help classify the groups

can reduce the parameter estimation problem and increase accuracy.

Stepwise classification analysis is selecting appropriate variables stepwise and classifying them.

Variable selection generally uses variables that can best explain group variables, that is, variables

with high discriminatory power between groups. For example, when performing an analysis of variance

to compare the means between groups, variables with high F values (or t values in the case of two groups) are selected.

This type of variable selection can be done by forward selection, which adds variables with high discriminatory power

one by one without selecting any variables, and backward elimination, which selects all variables and then removes variables

with low discriminatory power one by one. There is also a stepwise method that selects variables using

the forward selection method while examining whether the variables already selected can be removed.

However, it is not easy to verify whether the ‘optimal’ variable selection has been made regardless of the method used.

For more information, please refer to the references.

Characteristics of Bayes classification

The characteristics of Bayes classification are summarized as follows.

1) Since the Bayes classification model classifies using the posterior probability, which is calculated by

the prior probability and the likelihood probability distribution of each group, the risk of model overfitting

is low and robust.

2) Bayes classification model can perform stable classification even when incomplete data,

outliers, and missing values exist.

7.1.1 R and Python practice - Bayes classification

To analyze Bayes classification using R, we need to install a package called

MASS.

From the main menu of R,

select ‘Package’ => ‘Install package(s)’, and a window called ‘CRAN mirror’ will appear. Here,

select ‘0-Cloud [https]’ and click ‘OK’. Then, when the window called ‘Packages’ appears, select

‘MASS’ and click ‘OK’. 'MASS' is a package for modeling of Bayes classification model.

General usage and key arguments of the function are described in the following table.

Fit a linear discriminant analysis model.

|

lda(x, ...)

## S3 method for class 'formula'

lda(formula, data, ..., subset, na.action)

## Default S3 method:

lda(x, grouping, prior = proportions, tol = 1.0e-4,method, CV = FALSE, nu, ...)

## S3 method for class 'data.frame'

lda(x, ...)

## S3 method for class 'matrix'

lda(x, grouping, ..., subset, na.action)

|

| formula |

A formula of the form groups ~ x1 + x2 + ... That is, the response is the grouping factor and the right hand side specifies the (non-factor) discriminators. |

| data |

Data frame from which variables specified in formula are preferentially to be taken. |

| x |

(required if no formula is given as the principal argument.) a matrix or data frame or Matrix containing the explanatory variables. |

| grouping |

(required if no formula principal argument is given.) a factor specifying the class for each observation. |

| prior |

the prior probabilities of class membership. If unspecified, the class proportions for the training set are used. If present, the probabilities should be specified in the order of the factor levels. |

| tol |

A tolerance to decide if a matrix is singular; it will reject variables and linear combinations of unit-variance variables whose variance is less than tol^2. |

| subset |

An index vector specifying the cases to be used in the training sample. (NOTE: If given, this argument must be named.) |

| na.action |

A function to specify the action to be taken if NAs are found. The default action is for the procedure to fail. An alternative is na.omit, which leads to rejection of cases with missing values on any required variable. |

| method |

"moment" for standard estimators of the mean and variance, "mle" for MLEs, "mve" to use cov.mve, or "t" for robust estimates based on a t distribution. |

An example of R commands for a Bayes classification with purchase as the dependent variable of card data

and other variables as independent variables is as follows.

| install.packages('MASS') |

| library(MASS) |

| customer <- read.csv('http://estat.me/estat/Example/DataScience/PurchaseByCredit20_Continuous.csv', header=T, as.is=FALSE) |

| attach(customer) |

Purchase

[1] Yes No No Yes No No Yes No No Yes Yes No No Yes Yes No No No Yes

[20] No

Levels: No Yes

|

| ldamodel <- lda(Purchase ~ ., customer) |

ldamodel

Call: lda(Purchase ~ ., data = customer)

Prior probabilities of groups:

No Yes

0.6 0.4

Group means:

Age Income

No 27.250 200.00

Yes 33.125 291.25

Coefficients of linear discriminants:

LD1

Age 0.173328870

Income 0.001994526

|

If we want to classify the group of the customer data using the Bayes model,

R commands are as follows.

| pred <- predict(ldamodel, customer)" |

pred$class

$class

[1] No Yes No No No No Yes No No No Yes No Yes No Yes No No No Yes

[20] No

Levels: No Yes

|

To make a classification cross table, we can use a vector of prediction, pred$class, and

Purchase with table command as below.

Using this classification table, accuracy of the model is calculated as 0.7

which is (10+4) / (10+2+4+4).

classtable <- table(Purchase,pred$class)

Purchase No Yes

No 10 2

Yes 4 4

|

sum(diag(classtable)) / sum(classtable)

[1] 0.7

|

Python practice

[Colab]

# Import required libraries

import pandas as pd

customer = pd.read_csv('https://raw.githubusercontent.com/ogut77/DataScience/refs/heads/main/PurchaseByCredit20_Continuous.csv')

Age Income Purchase

0 25 150 Yes

1 34 220 No

2 27 210 No

3 28 250 Yes

4 21 100 No

5 31 220 No

6 36 300 Yes

7 20 100 No

8 29 220 No

9 32 250 Yes

10 37 400 Yes

11 24 120 No

12 33 350 No

13 30 180 Yes

14 38 350 Yes

15 32 250 No

16 28 240 No

17 22 220 No

18 39 450 Yes

19 26 150 No

from sklearn.discriminant_analysis import LinearDiscriminantAnalysis

# Separate features (X) and target variable (y)

X = customer.drop('Purchase', axis=1)

y = customer['Purchase']

# Initialize and train the Linear Discriminant Analysis model

lda = LinearDiscriminantAnalysis()

lda.fit(X, y)

# Make predictions on the test set

y_pred = lda.predict(X)

# Evaluate the model (example: accuracy)

# You would typically use more comprehensive evaluation metrics

# depending on your specific needs.

from sklearn.metrics import accuracy_score

from sklearn.metrics import confusion_matrix

accuracy = accuracy_score(y, y_pred)

cm=confusion_matrix(y, y_pred)

print(f"Accuracy: {accuracy}")

print(f"Confusion Matrix: \n{cm}")

Accuracy: 0.7

Confusion Matrix:

[[10 2]

[ 4 4]]

|

7.2 Logistic regression model

A linear regression model expresses the relationship between \(m\) independent variables (explanatory variables)

\(\small X_{1}, X_{2}, ... , X_{m}\) and the dependent variable (response or target variable) \(\small Y\) as a linear

equation as follows.

$$ \small

Y = \beta_{0} + \beta_{1} X_{1} + \beta_{2} X_{2} + \cdots \beta_{m} X_{m} + \epsilon

$$

Here, the error term \(\epsilon\) is assumed to be a normal distribution with a mean of 0 and a variance of

\(\sigma^{2}\). If the target variable \(\small Y\) has values of 0 and 1 representing two groups,

the above regression model is not appropriate. For example, Let us consider a simple linear regression model

to determine whether a customer will purchase a product (\(\small Y\) = 1) or not (\(\small Y\) = 0)

based on monthly income (\(\small X\)).

$$ \small

Y = \alpha + \beta X + \epsilon

$$

If we estimate the parameters \(\small \alpha \) and \(\small \beta \) using sample data and apply

the above formula to actual test data, since the predicted value of group \(\small Y\) becomes a continuous number,

there are cases where it goes beyond the range of [0, 1]. The

logistic regression is a model that

has been modified to fit the classification of two groups by solving this problem of the linear regression model.

When the target variable has the values 1 and 0, the logistic regression model is a linear regression of

the log value of the odds ratio, which is the ratio of the probability \(\small P(Y = 1 \;| x) \) and

the probability \(\small P(Y = 0 \;| x) \) given that \(\small X = x \), as shown below.

$$ \small

ln \; \frac{P(Y = 1 \;| x)}{P(Y = 0 \;| x)} = \alpha + \beta x

$$

Here, \(ln\) is the natural logarithm and \(\small P(Y = 0 \;| x) = 1 - P(Y = 1 \;| x) \).

If we rearrange the above equation using \(\small P(Y = 1 \;| x) \), it can be written as follows.

$$ \small

P(Y = 1 \;| x) = \frac {exp(\alpha + \beta x)}{1 + exp(\alpha + \beta x)}

$$

It means that, if the coefficients \(\small \alpha\) and \(\small \beta\) of this regression model can be estimated

using the least squares method, \(\small P(Y = 1 \;| x) \) can also be estimated.

The estimated probability \(\small P(Y = 1 \;| x) \) is called the posterior probability of the group 1, and

\(\small P(Y = 0 \;| x) \) is called the posterior probability of the group 0.

Data is classified into the group 1 if this posterior probability value is greater than a critical value

selected by the analyst, such as 0.5, otherwise it is classified as group 0.

The maximum likelihood estimation method is frequently used to estimate the coefficient of the logistic regression model.

The above simple logistic regression model with one variable can be extended to have \(m\) variables as follow.

$$ \small

ln \; \frac{P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}) )}{1 - P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}))} = \beta_{0} + \beta_{1} X_{1} + \beta_{2} X_{2} + \cdots \beta_{m} X_{m}

$$

If we rearrange the above equation using \(\small P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}) ) \), it can be written as follow.

$$ \small

P(Y = 1 \;|\; \boldsymbol x = (x_{1}, x_{2}, ... ,x_{m}) ) = \frac {exp(\beta_{0} + \beta_{1} X_{1} + \beta_{2} X_{2} + \cdots + \beta_{m} X_{m})}{1 + exp(\beta_{0} + \beta_{1} X_{1} + \beta_{2} X_{2} + \cdots + \beta_{m} X_{m})}

$$

Given the data \(\small \boldsymbol x = (x_{1}, x_{2}, ... ,x_{m})\) to be classified, the posterior probability

\(\small P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}) ) \) is estimated using the estimated

regression coefficients of \(\small \beta_{0}, \beta_{1}, ... ,\beta_{m}\). If the estimated posterior probability

is greater than the critical value selected by the analyst, it is classified as group 1, otherwise it is classified

as group 0.

Let us examine the effect of independent variable \(\small X_{i}\) on the classification of groups in

the logistic regression model. If all other variables are constant and only the variable value \(\small x_{i}\)

is increased by 1 unit (\(\small x_{i} + 1\)), the incremental odds ratio is as follows.

$$ \small

\begin{align}

\text{Incremental odds ratio} &= \frac{exp(\beta_{0} + \beta_{1} x_{1} + \cdots + \beta_{i} (x_{i}+1) + \cdots + \beta_{m} x_{m})}{exp(\beta_{0} + \beta_{1} x_{1} + \cdots + \beta_{i} x_{i} + \cdots + \beta_{m} x_{m})} \\

&= exp(\beta_{i})

\end{align}

$$

Therefore, when the variable \(\small X_{i}\) increases by 1 unit, if \(\small \beta_{i}\) is positive,

the odds ratio increase rate is greater than 1, so \(\small P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}) ) \)

also increases. On the other hand, if \(\small \beta_{i}\) is negative, the odds ratio increase rate is less than 1,

so \(\small P(Y = 1 \;|\; \boldsymbol x = (x_{1},x_{2}, ... , x_{m}) ) \) decreases. For example,

monthly income \(\small X\) is an independent variable and customer purchasing status \(\small Y\) is

the target variable, such as purchasing a product (\(\small Y = 1\)) or not (\(\small Y = 0\)).

The estimated logistic regression model is as follow.

$$ \small

ln \; \frac{P(Y = 1 \;| x)}{1 - P(Y = 1 \;| x)} = 0.21 + 1.34 x

$$

In this case, if the monthly income \(\small X\) increases by 1 unit, the odds ratio increase rate becomes

\(exp(1.34)\) = 3.82. That is, if monthly income increases by 1 unit, the odd ratio of the probability of purchasing

a product to the probability of not purchasing it increases by 3.82 times.

In the case of a logistic regression model with many independent variables, the variable that best explains

the target variable must be selected. In order to select variables, a model selection criterion that can compare

several models is needed, and the Akaike Information Criteria (AIC) is commonly used. Specific selection methods

include forward selection, backward elimination, and stepwise methods, as in the Bayes classification

variable selection method. For more information, please refer to a related statistics book.

Example 7.2.1 Using the survey data in Example 7.1.2, find a logistic regression model

with product purchase as the target variable and age, monthly income, as independent variables.

Answer

If we perform a logistic regression analysis using R with age (\(\small X_{1}\)) and monthly income

(\(\small X_{2}\)) as independent variables

and purchasing status as a target variable (\(\small Y\)), we will get the results in the following table.

| Coefficients: |

| (Intercept) | Age | Income |

| -7.629959 | 0.223517 | 0.001918 |

This means that the logistic regression model is as follows.

$$ \small

ln \; \frac{P(Y = 1 \;|\; \boldsymbol X = (X_{1}, X_{2}) )}{1 - P(Y = 1 \;|\; \boldsymbol X = (X_{1}, X_{2}))} = -7.629959 + 0.223517 X_{1} + 0.001918 X_{2}

$$

If we rearrange the above equation using \(\small P(Y = 1 \;|\; \boldsymbol X = (X_{1}, X_{2}) ) \), it can be written as follows.

$$ \small

P(Y = 1 \;|\; \boldsymbol X = (X_{1}, X_{2}) ) = \frac {exp(-7.629959 + 0.223517 X_{1} + 0.001918 X_{2} )}{1 + exp(-7.629959 + 0.223517 X_{1} + 0.001918 X_{2} )}

$$

If a customer whose age is 20 and income is 200, \(\small \boldsymbol X = (20, 200) \), the posterior probability

\(\small P(Y = 1 \;|\; \boldsymbol X ) \) is as follows.

$$ \small

\begin{align}

P(Y = 1 \;|\; \boldsymbol X = (20, 200) ) &= \frac {exp(-7.629959 + 0.223517 \times 20 + 0.001918 \times 200 )}{1 + exp(-7.629959 + 0.223517 \times 20 + 0.001918 \times 200 )} \\

&= \frac{0.062286}{1 + 0.062286 } \\

&= 0.058634

\end{align}

$$

If the critical value of the posterior probability is 0.5, then the customer is classified by group 0, which is the

non-purchasing group.

7.2.1 R and Python practice - Logistic regression

Let us practice the logistic regression using R commands with the data saved at

http://estat.me/estat/Example/DataScience/PurchaseByCredit20_Continuous.csv.

In order to practice the decision tree using this data, we need to change first the working directory of R

as follows.

File > Change Directory > C: > Rwork

If we read the data file in R, it looks like as follows.

| # read the data file |

| customer <- read.csv('http://estat.me/estat/Example/DataScience/PurchaseByCredit20_Continuous.csv', header=T, as.is=FALSE) |

customer

Age Income Purchase

1 25 150 Yes

2 34 220 No

3 27 210 No

4 28 250 Yes

5 21 100 No

6 31 220 No

7 36 300 Yes

8 20 100 No

9 29 220 No

10 32 250 Yes

11 37 400 Yes

12 24 120 No

13 33 350 No

14 30 180 Yes

15 38 350 Yes

16 32 250 No

17 28 240 No

18 22 220 No

19 39 450 Yes

20 26 150 No

|

| attach(customer)

|

Purchase

[1] Yes No No Yes No No Yes No No Yes Yes No No Yes Yes No No No Yes

[20] No

Levels: No Yes

|

| logitmodel <- glm(Purchase ~.,family=binomial(link='logit'),data=card) |

logitmodel

Call: glm(formula = Purchase ~ ., family = binomial(link = "logit"), data = card)

Coefficients:

(Intercept) Age Income

-7.629959 0.223517 0.001918

Degrees of Freedom: 19 Total (i.e. Null); 17 Residual

Null Deviance: 26.92

Residual Deviance: 20.68 AIC: 26.68

|

Python practice

[Colab]

# Import required libraries

import pandas as pd

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import train_test_split

from sklearn.metrics import accuracy_score, confusion_matrix

# Load the dataset (assuming it's already loaded as 'customer')

# If not, uncomment the line below

customer = pd.read_csv('https://raw.githubusercontent.com/ogut77/DataScience/refs/heads/main/PurchaseByCredit20_Continuous.csv')

# Separate features (X) and target variable (y)

X = customer.drop('Purchase', axis=1)

y = customer['Purchase']

# Initialize and train the Logistic Regression model

logreg = LogisticRegression() # Specify a solver

logreg.fit(X, y)

print(logreg)

# Make predictions on the test set

y_pred = logreg.predict(X)

# Evaluate the model

accuracy = accuracy_score(y, y_pred)

cm = confusion_matrix(y, y_pred)

print(f"Accuracy: {accuracy}")

print(f"Confusion Matrix:\n{cm}")

|

7.3 Nearest neighbor classification model

Decision tree, Bayes classification, and logistic regression models first establish an appropriate model

from the collected data and then apply it to the data to be classified. These models are called eager learners.

However, the

nearest neighbor classification model establishes a model when

there is data to be classified and is called a lazy learner. In other words, the nearest neighbor

classification model first stores all training data in the computer. When the data is to be classified,

it finds a set of \(k\) data that are most similar to the variable values of the data and classifies the data

into a group with a majority vote in that set. It is called a \(k\)-nearest

neighbor classification model. The similarity between the data to be classified and the training data uses

various mathematical or statistical proximity measures studied in Chapter 3.

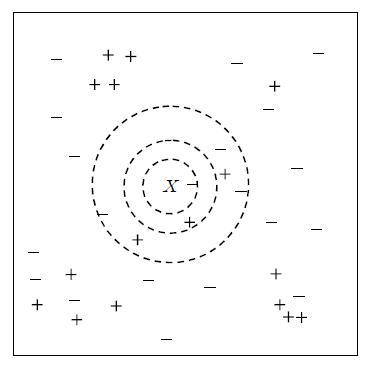

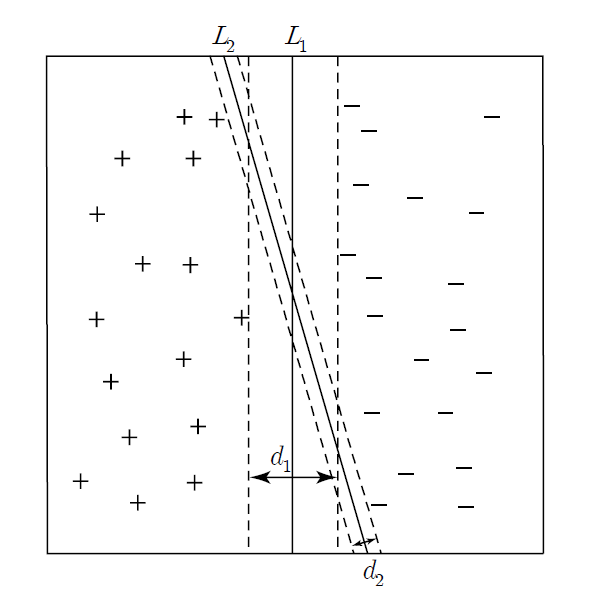

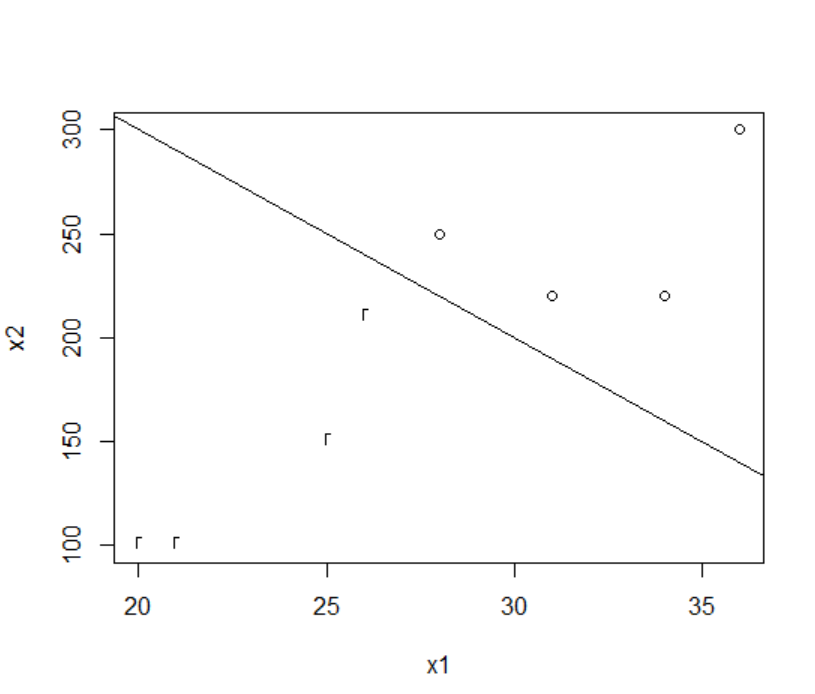

<Figure 7.3.1> shows two-dimensional continuous data divided into + and - groups.

When the data marked with \(\small X\) in the Figure is to be classified, it shows

the 1-nearest neighbor (innermost circle), 2-nearest neighbor (middle circle), and 7-nearest neighbor

(outer circle) data points using the two-dimensional Euclidean distance.

<Figure 7.3.1> 1-nearest, 2-nearest, 7-nearest neighbor data for given data marked with \(\small X\)

If only 1-nearest neighbor is used for classification, there is one - group, and the data \(\small X\)

is classified as the - group. If 2-nearest neighbors are used, there are one + group and one - group data,

so it is difficult to classify the data \(\small X\)

and it can be classified into either group. If 7-nearest neighbors are used, since there are three + groups and four - groups,

the majority rule is used to classify \(\small X\) into the - group.

As seen in these cases, the appropriate selection of \(k\) has a great influence on the classification result.

If \(k\) is too small, the data may be incorrectly classified due to the noise of the data.

If \(k\) is too large, the data may not be classified into a group close to the data.

An algorithm for the nearest neighbor classification model can be summarized as follows.

[

Algorithm for the \(k\) nearest neighbor classification]

Suppose there are \(n\) number of training data with \(m\) variables \(\boldsymbol x_{i}\) and

group variable \(y_i\) as \(\small D = \{(\boldsymbol x_{1}, y_{1}),(\boldsymbol x_{2}, y_{2}), ... , (\boldsymbol x_{n}, y_{n}) \}\).

The algorithm first calculates the similarity distance between the test data \(\boldsymbol x\) to be classified

and all training data. If there is a lot of training data, the calculation of the similarity distance may take

a lot of time. After finding the \(k\) adjacent neighbors \(\small D_{\boldsymbol x}\) using the calculated distance,

the test data \(\boldsymbol x\) is classified into a majority group of these adjacent neighbors,

which can be expressed in the following formula.

$$ \small

y = {argmax}_{v} \; \sum_{(\boldsymbol x_{i}, y_{i}) \in D_{\boldsymbol x}} \; I (v=y_{i})

$$

| Step 1 |

Let \(\boldsymbol x\) be the test data, and \(D = \{(\boldsymbol x_{1}, y_{1}),(\boldsymbol x_{2}, y_{2}), ... , (\boldsymbol x_{n}, y_{n}) \}\)

be the training data. |

| Step 2 |

for test data \(\boldsymbol x\) do |

| Step 3 |

\(\qquad\)for i = 1 to n do |

| Step 4 |

\(\qquad \qquad\)Calculate the distance \(d(\boldsymbol x, \boldsymbol x_{i})\) between \(\boldsymbol x\) and \(\boldsymbol x_{i}\) |

| Step 5 |

\(\qquad\)end for |

| Step 6 |

\(\qquad\)Find the training data set \(D_{\boldsymbol x}\) that is the \(k\) nearest neighbor of \(\boldsymbol x\) |

| Step 7 |

\(\qquad\)Classify \(\boldsymbol x\) into the majority group of \(D_{\boldsymbol x}\), that is

\(\qquad\qquad y = {argmax}_{v} \; \sum_{(\boldsymbol x_{i}, y_{i}) \in D_{\boldsymbol x}} \; I (v=y_{i})\)

|

| Step 8 |

end for |

In this algorthm, when the test data \(\boldsymbol x\) is classified into the majority group of the

\(k\)-nearest neighbor data \(\small D_{\boldsymbol x}\), the distance between \(\boldsymbol x\) and

neighbors \(\boldsymbol x_{i}\) was not considered.

A distance-weighted classification method can be used to compensate for this shortcoming, that has a weighting coefficient

\(\frac{1}{d(\boldsymbol x , \boldsymbol x_{i})^2 }\) which is inversely proportional to the distance.

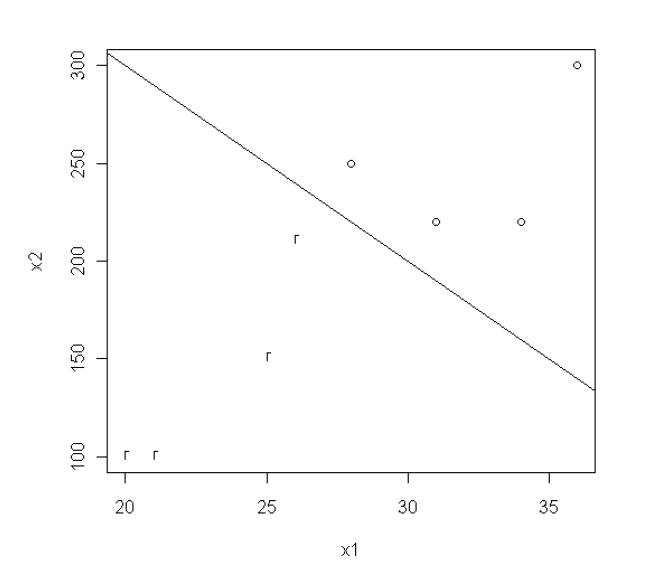

Example 7.3.1 Using the survey data in Example 7.1.2, classify a customer whose age is 33 years old

and has a monthly income of 190 whether he will buy a product or not, using the 5-nearest neighbor classification model.

Answer

Age and monthly income have different measurement units, so they must be converted to the same unit.

Here, the standardization transformation was used using the sample average of age 29.6 and its

sample standard deviation of 5.623, and the sample average of monthly income 236.5, and sample

standard deviation 95.547 as Table 7.3.1. The standardized value of the customer's data

(33, 190) becomes (0.605, -0.487), and Table 7.3.1 shows the squared Euclidean distance between the customer data and all data.

5-nearest neighbors were colored as yellow background which included 3 of 'No's and 2 of 'Yes's.

Therefore, the customer is classified into 'No" which means he will not purchase a product.

| Table 7.3.1 Standardized data of age and income, and squared Euclid distance of the customer |

| Number |

Age |

Income

(unit 10,000 won) |

Purchase |

Standardized

Age |

Standardized

Income |

Squared Euclid

Distance of customer |

| 1 | 25 | 150 | Yes | -0.818 | -0.905 | 2.199 |

| 2 | 34 | 220 | No | 0.782 | -0.173 | 0.130 |

| 3 | 27 | 210 | No | -0.462 | -0.277 | 1.182 |

| 4 | 28 | 250 | Yes | -0.285 | 0.141 | 1.185 |

| 5 | 21 | 100 | No | -1.529 | -1.429 | 5.441 |

| 6 | 31 | 220 | No | 0.249 | -0.173 | 0.225 |

| 7 | 36 | 300 | Yes | 1.138 | 0.665 | 1.610 |

| 8 | 20 | 100 | No | -1.707 | -1.429 | 6.232 |

| 9 | 29 | 220 | No | -0.107 | -0.173 | 0.605 |

| 10 | 32 | 250 | Yes | 0.427 | 0.141 | 0.426 |

| 11 | 37 | 400 | Yes | 1.316 | 1.711 | 5.337 |

| 12 | 24 | 120 | No | -0.996 | -1.219 | 3.098 |

| 13 | 33 | 350 | No | 0.605 | 1.188 | 2.804 |

| 14 | 30 | 180 | Yes | 0.071 | -0.591 | 0.296 |

| 15 | 38 | 350 | Yes | 1.494 | 1.188 | 3.595 |

| 16 | 32 | 250 | No | 0.427 | 0.141 | 0.426 |

| 17 | 28 | 240 | No | -0.285 | 0.037 | 1.064 |

| 18 | 22 | 220 | No | -1.352 | -0.173 | 3.925 |

| 19 | 39 | 450 | Yes | 1.672 | 2.235 | 8.543 |

| 20 | 26 | 150 | No | -0.640 | -0.905 | 1.725 |

Selection of \(k\) on the neighbor classification

The selection of \(k\) in the nearest neighbor classification model is important for an accurate classification.

The following module of eStatU makes it possible to search for a \(k\) value, which shows better accuracy,

sensitivity or specificity on the nearest neighbor classification. \(k\) is selected when there is no

significant increase in accuracy. Since the number of data is small in this example, it is not easy to decide \(k\).

If we select \(k\) = 5, eStat shows the classification result of all training data.

[Nearest neighbor classification]

Characteristics of the neighbor classification model

The characteristics of the nearest neighbor classification model are summarized as follows.

1) The nearest neighbor classification method is based on the data to be classified, so it does not require a special model,

and only requires a measurement of the similarity between this data and the training data.

If the training data increases, it takes a lot of time and effort to calculate the similarity measure,

and, if an appropriate similarity measure is not used, the classification may not be accurate.

2) The nearest neighbor classification method classifies only using local information of the nearest neighbors of the data

to be classified, so if \(k\) is small and there is much noise in the data, the classification may not be accurate.

3) Since the decision boundary determined by the nearest neighbor classification method is not a function,

it is more flexible than the straight or rectangular classification boundary of a decision tree or other models.

However, a boundary that is too dependent on the training data may not help the stability of the classification.

The number of nearest neighbors should be increased or a distance-weighted classification method

should be considered to prevent this problem.

7.3.1 R and Python practice - Nearest neighbor classification

To use k-nearest neighbor (KNN) classification using R, we need to install a package called

DMwR2.

From the main menu of R,

select ‘Package’ => ‘Install package(s)’, and a window called ‘CRAN mirror’ will appear. Here,

select ‘0-Cloud [https]’ and click ‘OK’. Then, when the window called ‘Packages’ appears, select

‘DMwR2’ and click ‘OK’.

General usage and key arguments of the function are described in the following table.

k-nearest neighbor classification model.

This function provides a formula interface to the existing knn() function of package class. On top of this type of convinient interface, the function also allows standardization of the given data.

|

|

kNN(form, train, test, stand = TRUE, stand.stats = NULL, ...)

|

| form |

An object of the class formula describing the functional form of the classification model. |

| train |

The data to be used as training set. |

| test |

The data set for which we want to obtain the k-NN classification, i.e. the test set. |

| stand |

A boolean indicating whether the training data should be previously normalized before obtaining the k-NN predictions (defaults to TRUE). |

| stand.stats |

This argument allows the user to supply the centrality and spread statistics that will drive the standardization. If not supplied they will default to the statistics used in the function scale(). If supplied they should be a list with two components, each beig a vector with as many positions as there are columns in the data set. The first vector should contain the centrality statistics for each column, while the second vector should contain the spread statistc values. |

An example of R commands for a k-neares neighbor classification with customer data as both training and testing

when k= 5 is as follows.

| install.packages('DMwR2') |

| library(DMwR2) |

| customer <- read.csv('http://estat.me/estat/Example/DataScience/PurchaseAgeIncome_Continuous.csv', header=T, as.is=FALSE) |

| attach(customer) |

Purchase

[1] Yes No No Yes No No Yes No No Yes Yes No No Yes Yes No No No Yes

[20] No

Levels: No Yes

|

| nn <- kNN(Purchase ~ ., customer, customer, k=5) |

nn

[1] No No No No No No Yes No No No Yes No Yes No Yes No No No Yes No

Levels: No Yes

|

To make a classification cross table, we can use a vector of Purchase and nn which is the predicted class

with table command as below.

Using this classification table, accuracy of the model is calculated as 0.75

which is (11+4) / (11+1+4+4).

classtable <- table(Purchase, nn)

Purchase No Yes

No 11 1

Yes 4 4

|

sum(diag(classtable)) / sum(classtable)

[1] 0.75

|

Python practice

[Colab]

# Import required libraries

import pandas as pd

from sklearn.metrics import accuracy_score, confusion_matrix

from sklearn.neighbors import KNeighborsClassifier

customer = pd.read_csv('https://raw.githubusercontent.com/ogut77/DataScience/refs/heads/main/PurchaseByCredit20_Continuous.csv')

# Separate features (X) and target variable (y)

X = customer.drop('Purchase', axis=1)

y = customer['Purchase']

# Initialize and train the KNN model

knn = KNeighborsClassifier(n_neighbors=5) # You can adjust the number of neighbors

knn.fit(X, y)

# Make predictions on the test set

y_pred = knn.predict(X)

# Evaluate the model

accuracy = accuracy_score(y, y_pred)

cm = confusion_matrix(y, y_pred)

print(f"KNN Accuracy: {accuracy}")

print(f"KNN Confusion Matrix:\n{cm}")

|

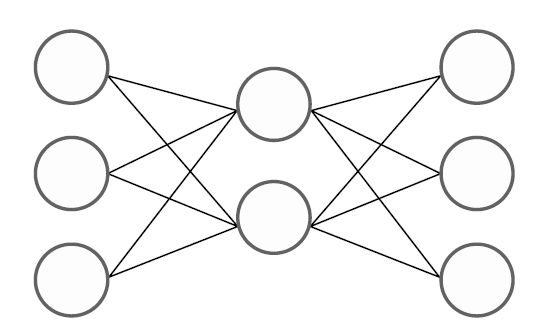

7.4 Artificial neural network model

The

artificial neural network model is a model that imitates the way the human brain makes decisions and classifies them.

It is said that the human brain is composed of a neural network in which \(10^{11}\) neurons are connected to each other.

When one neuron is stimulated, this stimulation is transmitted to other neurons and the information held

by multiple neurons is synthesized to make a decision. The neural network model connects multiple nodes

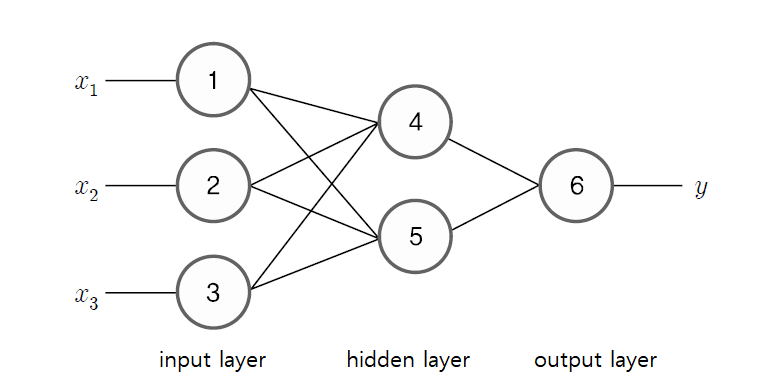

into a network similar to the human brain and makes decisions to classify data, as in <Figure 7.4.1>.

<Figure 7.4.1> Neural network model connects multiple nodes into a network

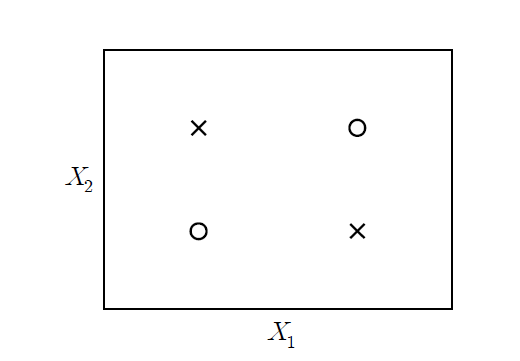

The artificial neural network model is a model that uses a generalized nonlinear function as a classification function.

The motivation for studying this model is the simple two-group (denoted as o and x) two-dimensional data

as in <Figure 7.4.2>. This data cannot be separated into two groups o and x by a single straight line

(not linearly separable), and can only be separated by two straight lines or nonlinear functions.

<Figure 7.4.2> Two-dimensional data which cannot be separated into two groups o and x by a single straight line

There are many types of nonlinear functions for classification, so many studies have been conducted

on classification models using generalized nonlinear functions. In 1957, Rosenbalatt of Cornell Aeronautical Laboratory

in the United States used a single-layer neural network model called a perceptron

for character recognition. However, this perceptron could only solve linear problems, so it did not receive much attention.

In 1969, Minsky and Papert of MIT developed a multilayer neural network model that introduced a hidden layer

to the perceptron neural network and showed that classification was possible with a generalized nonlinear function.

In 1982, Hopefield developed a back-propagation algorithm that could effectively estimate the weight coefficients

of a multilayer neural network. Since then, computer performance has improved, making it easier to estimate

weight coefficients using the back-propagation algorithm, and neural network models have been widely used

in real-world problems. In Section 7.4.1, a single-layer neural network model is introduced to understand

neural network models, and in Section 7.4.2, a multilayer neural network model is explained.

7.4.1 Single-layer neural network

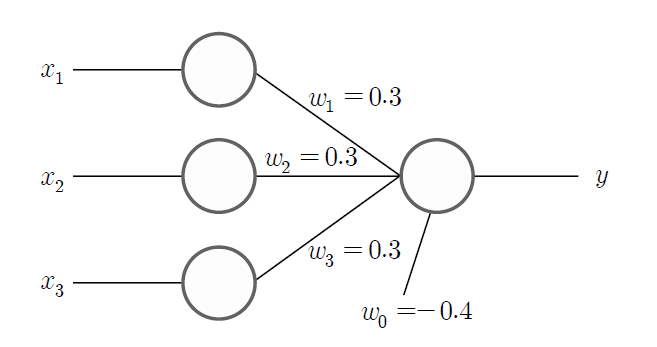

To understand the artificial neural network model, Let us look at the following single-layer neural network example.

Example 7.4.1 (Single-layer neural network)

Suppose \(y\) is a group variable where there are two groups, denoted '+1' and '-1', and there are three binary variables

\(x_{1}, x_{2}, x_{3}\) which have values either 0 or 1. If two or more of the three binary variables have the value 1,

classify them as the group ‘+1’, and if they have one or fewer 1 value, classify them as the group ‘-1’ as in Table 7.4.1.

Create a single-layer neural network model that can perform such classification and classify this data.

| Table 7.4.1 Possible values of three binary variables \(x_{1}, x_{2}, x_{3}\) and their group \(y\) |

| Number |

\(x_{1}\) |

\(x_{2}\) |

\(x_{3}\) |

\(y\) |

| 1 | 0 | 0 | 0 | -1 |

| 2 | 0 | 0 | 1 | -1 |

| 3 | 0 | 1 | 0 | -1 |

| 4 | 0 | 1 | 1 | +1 |

| 5 | 1 | 0 | 0 | -1 |

| 6 | 1 | 0 | 1 | +1 |

| 7 | 1 | 1 | 0 | +1 |

| 8 | 1 | 1 | 1 | +1 |

Answer

If the predicted value of the group is \(\hat y\), the above data can be classified using the following linear function

model.

$$ \small

\hat y = \{ \array {\; +1 \quad & if \;\; 0.3 x_{1} + 0.3 x_{2} + 0.3 x_{3} - 0.4 > 0 \cr

\; -1 \quad & if \;\; 0.3 x_{1} + 0.3 x_{2} + 0.3 x_{3} - 0.4 < 0 } \

$$

For example, if \(\small x_{1} = 1, \; x_{2} = 1, \; x_{3} = 0 \), then

\(\small 0.3 x_{1} + 0.3 x_{2} + 0.3 x_{3} - 0.4 = 0.2\), so \(\hat y\) = +1.

If \(\small x_{1} = 0, \; x_{2} = 1, \; x_{3} = 0 \), then

\(\small 0.3 x_{1} + 0.3 x_{2} + 0.3 x_{3} - 0.4 = -0.1 \), so \(\hat y\) = -1.

Let us put aside the discussion of how to create such a linear classification model for a moment

and if we represent the above model as a neural network in an easy-to-understand way,

it is as in <Figure 7.4.3>. This is called a single-layer neural network or

perceptron.

<Figure 7.4.3> Single layer neural network which is a linear classification model

As you can see in the figure, there is an input node to display the value of three variables

\(\small x_{1}, \; x_{2}, \; x_{3} \) and

the output node of the model to display the value of the group variable \(\small y\).

The nodes are also called neurons in neural networks as the human brain.

Each input node is connected to the output node with a weight coefficient, which describes

the connections between neurons in the brain. Just as neurons in the brain can learn and

make decisions, neural networks use data to train the optimal weight coefficients

(in the figure, \(\small w_{1} = 0.3, w_{2} = 0.3, w_{3} = 0.3 \)) that connect

the relationship between input nodes and output nodes. The output node of the neural network

calculates the value \(\hat y\) of the group by adding a constant \(\small w_{0} = -0.4\)

to the linear combination using the weight coefficients of each input node to calculate

the value \(\small w_{0} + w_{1}x_{1} + w_{2}x_{2} + w_{3}x_{3}\), which is called a

linear combination function. The constant \(\small w_{0}\) is called a bias factor.

The sign function \(sign(x)\) is used to investigate the sign of the calculated

linear combination function value which is called an activation function.

In general, when there are \(m\) variables \(x_{1}, x_{2}, ... , x_{m}\) and

the weighting coefficients for each variable are \(w_{1}, w_{2}, ... , w_{m}\)

and the constant term (bias) is \(w_{0}\), the classification function of a single-layer neural network model,

such as Example 7.4.1, can be expressed as a nonlinear function as follows.

$$

\hat y = sign( w_{0} + w_{1}x_{1} + w_{2}x_{2} + \cdots + w_{m}x_{m} )

$$

Here, the linear combination (or weighted sum) of each variable

\(w_{0} + w_{1}x_{1} + w_{2}x_{2} + \cdots + w_{m}x_{m} \) is called a

combination function.

The sign function, \(sign(x)\) that has a value of +1 when \(x\) is positive and a value of -1

when \(x\) is negative, is called an

activation function. The activation function

is a function that converts the input combination function value back into a certain range of values.

The classification function of single-layer neural network is a composite function of a linear combination function

with the sign function.

In the example above, a weighted sum of input information was used as the combination function,

but there are other combination functions such as simple sums of input information, maximum values, minimum values,

or logical ANDs and ORs, but the weighted sum is the most commonly used.

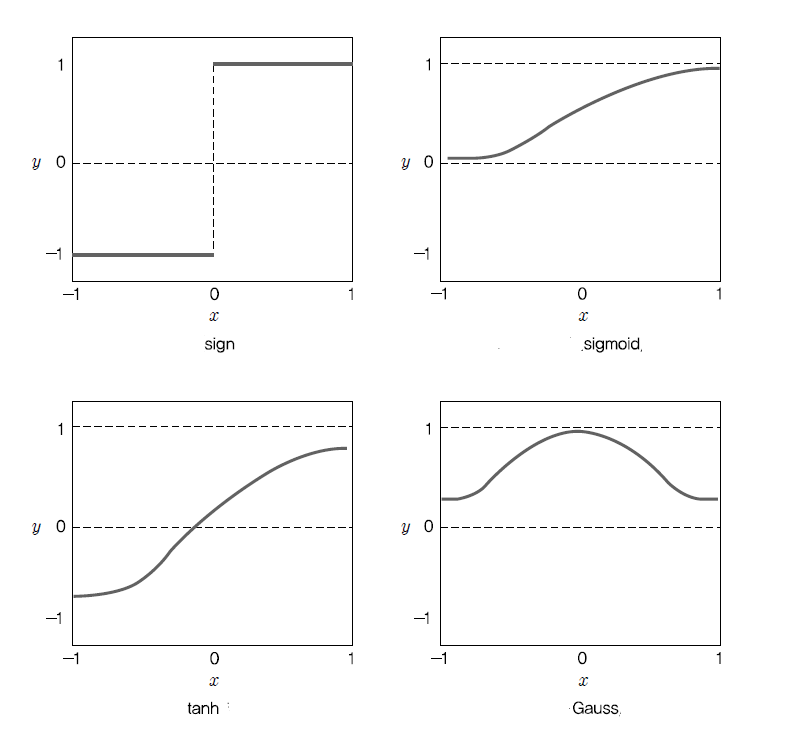

In addition to the sign function \(sign(x)\), examples of frequently used activation functions

are as in Table 7.4.2, and <Figure 7.4.4> shows shapes of these activation functions.

| Table 7.4.2 Examples of activation functions |

| Name |

Activation fuction |

Range |

| \(sign\) function | \(y = sign(x)\) | -1, +1 |

| \(sigmoid\) fuction | \(y = \frac{1}{1+e^{-x}}\) | (0, 1) |

| \(tanh\) function | \(y = \frac{e^{x} - e^{-x}}{e^{x} + e^{-x}}\) | (-1, 1) |

| \(Gauss\) function | \(y = e^{-\frac{x^2}{2}}\) | (0, 1) |

<Figure 7.4.4> Shapes of activation functions

The sigmoid function, which is widely used as an activation function, converts the input value

to a value between (0,1). This function has little effect on the value of \(y\)

when the value of \(x\) is very large or very small. When the sigmoid function

\(y = \frac{1}{1+e^{-x}}\) is differentiated, it has the following good property.

$$

\begin{align}

y' &= \frac{e^{-x}}{(1+e^{-x})^2} \\

&= \frac{1}{1+e^{-x}} (1 - \frac{1}{1+e^{-x}}) \\

&= y (1 - y)

\end{align}

$$

It means that the differentiation of the sigmoid function \(y\) can be easily calculated as \(y(1-y)\).

Because of this property of the sigmoid function, it is widely used in optimization problems

to obtain the rate of change easily.

Learning algorithm for single layer neural network

In the classification function of the single-layer neural network model, estimating the weight coefficients,

\(w_{1}, w_{2}, ... , w_{m}\) and the constant term \(w_{0}\) is called a learning

of the neural network. Let \(n\) training data be

\(D = \{ (x_{i1}, x_{i2}, ... , x_{im}, y_{i}),\; i=1,2,..., n \}\)

and \(w_{1}^{(i)}, w_{2}^{(i)}, ... , w_{m}^{(i)}\) be the \(i\)th iteration estimated values

of the weight coefficients. The weight coefficients of the single-layer neural network are estimated

using an iterative search algorithm as follows.

[

Learning algorithm for the single-layer neural network]

| Step 1 |

Let \(D = \{ (x_{i1}, x_{i2}, ... , x_{im}, y_{i}),\; i=1,2,..., n \}\) be the training data |

| Step 2 |

\(w_{1}^{(0)}, w_{2}^{(0)}, ... , w_{m}^{(0)}\) be the initial estimated value of the coefficients and \(\lambda\) is the learning rate |

| Step 3 |

for i = 1 to n do |

| Step 4 |

\(\qquad\)for j = 1 to m do |

| Step 5 |

\(\qquad \qquad\)Estimate \(y_{i}^{(i)}\) using \(w_{1}^{(i-1)}, w_{2}^{(i-1)}, ... , w_{m}^{(i-1)}\) |

| Step 6 |

\(\qquad \qquad\)\(w_{j}^{(i)} = w_{j}^{(i-1)} + \lambda (y_{i} - y_{i}^{(i)}) x_{ij} \) |

| Step 7 |

\(\qquad\)end for |

| Step 8 |

end for |

In step 2 of the algorithm, the initial values of the weight coefficients

\(w_{1}^{(0)}, w_{2}^{(0)}, ... , w_{m}^{(0)}\) usually use random numbers between 0 and 1.

\(\lambda\) is called a

learning rate and has a value between 0 and 1.

If the learning rate is close to 1, the estimated value changes a lot, and if it is close to 0,

the estimated value changes slowly. In step 5, \(y_{i}^{(i)}\) is the estimated value

when the group value \(y_{i}\) is estimated \(i\) times repeatedly. When this algorithm is repeated

as many times as the number of data (\(i = 1, 2, ... , n\)), we say that

‘the neural network has been trained’.

In step 6, the search algorithm for weight coefficients such as

\(w_{j}^{(i)} = w_{j}^{(i-1)} + \lambda (y_{i} - y_{i}^{(i)}) x_{ij} \) can be intuitively

easily understood. The \(i\)th estimate \(w_{}^{(i)}\) for the weight coefficient of \(x_{j}\)

is obtained by adding a value proportional to the current prediction error \((y_{i} - y_{i}^{(i)})\)

to the previous estimated weight coefficient \(w_{j}^{(i-1)}\).

If the prediction is accurate, \((y_{i} - y_{i}^{(i)})\) = 0, so the weight coefficient does not change.

If the prediction is not accurate, for example, \(y_{i}\) = +1, \(y_{i}^{(i)}\) = -1,

then the prediction error \((y_{i} - y_{i}^{(i)})\) = 2, so in order to increase the estimated value,

the weight coefficient of the input node with a positive value is increased,

and the weight coefficient of the input node with a negative value is decreased.

On the other hand, if \(y_{i}\) = -1, \(y_{i}^{(i)}\) = +1,

then the prediction error \((y_{i} - y_{i}^{(i)})\) = -2, so in order to reduce the estimated value,

the weight coefficient of the input node with a negative value is increased,

and the weight coefficient of the input node with a positive value is decreased.

The above search method is an algorithm that finds weighting coefficients which minimize

the sum of square errors when the estimated value \(\hat y_{i}\) for each data group is found

using the linear combination function \(w_{0} + w_{1}x_{1} + w_{2}x_{2} + \cdots + w_{m}x_{m} \)

and the sigmoid activation function. The sum of squared errors in a single-layer neural network

with \(m+1\) weighting coefficients \(\boldsymbol w = (w_{0}, w_{1}, w_{2}, ... , w_{m})\)

is as follows.

$$

E(\boldsymbol w) = \sum_{i=1}^{n} \; (y_{i} - \hat y_{i})^2

$$

In order to find \(\boldsymbol w = (w_{0}, w_{1}, w_{2}, ... , w_{m})\) that minimizes

the sum of squared errors, we can differentiate \(E(\boldsymbol w)\) partially

with respect to each \(w_{j}\) as follows.

$$

\frac{\partial E(\boldsymbol w)}{\partial w_{j}} = -2 \; \sum_{i=1}^{n} \; (y_{i} - \hat y_{i}) \frac{\partial \hat y_{i}}{\partial w_{j}}

$$

Therefore, one way to search for the weight coefficient \(w_{j}\) that minimizes

the sum of squared errors is to move in the direction of the partial derivatives as follows.

$$

w_{j} \;←\; w_{j} \;-\; \lambda \; \frac{\partial E(\boldsymbol w)}{\partial w_{j}}

$$

In the case of the linear combination function and sigmoid activation function, the algorithm

for searching weight coefficients can be created as follows.

$$

w_{j} \;←\; w_{j} \;-\; \lambda \; (y_{i} - \hat y_{i}) x_{ij}

$$

For more information on the algorithm, please refer to the relevant literature,

and let us examine the learning of a single-layer neural network using the following example.

Example 7.4.2

For the single-layer neural network of Example 7.4.1, train the neural network

with the initial values for the weight coefficients as

\(w_{1}^{(0)}\) = 0.2, \(w_{2}^{(0)}\) = 0.1, \(w_{3}^{(0)}\) = 0.1, the bias \(w_{0}\) = -0.4,

and the learning rate \(\lambda\) = 0.1.

Answer

Table 7.4.3 is the application of the learning algorithm to the single-layer neural network, which calculates

the weighted linear combination

\(\small \boldsymbol w^{(i)} = w_{0} + w_{1}^{(i-1)}x_{1} + w_{2}^{(i-1)}x_{2} + w_{3}^{(i-1)}x_{3}\)

and the estimation of group value \(\small \hat y_{i} = sign(\boldsymbol w^{(i)})\)

using the given initial values.

| Table 7.4.3 Application of learning algorithm to the sigle-layer neural network |

| iteration |

data |

linear combination function |

activation function |

modified coefficients |

| i |

\(x_{i1}\) |

\(x_{i2}\) |

\(x_{i3}\) |

\(y_{i}\) |

\(\small \boldsymbol w^{(i)} = w_{0} + w_{1}^{(i-1)}x_{1} + w_{2}^{(i-1)}x_{2} + w_{3}^{(i-1)}x_{3}\) |

\(\small \hat y_{i} = sign(\boldsymbol w^{(i)})\) |

\(w_{1}^{(i)}\) |

\(w_{2}^{(i)}\) |

\(w_{3}^{(i)}\) |

| 1 | 0 | 0 | 0 | -1 | -0.4 | -1 | 0.2 | 0.1 | 0.1 |

| 2 | 0 | 0 | 1 | -1 | -0.3 | -1 | 0.2 | 0.1 | 0.1 |

| 3 | 0 | 1 | 0 | -1 | -0.3 | -1 | 0.2 | 0.1 | 0.1 |

| 4 | 0 | 1 | 1 | +1 | -0.2 | -1 | 0.2 | 0.3 | 0.3 |

| 5 | 1 | 0 | 0 | -1 | -0.2 | -1 | 0.2 | 0.3 | 0.3 |

| 6 | 1 | 0 | 1 | +1 | 0.1 | +1 | 0.2 | 0.3 | 0.3 |

| 7 | 1 | 1 | 0 | +1 | 0.1 | +1 | 0.2 | 0.3 | 0.3 |

| 8 | 1 | 1 | 1 | +1 | 0.4 | +1 | 0.2 | 0.3 | 0.3 |

Looking at the table, if the actual group value \(\small y_{i}\) and the estimated value

\(\small \hat y_{i}\) are the same, there is no change in the weight coefficient (iterations 1, 2, and 3).

In iteration 4, since the error is (\(\small y_{4} - \hat y_{4}\)) = 2, the weight coefficient of

the variable with \(\small x_{2}\) = 1 and \(\small x_{3}\) = 1 is increased by

\(\small \lambda \times (y_{4} - \hat y_{4}) \times x_{4j}\) = 0.2.

Since the other data have the same group value and predicted value, there is no change

in the weight coefficient, so the estimated final weight coefficient is

\(w_{1}\) = 0.2, \(w_{2}\) = 0.3, \(w_{3}\) = 0.3. That is, the final neural network model is

\(\small \hat y = sign( -0.4 + 0.2 x_{1} + 0.3 x_{2} + 0.3 x_{3} )\). If this estimation formula

is applied to all data, the groups are accurately classified.

It should be noted that the estimation algorithm for the weight coefficients of

a single-layer neural network can have different solutions depending on the initial value

and learning rate. For example, if the initial values are the same and the learning rate is

\(\lambda\) = 0.05, the final weight coefficients are

\(w_{1}\) = 0.2, \(w_{2}\) = 0.25, \(w_{3}\) = 0.25, and this solution also correctly

classifies all data.

7.4.2 Multilayer neural network

The single-layer neural network model classifies data between two groups as a linear classification function.

However, it is not suitable when the data cannot be classified as a linear function, as in <Figure 7.4.2>.

In this case, a

multilayer neural network model which classifies data using a nonlinear function is useful.

<Figure 7.4.5> is an example of Example 7.4.1 expressed as a multilayer neural network.

As shown in the figure, a multilayer neural network consists of an

input layer consisting of input nodes,

a

hidden layer that is a set of intermediate nodes that synthesize the nodes of the input layer,

and an

output layer that synthesizes the nodes of the hidden layer. A neural network like

<Figure 7.4.5> has only one hidden layer, but can create multiple hidden layers, and each layer

can have multiple nodes, so various types of networks can appear.

<Figure 7.4.5> Example of multilayer neural network

The neural network in <Figure 7.4.5> can be expressed as a formula as follows. Let the weight coefficients

from the input node ① to the hidden nodes ④ and ⑤ be \(w_{14}\) and \(w_{15}\), let the weight coefficients

from the input node ② to the hidden nodes ④ and ⑤ be \(w_{24}\) and \(w_{25}\), and let the weight coefficients

from the input node ③ to the hidden nodes ④ and ⑤ be \(w_{34}\) and \(w_{35}\).

In the same way, let the weight coefficient from the hidden node ④ to the output node ⑥ be \(w_{46}\),

and let the weight coefficient from the hidden node ⑤ to the output node ⑥ be \(w_{56}\).

And if the bias constants of nodes ④, ⑤, and ⑥ are \(w_{04}, w_{05}, w_{06}\) and the activation function is

\(f_{4}, f_{5}, f_{6}\), then the output values \(O_{4}\) and \(O_{5}\) calculated from hidden nodes ④ and ⑤ are

as follows.

$$

\begin{align}

O_{4} &= f_{4} ( w_{04} + w_{14} x_{1} + w_{24} x_{2} + w_{34} x_{3} ) \\

O_{5} &= f_{5} ( w_{05} + w_{15} x_{1} + w_{25} x_{2} + w_{35} x_{3} )

\end{align}

$$

The value of the output node ⑥, i.e., the estimated value of \(y\), is the value of the activation function

for linear combination of \(O_{4}\) and \(O_{5}\) as follows.

$$

\hat y = f_{6} ( w_{06} + w_{46} O_{4} + w_{56} O_{6} )

$$

If we combine the above equations, the estimated value of \(y\) becomes the following complex nonlinear function.

$$

\hat y = f_{6} ( w_{06} + w_{46} f_{4} ( w_{04} + w_{14} x_{1} + w_{24} x_{2} + w_{34} x_{3} ) + w_{56} f_{5} ( w_{05} + w_{15} x_{1} + w_{25} x_{2} + w_{35} x_{3} ) )

$$

In the above example, if there are multiple hidden layers, more hidden nodes, and multiple output nodes,

the nonlinear function that represents the final output becomes more complex. Therefore,

the design of a multilayer neural network should always consider the following:

- How many hidden layers should there be?

- How many nodes should each hidden layer have?

- Is there a nonlinear function represented by these hidden layers and hidden nodes?

Let us assume that values of all variables, \(\boldsymbol x = (x_{1}, x_{2}, ... , x_{m})\), can be converted

to values between [0,1].

The following theorem shows the existence of a nonlinear function represented

by the multilayer neural network.

Theorem 7.4.1 Approximation of a continuous function (Kolmogorov)

When a continuous function \(f(\boldsymbol x)\) is defined on \([0,1]^{m}\), this function can be expressed

as follows.

$$

f(\boldsymbol x) = \sum_{k=1}^{2m+1} \; \Theta_{k} \left[ \sum_{j=1}^{m} \; \phi_{jk} (x_{j}) \right]

$$

Here, \(\Theta_{k}\) and \(\phi_{jk}\) are appropriately chosen functions.

This theorem can be interpreted as a neural network as follows. For the input nodes of variables

\(x_{1}, x_{2}, ... , x_{m}\), \((2m + 1)\) hidden nodes receive the sum of nonlinear functions \(\phi_{jk} (x_{j})\).

Each hidden node receiving this value outputs a nonlinear function \(\Theta_{k}\), and

the final output node calculates the sum of these. In other words, assuming that there is a nonlinear

function \(y = f(\boldsymbol x)\), this function can be approximated by a composite function of combination functions

and activation functions, such as equation in the Theorem 7.4.1. A neural network model consisting of

this complex approximation function is often called a black box. It is not known exactly

how many hidden nodes can approximate the function \(y = f(\boldsymbol x)\) well.

Design of multilayer neural network model

The neural network model is experimented with various combinations of the number of hidden layers

and the number of nodes through trial and error, and the general design method is as follows.

1) Data preparation

In the case of continuous variables, units of variables may be different, so the variable values are usually converted to be

between 0 and 1. A simple conversion method is to subtract the minimum value from the actual data value and

then divide it by the possible range of the variable (maximum value - minimum value). For ordinal variables,

the smallest ordinal value is set to 0, the larger ordinal value is set to 1, and the ordinal values in between are converted

proportionally. In the case of categorical variables, each category value is usually treated as one variable,

and a binomial value of 0 or 1 is used depending on the presence or absence of the category value.

It is desirable to have a certain number of data for each category value, but if the number of data is small,

it is sometimes combined with adjacent category values. Missing values are either removed or replaced

by estimating a value appropriate for the data.

2) Number of input nodes

If the variable is binomial or continuous data, assign one input node to each variable. If the variable

is categorical, assign one input node to each categorical value.

3) Number of output nodes

If there are two groups, one output node is sufficient. If there are \(K\) groups, assign \(K\) output nodes.

4) Number of hidden layers and number of hidden nodes

Determining the number of hidden layers and number of hidden nodes is a problem of determining

the nonlinear function of the neural network model. If the number of hidden layers and hidden nodes increases,

the model may be overfitted, so if possible, it is good to have a model that can classify satisfactorily

with a small number of hidden layers and hidden nodes. However, there is no exact method to find

the optimal number of hidden layers and hidden nodes. Usually, after setting the number of hidden layers and

hidden nodes sufficiently, we reduce them one by one and select a model with high accuracy and

a small number of hidden layers and hidden nodes. At this time, model selection criteria such as

AIC (Akaike information criteria) can be used.

If possible, it is good to obtain the classification function by setting the number of hidden layers to 1.

However, if too many nodes are created in one hidden layer, the number of hidden layers is set to two,

and the number of nodes in each layer is reduced. It is usually done so that the number of nodes in each layer

does not exceed twice the number of nodes in the input layer. Experiments to determine the number of

hidden layers and nodes take the most time in artificial neural network models.

5) Selection of activation function

Among the activation functions in Table 7.4.2, the sigmoid function, which is useful for the estimation algorithm

of weight coefficients, is often used. The activation function is known to affect the algorithm speed

during the training process of a neural network but does not have a significant effect on the results.

6) Initial value problem

Algorithms that estimate the weight coefficients of a multilayer neural network model require initial values,

and most of them randomly generate values between -1 and 1. Since there is a possibility that a given initial value

will find a local solution, it is necessary to experiment several times to find the same weight coefficients

by trying various initial values.

7) Interpretation of output variables

If there are two groups and one output node, the output value is a continuous value, so it can be classified

based on an appropriate boundary value. If there are multiple groups, the number of output nodes is usually

the same as the number of groups, and the group is classified based on the value of the output node

that is large (or small).

8) Sensitivity analysis

After obtaining the solution of the neural network using training data, it is a good idea to conduct

sensitivity analysis to determine the relative importance of the input variables. Change the value of

the input variable from the minimum to the maximum and examine the change in the output value.

Learning algorithm of multilayer neural networks

The process of estimating the weight coefficients of a multilayer neural network model is called

learning of the neural network. Since a multilayer neural network is a complex nonlinear function model,

estimating the weight coefficients is not easy. The learning algorithm for a single-layer neural network

is not suitable for a multilayer neural network with a nonlinear function that has many weight coefficients.

The estimation of the weight coefficients in a multilayer neural network uses the

gradient descent method.

Let the input node values of a multilayer neural network with \(m\) input variables be

\(\boldsymbol x = (x_{1}, x_{2}, ... , x_{m})\). Let the weight coefficient connecting node \(j\) to node \(k\)

in the neural network be \(w_{jk}\), the constant coefficient at this time be \(w_{0k}\), and

let all the weight coefficients appearing in this neural network be \(\boldsymbol w\).

The output of the neural network can be expressed as \(\hat y = f(\boldsymbol x : \boldsymbol w )\),

where the function \(f\) is a composite function of several combination functions and activation functions

as in Theorem 7.4.1. In order to find the weight coefficient \(\boldsymbol w\) of the multilayer neural network,

it is reasonable to minimize the distance \(d(y_{i}, \hat y_{i})\) between the observed group value

\(y_{i}\) of all data and the estimated value \(\hat y_{i}\) of the neural network.

If we use the Euclidean square distance, we find the weight coefficient that minimizes the error sum of squares

\(\small E(\boldsymbol w )\) as follows.

$$

E(\boldsymbol w ) = \sum_{i=1}^{n} \; ( y_{i} - \hat y_{i} )^2

$$

To find \(\boldsymbol w\) that minimizes the error sum of squares, we differentiate \(\small E(\boldsymbol w )\)

with respect to each \(w_{jk}\) as follows.

$$

\frac{\partial E(\boldsymbol w )}{\partial w_{jk}} = -2 \sum_{i=1}^{n} \; ( y_{i} - \hat y_{i} ) \; \frac{\partial \hat y_{i}}{\partial w_{jk} }

$$

If \(\hat y_{i}\) is estimated using the sigmoid activation function, the rate of change of the estimated value,

\(\small \frac{\partial \hat y_{i}}{\partial w_{jk} }\), is proportional to \(\hat y_{i} (1 - \hat y_{i}) \)

due to the differentiation characteristic of the sigmoid function. Therefore, we can create an algorithm

to search for weight coefficients as follows.

$$

w_{jk} \;←\; w_{jk} \;-\; \lambda \; \frac{\partial E(\boldsymbol w )}{\partial w_{jk} }

$$

Here, \(\lambda\) is the learning rate, which has a value between 0 and 1.

\(\frac{\partial E(\boldsymbol w )}{\partial w_{jk} }\) means the gradient descent rate, which implies

that the estimation of weight coefficients should be adjusted in the direction that decreases

the total error sum of squares. If the output value of input node \(j\) is \(O_{j}\) and

the error at output node \(k\) is \(E_{k}\), the above update of weight coefficients is as follows.

$$

w_{jk} \;←\; w_{jk} \;-\; \lambda \; E_{k} O_{j}

$$

Here, \(\small \lambda \; E_{k} O_{j}\) is the change amount of the weight coefficient,

which is the same concept as the estimation of the weight coefficient of the single-layer neural network.

That is, the weight coefficient is updated as a learning rate \(\lambda\) proportional to the input

\(O_{j}\) from node \(j\) by considering the error \(E_{k}\) of node \(k\).

In a similar way, the bias constant \(w_{0k}\) is updated as follows.

$$

w_{0k} \;←\; w_{0k} \;-\; \lambda \; E_{k}

$$

In this algorithm, the estimation of \(E_{k}\) and \(O_{j}\) is not easy when applied to the hidden nodes

in the multilayer neural network model, so the back-propagation algorithm developed by Hopefield is used.

The back-propagation algorithm sets a criterion for optimizing the initial weight coefficients and

the objective function, and divides it into the forward step and the backward step to repeatedly update

the weight coefficients. In the forward step, the estimated weight coefficients are used to calculate

the output values of all nodes, and the output values of the nodes in the layer \(l\) are used

to calculate the output values of the nodes in the layer \(l+1\). In the backward step, the output values

and error values for the nodes in the calculated layer \(l+1\) are used to estimate the error values for the nodes in the layer \(l\) and the weight coefficients are updated. This method is repeatedly applied

until the weight coefficients hardly change or the objective function value is optimized,

and the algorithm is stopped.

When the sigmoid activation function is used in the multilayer neural network in <Figure 7.4.5>,

let us estimate the weight coefficients by applying the back-propagation algorithm.

First, the initial weight coefficients are used to obtain the output values \(O_{1}, O_{2}, ..., O_{6}\)

of each node. Here, \(O_{1}, O_{2}, O_{3}\) are the values of the input variable \(x_{1}, x_{2}, x_{3}\).

The key is how to obtain the error \(E_{k}\) of each node. In the back-propagation algorithm,

it is estimated by considering the weighted sum of the errors of all nodes connected to node \(k\).

In the case of a sigmoid function, the rate of change \(\small \frac{\partial \hat y_{i}}{\partial w_{jk} }\)

is proportional to \(\hat y_{i} (1 - \hat y_{i}) \), so the error \(E_{6}\) of the output node ⑥

is estimated as follows.

$$

E_{6} \;=\; O_{6}(1-O_{6})(y_{i} - O_{6})

$$

Here, \(O_{6}(1-O_{6})\) denotes the rate of change \(\hat y_{i}(1 - \hat y_{i})\), and

the \((y_{i}-O_{6})\) term denotes the estimation error \((y_{i} - \hat y_{i})\).

That is, the meaning of the error \(E_{6}\) is the estimation error \((y_{i} - O_{6})\)

multiplied by the error change rate \(O_{6}(1-O_{6})\).

The error \(E_{5}\) of hidden node ⑤ is calculated by multiplying the error change rate

\(O_{5}(1-O_{5})\) by the weighted sum of errors of all nodes connected to node ⑤,

which is called the back-propagation of the error. That is,

$$

E_{5} \;=\; O_{5}(1-O_{5}) \sum_{k} \; w_{5k} E_{k}

$$

After calculating the error \(E_{4}\) of hidden node ④ in a similar way, the weight coefficients are updated.

Let us look at the back-propagation algorithm for estimating the weight coefficient of

a multilayer neural network through the following example.

Example 7.4.3 (Learning algorithm of the multilayer neural network)

For the multilayer neural network model in Figure 7.4.5, let the input data be group 1 and

the variable values be (\(x_{1}, x_{2}, x_{3}\) ) = (1, 0, 1). Let us find the weight coefficient

and bias of the model equation using the back-propagation algorithm of the gradient descent method.

The same sigmoid function, f(x), is used for all activation functions, and the initial values of the weight coefficient

and bias are set as follows using a random number between (-1,1). Let the learning rate be \(\lambda\) = 0.1.

| Table 7.4.4 Initial values of the weight coefficients for the multilayer neural network in Figure 7.4.5 |

| \(w_{14}\) |

\(w_{15}\) |

\(w_{24}\) |

\(w_{25}\) |

\(w_{34}\) |

\(w_{35}\) |

\(w_{46}\) |

\(w_{56}\) |

\(w_{04}\) |

\(w_{05}\) |

\(w_{06}\) |

| -0.51 |

-0.99 |

0.35 |

-0.45 |

0.39 |

0.19 |

0.27 |

0.71 |

-0.75 |

-0.09 |

0.18 |

Answer

The forward step of the back-propagation algorithm calculates the output values of all nodes using the given

initial values. In the neural network of <Figure 7.4.5>, the output values \(O_{1}, O_{2}, O_{3}\)

of nodes ①, ②, and ③ are the values of the input variables \(x_{1}, x_{2}, x_{3}\), and the output values

of nodes ④, ⑤, and ⑥ are as follows, using the given initial weight coefficients.

$$ \small

\begin{align}

O_{4} &= f( w_{14} x_{1} + w_{24} x_{2} + w_{34} x_{3} + w_{04} ) \\

&= f( -0.51 \times 1 \;+\; 0.35 \times 0 \;+\; 0.39 \times 1 \;-\; 0.75 \\

&= f(-0.87) = 0.2953 \\

O_{5} &= f( w_{15} x_{1} + w_{25} x_{2} + w_{35} x_{3} + w_{05} ) \\

&= f( -0.99 \times 1 \;-\; 0.45 \times 0 \;+\; 0.19 \times 1 \;-\; 0.09 \\

&= f(-0.89) = 0.2911 \\

O_{6} &= f( w_{46} O_{4} + w_{56} O_{6} + w_{06} ) \\

&= f( 0.27 \times 0.2953 \;+\; 0.71 \times 0.2911 \;+\; 0.18 \\

&= f(0.4664) = 0.6145 \\

\end{align}

$$

The backward step of the back-propagation algorithm first estimates the error \(\small E_{6}\) of node ⑥,

and then estimates the errors of nodes ④ and ⑤. The estimation of the error \(\small E_{6}\) of node ⑥

is as follows.

$$ \small

\begin{align}

E_{6} \;&=\; O_{6}(1-O_{6})(y_{i} - O_{6}) \\

&=\; 0.6145 \times (1-0.6145) \times (1 - 0.6145) = 0.0913

\end{align}

$$

Here, the \(\small O_{6}(1-O_{6})\) term is the rate of change from the differentiation of the sigmoid function

and \(y\) is the actual group value. The meaning of the error \(\small E_{6}\) is the estimation error,

\(\small y_{i} - O_{6}\), multiplied by the error change rate \(\small O_{6}(1-O_{6})\).

The error \(\small E_{5}\) of hidden node ⑤ is calculated by multiplying the error change rate